UK sales review Q2 2022

The UK housing market continued to look strong in Q2 despite higher mortgage rates and the rising cost-of-living.

Annual house price growth remained above 10% and activity was still high relative to pre-pandemic trends, though it slipped back from recent very high levels.

However, the signs of an impending slowdown grew further, with sentiment surveys and data from the portals pointing to activity declining further over the second half of the year. Current expectations are for prices to avoid outright falls, but for the pace of growth to slow.

Monthly data

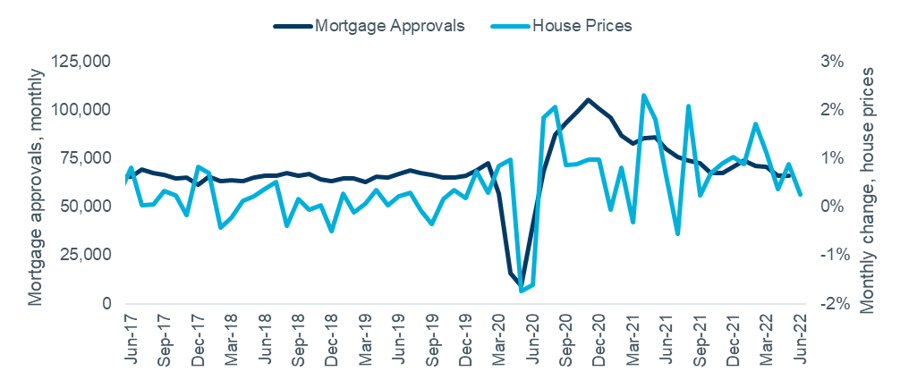

Activity based on mortgage approvals has returned to pre-pandemic trends following two years of volatility. There were 66,000 mortgage approvals for purchase in May, according to Bank of England data, similar to April but 23% down on May 2021. Nationwide reported monthly rises in all three months of Q2, taking the total to 11 consecutive monthly increases. Longer-term trends for both series are shown in Figure 1.

Figure 1 – UK house prices and mortgage approvals, monthly

Source: Nationwide HPI, Bank of England. Note: both seasonally adjusted

Transaction trends

The change in annual sales volumes turned negative in Q2, with the very high figures from Q2 2021 skewing the baseline somewhat. Actual levels of activity fell slightly, with HMRC reporting 303,000 transactions in Q2 compared to 318,000 in Q1. This is the first small sign of a drop off after the stamp duty holiday and other factors stimulated the market in 2020 and 2021.

This slight slowdown is mirrored in the ONS data, which is only currently available up to March due to their lag in reporting completions (note that the latest months are likely to be revised upwards).

Looking ahead, the latest RICS survey results suggest a relatively settled outlook, with perhaps a further small decline in activity. The net balances for ‘Agreed Sales’ and ‘Sales Expectations’ both turned negative over the course of Q2, reaching -13 and -9 respectively.

Figure 2 shows the two survey metrics plotted against the two measures of actual transaction levels. In the past these results, when ‘lagged’ by nine months, have been a good predictor of short-term trends in activity.

Figure 2 – Actual transaction levels vs. RICS sales metrics

Source: RICS Housing Market Survey (Jun 2022), HMRC, ONS UK HPI. Note: RICS figures lagged 9 months. RICS and HMRC figures seasonally adjusted

Commentary from the portals also indicates a market slowing down slightly. Rightmove’s July index report noted the ‘market cooling from boil to simmer’ and Zoopla stated in their May index report that ‘there are signals that the impetus in the market is slowing’.

The actual market data in these reports – inherently more backward-looking – still suggest strong conditions. Rightmove’s average time to sell measure fell to 32 days in June (33 in March) and Zoopla’s demand measure for June is 40% higher than the five-year average, with new supply only growing by 4% on the same basis.

Table 1 – Zoopla Market Metrics, four weeks to 26/6 vs five-year average

| Demand | +40% |

| Sales Agreed | +14% |

| Flow of New Supply | +4% |

| Stock of Homes for sale | -33% |

House prices

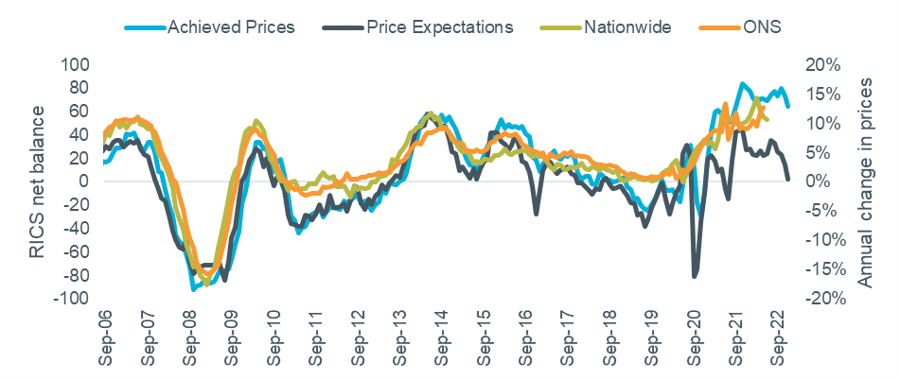

House price growth at national level remained high on an annual basis in Q2. Nationwide’s June index reported a slight slowdown to 10.7% (compared to 14.3% in March) while the latest ONS index (May) in now a little higher at 12.8%. The index results are shown in Figure 3, alongside RICS sentiment survey results.

The sentiment data from agents indicates that growth in values may slow further in the coming months. The RICS net balance for ‘Achieved Prices’ continued at a high level (+65) in June, extending the run of consecutive months at +50 or above to 22. ‘Price Expectations’ declined relatively sharply to +3 in June, the lowest figure since early 2021.

Figure 3 – Actual value changes vs. RICS price indicators

Source: RICS Housing Market Survey (Jun 2022), Nationwide HPI, ONS UK HPI. Note: RICS data lagged 6 months

July saw Rightmove’s index set a record high for the sixth consecutive month, with annual growth in asking prices of 9.3%. The continued strength of the market across the year to date caused them to revise their full year price forecast up from 5% to 7%, with low stock levels supporting values more than previously expected.

Zoopla’s index recorded growth in UK prices of 8.4% in the year to May, but with monthly growth of only 0.1% (the lowest since December 2019) noted that they expect rises to slow in the second half of the year. They do not anticipate any price falls, sticking with the previous full year forecast of 3% growth.

Outlook

Mortgage rates are rising as inflation grows, with the Bank of England responding by raising its base rate. In simple terms this will mean potential home buyers cannot afford to pay current prices, with affordability stretched even further due to other cost-of-living pressures. However, the risk appetite of lenders is another key variable – if they are happy to keep loan-to-income ratios at current levels borrowing will still be possible, just more expensive. If they reduce them, then we could see a stand-off develop between sellers’ price expectations and buyers’ more constrained budgets.

In the event of a stand-off, we might end up with a stagnating housing market. Lower housing market activity might be more economically appealing than a house price correction, but it is not without risk. A stagnating market could have massive secondary effects on the economy that contribute to a recession and eventual price crash anyway. It is not just those businesses directly involved in the house buying process that would suffer but all the other associated spending that comes with buying a home like fitting a new kitchen or buying furniture.