Industrial market update Q1 2022

The rent rise continues: If the classical economists’ definition of inflation being ‘too much money chasing too few goods’ needed a perfect illustration then the industrial sector is it.

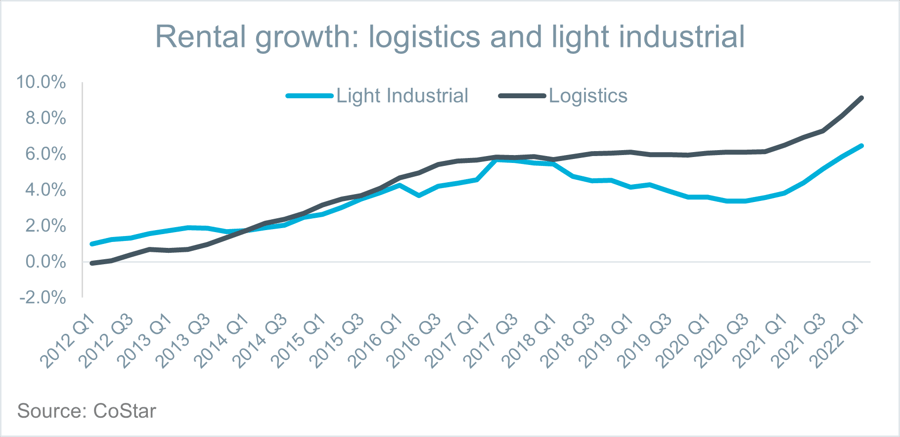

While the growth in the logistics sector has been well recorded, this is now spilling over into light industrial.

Rental growth for the year to end Q1 2022

Rental growth for the year to end Q1 2022 was 9% for logistics and 6% for light industrial. These rental growth rates show no signs of stopping just yet, indeed the quarterly growth rate accelerated to its highest rate in ten years in Q1 for the logistics sector (+2.8%). The simple truth is that yields will likely not stabilise until the outlook for rental growth diminishes, and although some observers report a slight slowing there is little evidence in the data yet. At the end of Q1 industrial yields in the South East had hit 3.0% and with rising bond yields happening simultaneously the yield spread is now just 1.4 percentage points.

Completions fall, construction rises

Completions eased from their mid-2021 peak, but the constant rise of rents has, unsurprisingly driven construction to levels not seen in the past 10 years and so completions will rise again. At the end Q1 there was 83 million square feet of industrial space under construction. With vacancy rates consistently below 4% since mid-2016 there appears to be plenty of capacity to absorb new supply. In the meantime, take up levels will be limited by the amount of available space.

Online retailing still finding its new rate

The proportion of retail sales online fell to 26.0% in March 2022, its lowest proportion since February 2020 at the onset of the Covid crisis. The proportion of retail sales spent online is still trending downwards from its Covid highs (peaked at 37.1% in February 2021) but with such a shift in shopping habits it feels like it is unlikely to go back to prior levels (for the 2 years prior to Covid the average rate was 18.7%). This falling proportion of sales is happening alongside significant faltering in consumer confidence and a deteriorating retail sales outlook.

Amazon profit warning

Reportedly Amazon accounted for a significant slice of logistics demand in 2020 and 2021, estimated to be 20% of the market. In the first quarter of 2022 this fell back to a much lower 3%. A recent profit warning from the group adds to the other emerging data that the online ecommerce boom might be waning.

Occupier margins will be squeezed in 2022 from a range of angles

Overall it is increasingly clear that alongside higher rent levels, occupiers’ margins will be squeezed from a range of angles: inflation driving higher business and operating costs, falling retail sales plus supply chain constraints adding to complexity and delay. This combination of factors makes it seem likely that rental growth prospects for the sector could dimmish over the course of this year (certainly listed logistics operators reacted negatively to the Amazon share warning losing 7-8% in their share price the day after).

| Industrial Q1 2022 | UK | London & South East |

|---|---|---|

Distribution, multi-let estates and specialised industrial | Current quarter (last quarter / 5yr ave) | Current quarter (last quarter / 5yr ave) |

| Occupier | ||

| Availability rate (%) | 5.3% (5.4% / 5.8%) | 6.1% (6.0%/5.7%) |

| Vacancy rate % | 3.3% (3.2% / 3.2%) | 3.8% (3.5%/3.1%) |

| Rental growth (12-month growth rate) | 8.4% (7.5% / 5.8%) | 8.5% (7.4% / 6.0%) |

| Quarterly take up (sqft) | 15.9m sqft (28.3m / 25.6m) | 3.6m sqft (6.5m / 6.0m) |

| Supply | ||

| Completions (net delivered sqft) | 7.3m sqft (9.3m / 10.3m) | 2.5m sqft (1.8m /2.2m) |

| Total under construction (sqft) | 82.8m sqft (78.3m / 50.3m) | 13.8m sqft (13.1m /9.9m) |

| Investment | ||

| Quarterly sales volume £m | £2,119m (£4,915m / £2.667m) | £870m (£1,835m / £946m) |

| Average yield | 3.4% (3.6% / 4.5%) | 3.0% (3.2% / 4.1%) * |

| Prime yield (rack rented) | 3.5% (prime regional) | 2.75% (prime within M25) |

Industrial: Key investment transaction

| Property Address | Town /City | Building size (sqft) | Sale Price (£m) | Net Initial Yield | Buyer |

|---|---|---|---|---|---|

| The Hub, Witton | Birmingham | 252,000 | £52m | 2.9% | Valor Real Estate Partner |

| Halifax Avenue | Lichfield | 397,000 | £60.3m | 3.4% | M7 Real Estate |

| Portfolio | Harlow | 370,000 | £159.5m | 3.0% | Mirastar REIM |

| Lanson Roberts Rd | Bristol | 541,000 | £104.7m | 4.2% | Realty Income Corporation |

| Shrewsbury Avenue | Peterborough | £54m | 3.1% | ICG | |

| Grand Union Park Royal | London (NW10) | 100,000 | £83m | – | SEGRO Plc |

Clouds appearing for the logistics sector?

Overall, it is clear that industrial occupiers’ margins will be squeezed this year not just from high rents. Inflation driving higher business and operating costs, falling retail sales alongside supply chain constraints. This combination of factors makes it seem likely that rental growth prospects for the sector could dimmish over the course 2022 after an incredibly buoyant 2021. Without ongoing strengthening in rental growth prospects, it will be more difficult for investors to justify yields of around 3%. This could well just be a mid-cycle pause for the sector, with long-term structure of increasingly online and on demand retail in its favour.