Retail market update Q4 2021

Slide in retail rents halts, but inflation and interest rates pose a threat as cost-of-living bites.

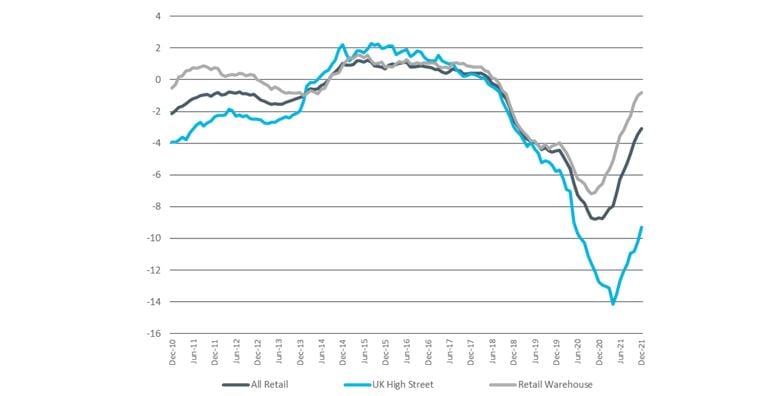

Rents beginning to stabilise

Rents plummeted as the pandemic emptied our high streets and retail destinations. In the final quarter of the year retail warehouse rents improved by +0.1%. Shopping centre rents fell by -0.7% and high street retail -2.3% (3 months to end quarter). Although not yet back into solidly positive growth, rents appear to be stabilising such that it would not be surprising to see growth early in 2022—at least on retail parks which have weathered the covid storm in much better shape than other retail segments.

Figure 1. Retail 12-month rental growth, %

Source: MSCI

Construction levels are low

It is not surprising that construction levels remain low across the retail sector, with less than 1m sq ft completed in Q4 and just 7m sq ft under construction (the overwhelming portion of the latter – 6.6m sq ft – being on the high street). This is well below the 5-year average of 10.4m sq ft; the halted decline in retail rents will need to turn unambiguously positive for new construction to look attractive.

Investment volumes holding up

Overall investment volumes have held up reasonably well (Table 1). For high street retail, the Q4 total of £1.04bn matched the level of Q3—but was still below the 5-year average for the sector (£1.6bn a quarter).

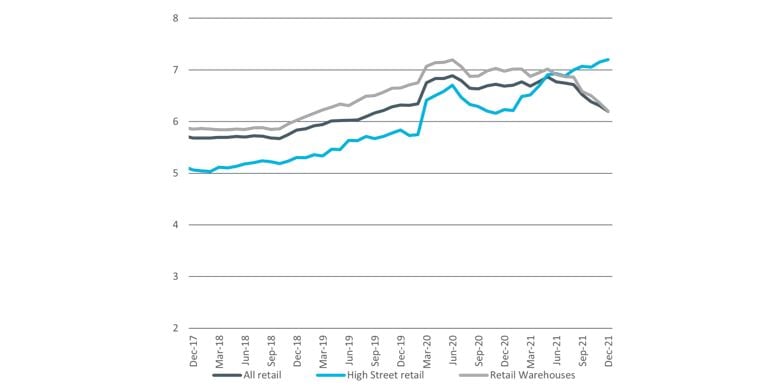

Yields eased a little to 7.2%, but there is still a wide margin above the 5-year average of 5.8%. The rerating in high street yields stands in clear contrast to other parts of the retail sector that have fared better (Figure 2).

Figure 2. Retail yields, %

Source: MSCI

Reflecting the strength of investor interest in retail warehouses, investment levels in Q4 exceeded the 5-year average at £426m, with yields sharpening slightly to 6.2% against the previous quarter’s 6.4% and bettering the 5-year figure (also 6.4%). This may be because retail warehouses offer secure income at a discounted price to sheds as well as potential for repurposing.

Overall, given the rebasing in retail rents and values, there is evidence that investors are starting to see the retail sector in a new post covid light.

Class E threat and opportunity

The introduction of Class E has, for the first time, brought retail within the scope of Permitted Development Rights. PDR has seen many cities lose large amounts of predominantly secondary office stock to residential; Norwich, for example, has lost a third of its office inventory. The thought of this happening to retail would not bode well for the high street.

However, there is evidence that planners will look to actively work with owners who want to switch shopping centres to other commercial uses – be it incubator space, small business and co-working space or creative industry hubs – to protect the vitality of high streets.

Inflation worries

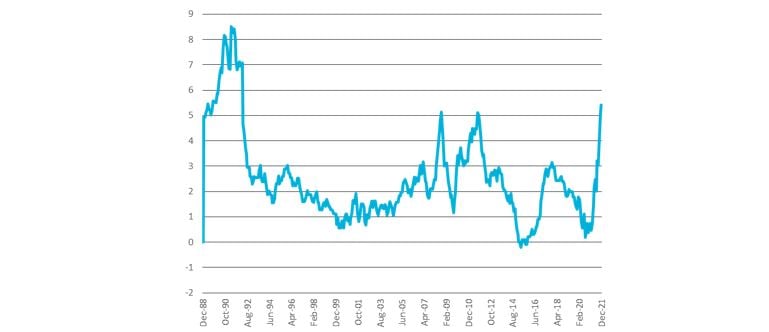

Inflation is back, with some forecasts expecting it to hit 7% during 2022. January 2022 data showed that it had already reached 5.5%. The most direct impact of this will be felt by consumers and, in the context of sharply rising energy costs and rising mortgage payments, the impact on footfall and retail sales could be significant.

Figure 3. Annual inflation, %

Source: Office for National Statistics

There are still high levels of covid related savings in the system that, for certain parts of the market, will help offset cost-of-living constraints. Interest rate rises – of which there have now been two with the likelihood of more – could pose a threat to highly geared investors if long term rates and swap rates rise.

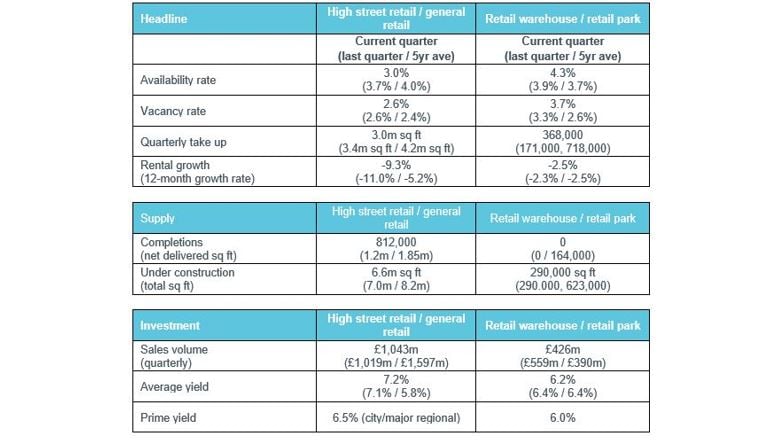

Table 1: Headline market data Q4 2021

Source: Cluttons, Costar

Table 2: Notable investment transactions

Source: Cluttons, Property Data, Costar

Commercial market update Q4 2021

- Overview

- Office market update Q4 2021

- Industrial market update Q4 2021

- Retail market update Q4 2021