UK sales review Q1 2022

Demand remained ahead of supply in Q1, leading to high levels of activity and price growth continuing the trends from 2021.

The volume of stock coming to market is gradually increasing but cannot keep pace with buyer appetite, so the strong sellers’ market persists.

High prices combined with rapid rises in the cost-of-living mean that affordability will be stretched for some buyers, but so far there has been limited sign of any slowdown. The second half of 2022 should see the market become more balanced.

Monthly Data

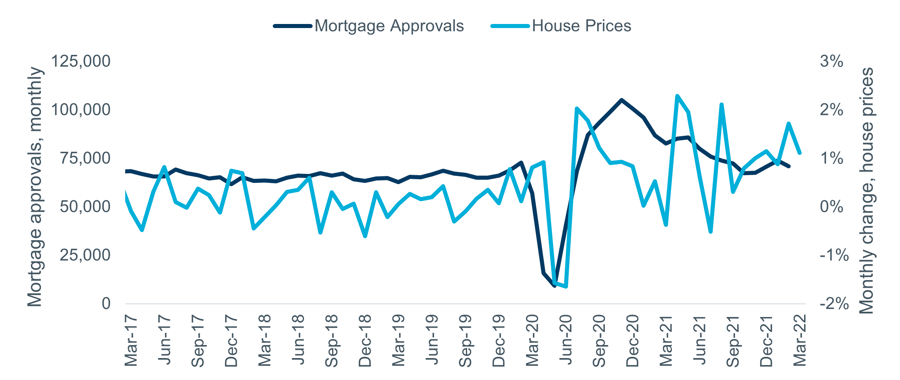

There were 71,000 mortgage approvals for purchase in February, according to Bank of England data. While this represents a fall both in monthly (-3.9%) and annual (-18%) terms, it remains above the longer-term average level of activity. House prices grew further in all three months in Q1 according to the Nationwide index; with a total rise over the quarter of 4.1%. Longer-term trends for both series are shown in Figure 1.

Figure 1 – UK house prices and mortgage approvals, monthly

Source: Nationwide HPI, Bank of England. Note: both seasonally adjusted

Transaction trends

Sales volumes remained relatively high in Q1, with individual months running at around 12% over the average pre-pandemic level. This suggests that, while the stamp duty holiday likely stimulated activity, there is still sustained demand many months after its end. On an annual basis the growth in transactions is slowing as Q1 last year saw very high levels of activity. HMRC’s latest data reports 1.37m transactions in the year to March.

The ONS data tells a similar story of high activity but slowing growth. Note this is only available up to December due to their lag in reporting completions and the latest months are still likely to be revised upwards.

Agent sentiment suggests a continuation of these more settled trends in the short term. The latest RICS survey results show the net balance for ‘Agreed Sales’ was at +9 in March, up from -12 three months earlier. ‘Sales Expectations’ were at +16, very much in line with levels over the past few months.

Figure 2 shows the two survey metrics plotted against the two measures of actual transaction levels. In the past these results, when ‘lagged’ by nine months, have been a good predictor of short-term trends in activity.

Figure 2 – Actual transaction levels vs. RICS sales metrics

Source: RICS Housing Market Survey (Mar 2022), HMRC, ONS UK HPI. Note: RICS figures lagged 9 months. RICS and HMRC figures seasonally adjusted.

Rightmove and Zoopla both reported very strong demand in the first quarter, with activity limited only by a lack of available stock. Rightmove’s average time to sell measure fell to 33 days in March (39 in December), the lowest ever figure and half what it was three years earlier. As predicted in Q4, the pace of price growth through 2021 has tempted more vendors to come to market in Q1, but the 12% growth in listings has not kept pace with demand.

Zoopla’s March index reported the flow of new supply was only 3% up on its five-year average, compared to demand 58% higher over the same period. This has resulted in the number of sales agreed being 18% higher but the stock of homes for sale being 40% lower.

House prices

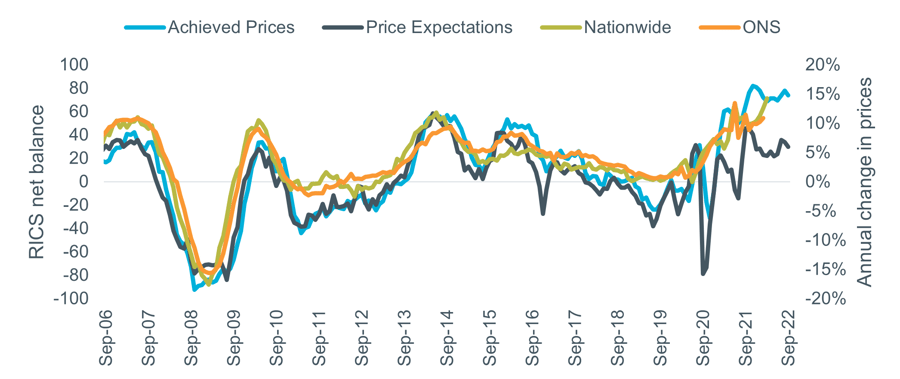

UK house prices grew by 14.3% for the year to March according to the Nationwide December index, the highest rate since 2005. The latest ONS index data (to February) was a little lower at +10.9%. The index results are shown in Figure 3, alongside RICS sentiment survey results.

The RICS net balance for ‘Achieved Prices’ continued at a very high level (+74) in December, extending the run of consecutive months at +50 or above to 19. ‘Price Expectations’ – at +30 in March – are also positive but continue to lag ‘Achieved Prices’, suggesting agents expect price growth to moderate over the next few months.

Figure 3 – Actual value changes vs. RICS price indicators

Source: RICS Housing Market Survey (Mar 2022), Nationwide HPI, ONS UK HPI. Note: RICS data lagged 6 months

Rightmove’s March index recorded a new asking price record, breaking through the £350,000 barrier for the first time, with annual growth at 10.4%. They expect growth to moderate in the second half of 2022 as emerging economic headwinds start to reduce buyer appetite, although they anticipate “demand will still outstrip supply”.

Zoopla also reported very high levels of price growth, with UK values up 8.3% annually. Growth in the first quarter was the highest for 15 years on their index. Their latest market indicators, shown in the table below, indicate the ongoing imbalance between supply and demand. Zoopla continue to forecast growth reducing to around 3% as demand normalises, but they have now pushed this expected reduction back to early 2023.

Table 1 – Zoopla Market Metrics, four weeks to 24/4 vs five-year average

Outlook

The cost-of-living issues highlighted previously continue to grow, and a majority of industry commentators expect them to start to bear down on the housing market later in the year. However, so far in 2022 there has been little to no sign of any negative impacts, despite further increases in the Bank of England base rate in March and May and inflation rising again.

The longer the market continues to defy the wider economic reality, the higher the chances of price falls in the future. The current high levels of demand suggest some buyers are trying to act before prices and mortgages become less affordable, which may make sense at the individual household level but increases the risk of a downturn sooner rather than later.