Wider South East Q1 2021

The wider South East saw strong house price growth in Q1, and the average time taken to rent a property reached record lows. The pandemic may be impacting the locations people choose, perhaps leaving traditionally popular commuter towns overlooked.

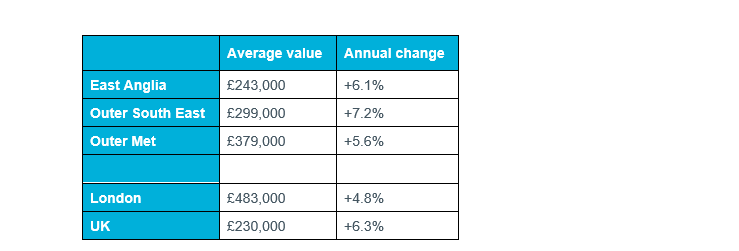

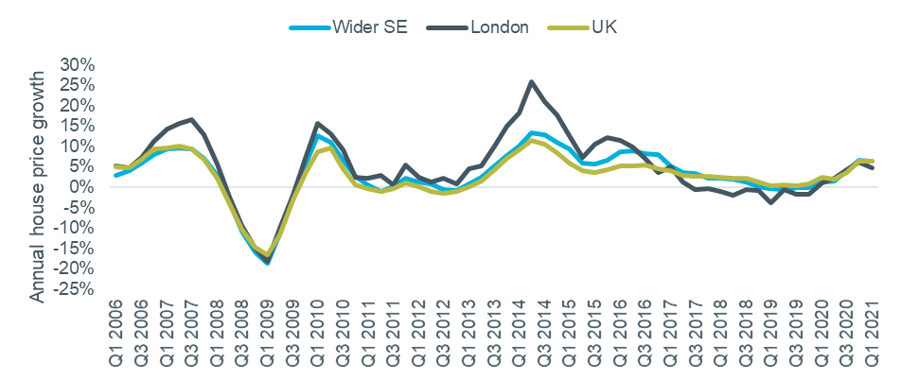

The wider South East continued to see strong price growth in Q1, in line with the performance of the UK market and ahead of London, according to the Nationwide indices. Table 1 shows their latest (Q1) index results, with Figure 1 showing the data back to 2006.

Table 1: Regional House Prices, Q1: 2021

Source: Nationwide House Price Index (values rounded to £1000)

Figure 1: House Price Growth: Wider SE, London and National

Source: Nationwide (Wider SE represented by average of ‘Outer Met’, ‘Outer SE’ and ‘East Anglia’ areas). Note: Quarterly regional series uses different UK figure to main monthly index.

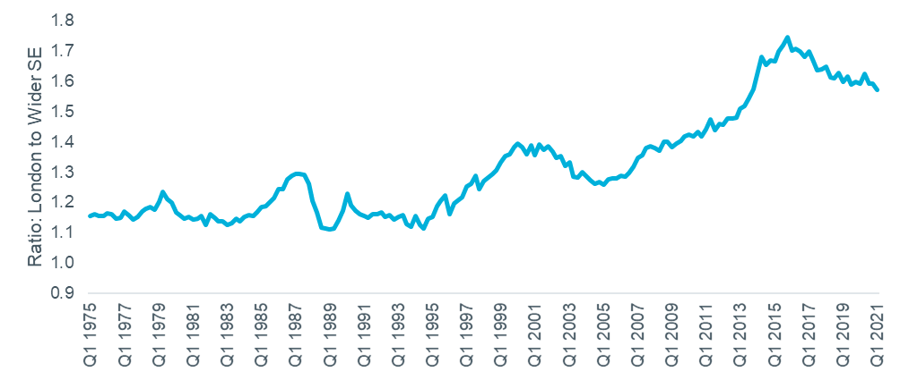

Figure 2 compares the long run data and shows that the fall in the ratio of London values to the wider South East has slowed. The high point of 1.75 was reached in Q4 2015, with the latest figure being 1.57, a small fall from 1.59 last quarter.

Figure 2: Ratio of London to Wider South East Values

Source: Nationwide (Wider SE represented by average of ‘Outer Met’, ‘Outer SE’ and ‘East Anglia’ areas).

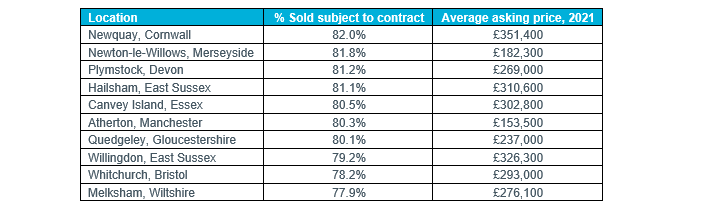

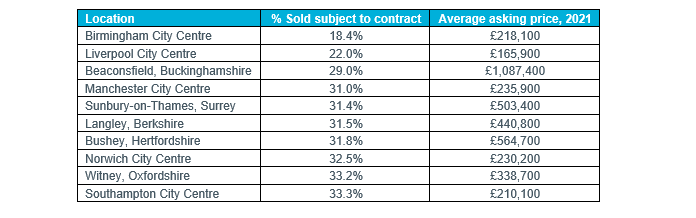

Analysis by Rightmove suggests that the pandemic may be having an impact on the destinations people choose when moving out of London, potentially seeing the traditionally popular commuter towns of the wider South East overlooked. Based on the proportion of listings marked as sold, the top ten sellers’ markets only included three locations in the East or South East, all near the coast (Hailsham and Willingdon in East Sussex and Canvey Island in Essex). The list was topped by Newquay in Cornwall and the full list is shown below.

Table 2: Top 10 Sellers’ Markets

Source: Rightmove

By contrast, the top ten buyers’ markets contained five commuter belt locations, along with a mix of regional city centres. The full list is shown below.

Table 3: Top 10 Buyers’ Markets

Source: Rightmove

Wider South East Rental Market

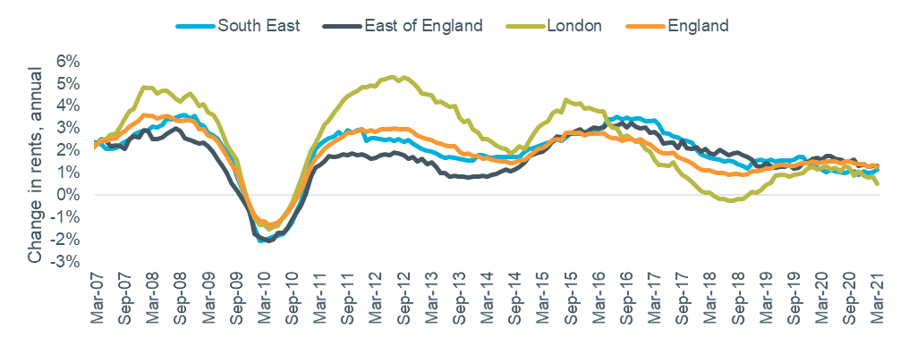

Figure 3 shows rental growth data at regional and national level from the ONS. This is based on all rents paid so is slow to respond to changes in market conditions. With annual growth of 1.2% in March, the South East moved back more into line with the East and the national average (both +1.3%), whereas growth in London slowed to 0.5%.

Figure 3: Rental Growth: Southern regions, London and National

Source: ONS Index of Private Housing Rental Prices

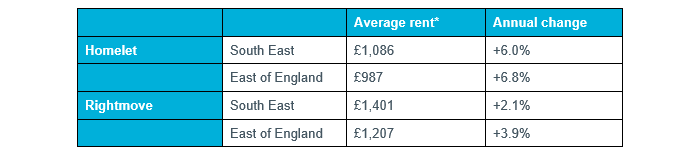

Analysis based on new lettings showed higher levels of growth. A summary of the latest data, from Rightmove’s Q1 index and Homelet’s March index, is shown in the table below. Homelet reported very strong growth in both the East and South East, noting that this was driven by increased demand over the second half of the year.

Table 4: Regional Rental Data, Q1 2021

Source: Homelet Index (actual achieved rents), Rightmove Rental Trends Tracker (asking rents).

Rightmove’s report noted that their average time to rent metric reached record lows in both the South East (18 days) and the East (16). This is driven by supply being down 54% (national, excluding London) compared to the same period in 2019, leading to strong competition for properties. The report also looked at longer-term data to review trends over five years. Rental values in the South East have grown 8.6% since Q1 2016, and 10.8% in the East. Both of these are in line with inflation over the period.