UK rental review Q2 2020

Rental market bounces back but outlook is mixed as increases in remote working and studying could limit demand in some sectors.

The national rental market restarted in mid-May (in England, later in devolved nations) with most indicators suggesting that the Coronavirus lockdown caused a blip rather than permanent change.

As shown in Figure 1, the June RICS survey reported strong recoveries in tenant demand and rent expectations, following record lows in April. The ONS rental index showed rents continuing to grow at around 1.4% annually in June (note that this data covers all rents paid rather than new listings so can be slow to respond to changes).

Other data sources also reported to a swift recovery in rental activity and no negative impact on rents at national level. Rightmove’s Q2 2020 Rental Price Tracker reported that rental enquiries hit an all time high on 6th July and that demand was 40% higher compared to the same period last year. Asking rents grew by 3.7% quarter-on-quarter according to their Q2 index, taking annual growth to 3.4%. Homelet’s June index reported annual growth of 1.1%.

The ONS have surveyed the public (Opinions and Lifestyle Survey) weekly throughout the Coronavirus crisis. The latest results (covering 2nd to 5th July) found that 18% of respondents said their household finances were being affected – down from 29% in mid-April. Of these, a large majority continue to report reduced income as the main reason, as shown in Figure 2. The proportion of that 18% reporting that they are ‘struggling to pay bills’ was 14% in the most recent results – about 2.5% of everyone surveyed.

While these reports suggest relative normality in the rental market, wider economic and employment data indicate potential issues on the horizon. Research by YouGov for Shelter showed that the number of people in rent arrears has increased by over 225,000 between March and June.

Government support for private renters has remained limited, with no direct financial help, only tweaks to benefits and guidance for landlords to show forbearance where possible. On 17th July the government published an amendment setting out how evictions, which have been paused during the crisis, can restart from 23rd August. Whether this leads to a large increase in the number of evictions (compared to before the ban) remains to be seen, and until then the potential impact on supply and rents is unclear.

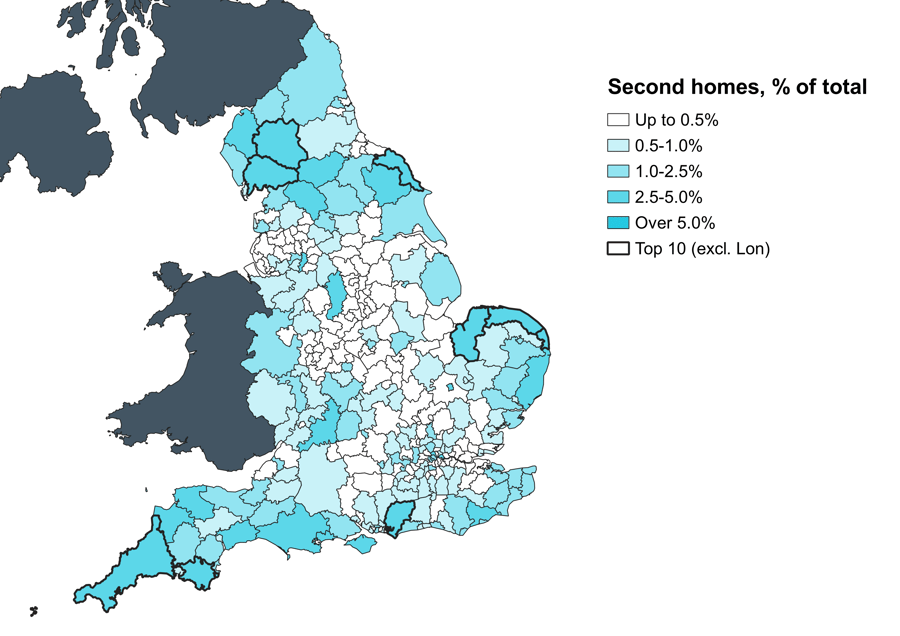

Holiday rentals saw record levels of bookings after the restrictions on UK travel were eased, with tourists potentially preferring to avoid hotels and planes where possible in order to make social distancing easier. If this trend grows, locations with high proportions of second and holiday homes could have increasing issues with locals being priced out. The map below highlights these areas, which are concentrated in coastal regions and National Parks.

Figure 3: Second homes in England, 2019

Source 2019 Council Tax Base

The outlook for student rental property is more mixed. Most universities are intending to offer a mix of online and in-person teaching for the 20/21 academic year, but demand for student housing is set to be lower. Unite Students, the largest owner of purpose-built student accommodation in the UK, reported in July that they expected a 10-20% fall in rental income for 20/21 compared to the year before, with an occupancy target of 90% (98% achieved in 19/20). This reduction follows Unite forgoing rent on almost two-thirds of their properties in the 19/20 summer term.

Travel restrictions may make it more difficult for international students to attend their courses. Around three-quarters of international students surveyed (in a study by IDP Connect) are expecting to commence their studies in the autumn as planned, further hitting demand for accommodation. The rental markets of major university cities and towns will see weaker rents and more supply in the short term.