Commercial market update Q3 2022

Bond yields have settled down, but property yields are exposed to some repricing as investors take into account higher borrowing costs.

The bond vs property yield spread narrows. Although bond yields soared in the wake of the mini-budget, they settled back as a more measured administration took over and remained largely unmoved by the recent Autumn Statement.

Nevertheless, borrowing costs are now markedly higher than six months ago, and property yields are now exposed to some re-pricing as investors take on board these higher costs.

Office: the central theme in this sector is the flight to quality by investors and occupiers alike. Whilst net absorption in Central London is positive, it is prime buildings exerting a positive force on the data. Given rocketing development costs there is a potential opportunity to repurpose some of the better-grade older stock. Vacancy rates remain elevated in most key UK cities and prime yields are starting to shift out across the board.

Retail: this sector was hit hardest by Covid and the cost-of-living-led recession will likely deliver another blow. Weak leasing demand and weak investor interest continues to plague the market, particularly for the high street. A thin development pipeline and more flexible planning allowing switching into alternative uses (often residential) will ultimately result in a smaller stock of retail assets and help prop up the sector going forward.

Industrial: rents and capital values surged this year in response to high levels of demand for occupiers and investors alike. There are signs now that the strong run in this sector is slowing. Rising business costs alongside higher rents are impacting occupier demand which has stalled rental growth. This is a mild pull pack though, not a mass exodus, with the impact on yields also being driven by both the yield gap and higher interest rates.

Key considerations

Higher interest rates are here to stay. Bond yields have receded virtually back to pre-mini-budget levels, but the Bank of England has now raised the bank rate to 3% and indicated there are more rises to come. However, it signalled strongly that rates may not have to rise as high as the markets were expecting, with central forecasts now showing the base rate peaking at 4% – 4.5% next year, while the Office for Budget Responsibility sees rates peaking at 5% in 2024. However, the central bank also warned of a longer-than-expected recession, continuing to late 2024, as it made this latest base rate move.

Expect the commercial investment market to take a breather. Given the recent tumult in the markets, higher interest rates and continuing worries related to the global political and economic environment it is not surprising to see a slowdown already evident in the investment market. There is the potential for a mismatch between vendor expectations and purchasers seeking a bargain in a falling market. Nevertheless, with pricing being rapidly adjusted, there is anticipation of renewed appetite and activity in Q1 2023.

The promising start in the commercial real estate sector in the first half of 2022, with expectations of positive returns for the year, is now being reversed in the second half. For the logistics sector, where there was the strongest performance at the start of the year, there is a fairly sharp correction underway. For the retail sector, there had been something of a bounce in the out-of-town sector, but with the consumer being heavily squeezed the recovery may be short-lived.

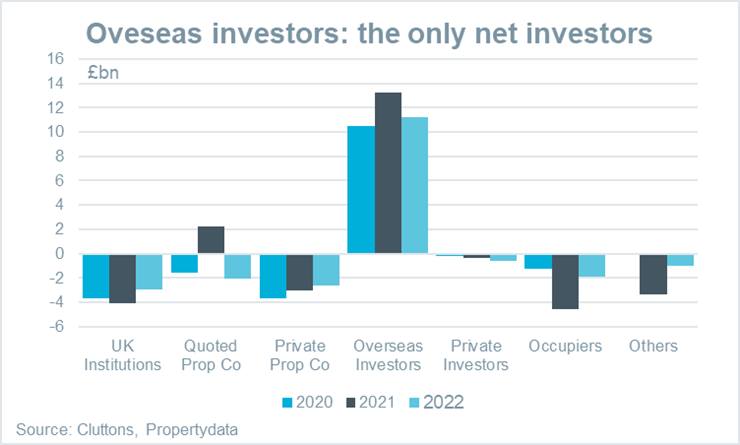

Overseas investors are likely to dominate as UK-domiciled funds and investors exercise a higher degree of caution as they wait to see where pricing settles. Indeed, some investment deals are already being renegotiated, including some portfolio sales. Overseas investors have been dominating the investment market for the last few years and whilst this is likely to continue if there is continued sterling weakness to capitalise on, some are still being cautious in the wake of the wider geo-political and economic uncertainty.

Beware overstated gloom. It is worth recalling that against the backdrop of higher inflation at the end of 2021, expectations were already in place for interest rates to rise. The market has been quick to react in both directions, firstly in the wake of the unfunded tax cuts in the mini-budget and then with the new administration, allowing bond yields and swap rates to settle back – albeit not quite all the way. The prospects for a more stable market in 2023, following the price correction currently underway, will be driven by market confidence and the policies coming out of the administration.

There was also welcome news in the Autumn Statement of extended reliefs for the retail, hospitality, and leisure sectors after business rates revaluations next year. The business rates multiplier will also be frozen for a year from next April.

Looking ahead

It is challenging to find pockets of optimism in the market at present. The misjudged mini-budget created a lot of noise and put the Government under pressure to show how it would balance the books in the recent Autumn Statement. Whilst bond yields initially jumped dramatically in response to the mini-budget, they have since settled down and remained largely unchanged after Jeremy Hunt delivered the Autumn Statement. However, a wider economic and inflationary picture means higher yields and interest rates are here to stay.

And yet, that is not to say there are no opportunities in the current market. Repricing will give rise to opportunities as long as buyers and sellers are willing to be realistic. This could work its way through the market relatively quickly, even as early as Q1 2023. The level of adjustment needed will depend on the outlook for the economy: the Autumn Statement will give more insight into the trajectory the economy is likely to take.

With uncertainty being the watchword for the market at present, it’s worth remembering that reinvention is what property does. To paraphrase 1930s economist Homer Hoyt: “the cycle repeats – but not the same as before”. And certainly, that holds true for each of the main three property sectors currently.

- The office market is re-inventing itself to suit the new hybrid working needs.

- The retail market is adjusting to increased competition from online retail and more flexible planning allowing retail assets to be re-purposed.

- The industrial sector is enjoying the other side of the online retail coin with strong demand taking it into many more urban locations so last-mile delivery can service increasingly instant demand.

There are a wide range of opinions on where the economy will land and what’s in store for the commercial property sectors – and the range is more extensive than at any time in recent history. As the dust settles on the Autumn statement and forecasts from the Bank of England and the Office for Budget Responsibility, more information will emerge to help make the outlook for Q1 clearer.