UK & London lettings update Q3 2023

Rents continue to rise, but a slight loosening in supply means the pace of growth is beginning to ease in many regions.

Article updated 7 September 2023

Rents will continue to rise this year, but at a slower rate than in 2022.

Our quarterly update examines the latest trends in the UK, regional and prime London lettings markets.

Key highlights:

- Rents have risen strongly over the last 12 months as demand far outstripped the supply of homes to rent

- Rental growth will continue into 2023, but at a slower rate

- Constraints on the supply of rental property are beginning to ease, but are unlikely to fully unwind quickly

UK rental market

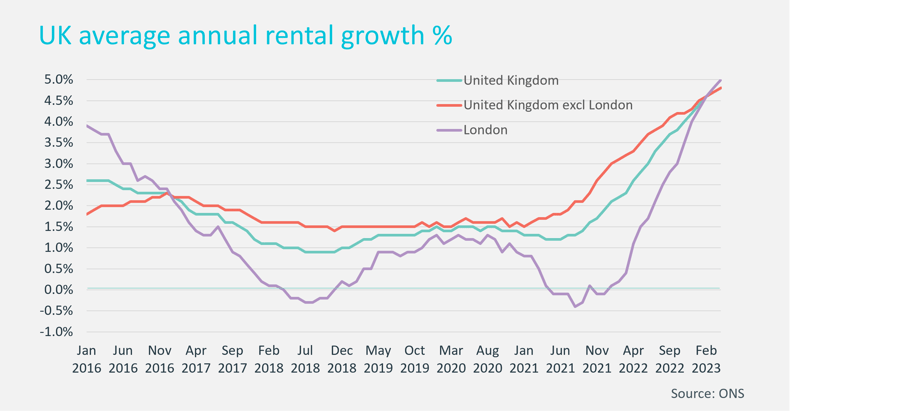

The UK rental market is still moving strongly, with rents continuing to rise. The official data on rents show that rental growth rose to 5% in May, up from 4% at the end of last year, and 1.2% in the summer of 2021.

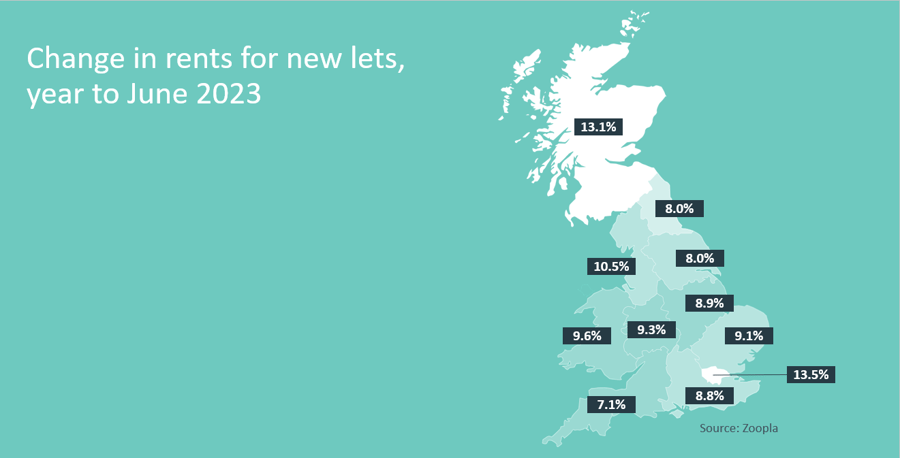

Looking at new lets only, the rate of growth is even higher, with Zoopla reporting that a 10.4% annual rise in rents for those moving into a new rental property. This rises to 13.5% in London, where the supply remains most constrained.

There are signs however of a slight loosening in supply, in some cases driven by affordability constraints, which will start to reduce the upwards pressure on asking rents.

Rising mortgage rates are putting pressure on landlords with gearing, as well as homeowners. Around 60% of landlords have a mortgage, although a third of these have more than 50% equity in their properties, according to Zoopla. The rise in borrowing costs has prompted some landlords to look at exiting the market. Zoopla says that one in ten properties currently for sale has previously been a rental property. This is a fairly typical level of churn in the market – but the difference now is that whereas 50% of those properties were bought by investors and returned to the rental market, this proportion has now dropped to 30%.

Coupled with the increased costs of entering the market as a landlord, this now signals that overall stock levels in the rental market are starting to be eroded. The burgeoning Build-to-Rent sector will fill in some of the gaps, but in the short-term, the lack of rental properties, especially in London and the South East, will continue to act as an upward driver on rents.

There is a caveat here however, in that agents are reporting that rental properties that are not well-priced are not attracting the same levels of attention. There is a natural ceiling for properties in the rental market, and while this may have been pushed higher in the market of the last 18 months, this too will act as a brake on further hefty rent rises.

Focus on: Prime London Rental

The bounce back in rental demand after the pandemic amid constrained supply created a turbo-charged market in 2022. There is still very strong rental demand compared to pre-pandemic norms, but it has now plateau-ed in many areas, or has started to recede slightly.

Rents in some central prime areas fell during 2020 and 2021 as students returned home and some renters choose to move out of city centres, creating a rise in supply. More supply was added as short-term rental landlords also moved their properties into the long-term rental market in the absence of visitors. Some landlords, faced with increased tax and regulation also took this opportunity to sell their properties.

As the pandemic ended, these trends reversed. Overseas and domestic tourism returned with a bang, prompting those short-term landlords to take their properties back out of the long-term market. At the same time, students, graduates and workers returned to city centres as supply was tight, putting upwards pressure on rents.

Demand for rental properties is still high in relation to most historical norms, yet the number of homes listed for rent was down more than 6% year-on-year in May, according to data from Lonres, highlighting the demand/supply imbalance. As the sales market outlook becomes cloudier, some potential sellers may be tempted to rent out properties if they can not achieve their asking price, which could act as a loosener on supply in some markets.

The rental market remains seasonal, especially in city centres, and prime central London is no exception. Demand rises in late summer, with the peak months in August and September as students return to university, new school terms start, and graduates embark on their first jobs. This will put some further upward pressure on rents, but as shown in the chart below, the growth in rents has peaked, so overall rental growth is set to be lower this year than last year. Cluttons forecasts show prime London rental growth at 5% by the end of the year.

The sharp rise in rents over the last few years alongside a slower rise in prices means prime London yields have also moved out over the last 24 months, from 2.7% in summer 2021 to 3.2% in June this year.

Outlook

| Year | UK house price change | Prime London sales price change | Prime London rental value change |

|---|---|---|---|

| Dec-22 | 3.0% | 1.0% | 12% |

| Dec-23 | -8.0% | -4.0% | 5.0% |

| Dec-24 | -2.0% | 0.5% | 3.5% |

| Dec-25 | 4.5% | 3.0% | 3.0% |

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.