Commercial Quarterly Examiner – office market update Q3 2025

Average UK office occupancy continues to push higher and reached a new post-pandemic high of 40.2% in early October according to Remit Consulting’s Return survey which was first undertaken in May 2021 after the first national COVID lockdown ended.

Pre-pandemic, the consensus is that office occupancy typically hovered around 70%. Businesses may have overdone downsizing and consolidation.

A European Office Occupier Survey published this year, found that one in five companies with office expansion plans are looking to increase their footprint due to overcontraction or bigger-than-expected returnto-office numbers.

Those employees who returned to their desks seem to be demanding more comfortable working conditions. A British Council for Offices’ report entitled, “Review of Post- Pandemic UK Office Utilisation” recommended that developers should consider a utilisation rate of 66% rather than the previous 80% benchmark. The occupational density guidance has increased from 12.5m2 per person to 15m2.

Demand for office space grows organically but the rate of growth has recently slowed. The growth of office-based economic output decreased from 0.86% in Q1 to 0.38% in Q2. The annual rate of growth decreased to

1.76% from 2.29% in Q1. Office output has grown at an annualised average of 2.34% since June 2000, outperforming a more broad-based measure of GDP which has grown at 1.55% a year over the same period.

Central London offices Occupational view

- The divergence between new Grade A space and all other space in the market is increasing.

- In the medium term, it is unlikely that the development pipeline will match demand.

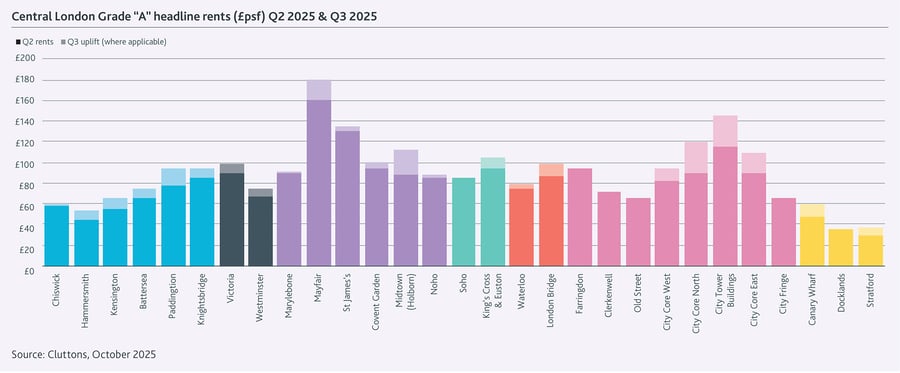

Central London office availability increased in Q3 by 3.0% to 32.1 million sf which represents 28 months’ supply at the post-Covid average rate of take-up. The occupational market for the very best buildings typically called “Grade A” is tighter but availability for the best office space increased by 20% in Q3 to 5.43 million sf. This represents 19 months’ supply.

In the City office market, the availability of Grade A office space in Q3 once again rose above one million sf representing 9 months’ supply. This includes British Land and GIC’s 2 Finsbury Square redevelopment of part of the 1980’s Broadgate office campus comprising 750,000 sf in a 36-storey East Tower and a 21-storey West Tower, linked by a 12-storey podium. The scheme is scheduled to complete in 2027 and is reported to be 31% pre-let.

The most liquid West End occupational markets are the relatively fringe West End locations of Noho and Victoria where there is 27 months’ supply of the best space. In Victoria there are just four Grade A buildings available to let including WELPUT’s 470,000 sf mixed use redevelopment of the former House of Fraser store at 105 Victoria

Street and the net zero carbon redevelopment of a 1950’s office at 11 Belgrave Road where 68,500 sf is available.

In Noho a further three buildings offering Grade A space are available including 156,000 sf at GPE’s Rathbone Square redevelopment of the former Royal Mail sorting office as Meta / Facebook prepares to move to its 620,000 sf Kings Cross campus at 11-21 Canal Reach.

In Q3 a further 315,000 sf of new office space was completed in Central London. So far this year development completions have delivered 1.39 million sf. Demand or take-up for Grade A space averages 868,000 sf per quarter so it is little surprise that rents are increasing for new space.

British Land are reportedly asking £130 psf for space in 1 Broadgate and quoting rents for refurbished space at Paddington Basin have risen to £102 psf. At 77 Grosvenor Street, a building offering a private roof terrace

and pavilion and best-in-class “end-of-trip” facilities (cycle storage, showers etc) located in the heart of Mayfair surrounded by luxury retail, high-end restaurants and extremely well served by public transport has achieved

rents of £220 psf.

In the last five years, ultra low vacancy rates across core City and West End locations have caused exceptionally strong headline rental growth for the best newly developed space in these locations. In the next five years

46 Grade A buildings are scheduled to complete in Central London providing more than 12.5 million sf of office space. But 59% of this space is already pre-let.

Investment view

- Central London office market valuations continue to improve, driven by a continuing strength in the West End market.

- ESG compliance is a growing priority for European investors, pushing development strategies towards retrofitting and sustainability.

After three consecutive quarters of improving conditions, the recovery in London office market valuations slowed in Q3. The Q3 2025 RICS UK Commercial Property Monitor points to a general deterioration in market activity during

Q3 due to the challenging macroeconomic environment. Occupier demand has softened and investment enquiries have declined although feedback suggests London is a little more resilient than Rest of UK markets. Capital value growth decreased from 1.44% in Q2 to 1.02% in Q3 but still representing an annualised rate of 4.1%.

Year-on-year capital value growth improved to 2.99% in September from 1.26% in June.

Performance continues to be driven by the West End which has benefitted from growth of 1.62% in the three months to September and 5.12% year-on-year. Despite growing market rental value growth and strong occupier demand for

Grade A space, City office valuations decreased in Q3 by -0.22%. Across the whole Central London office market capital values decreased by -26.3% between June 2022 and February of this year but have since grown 3.0%.

For European investors, ESG compliance has become a crucial investment criterion. A 2024 report entitled “Emerging Trends in Real Estate” predicts that 90% of institutional investors will prioritise ESG factors in real estate decisions

by 2050. This shift has led to a preference for retrofitting existing assets over new developments, and support for adaptive reuse strategies to achieve decarbonisation goals.

Stanhope, the development and asset manager, and Cheyne Capital, a global alternative investment fund manager, have acquired Row One on London’s South Bank between London Bridge and Southwark Bridge, with planning

consent for a 250,000 sf office tower with 18 terraces overlooking the River Thames, a club room, wellness centre, end-of-trip facilities, bike spaces, showers, and a new public realm. The scheme aims for net zero operation and targets excellent energy efficiency and sustainability in building operation (NABERS UK 5*), supporting occupant comfort, air and water quality, lighting, and overall wellness (WELL Platinum) and exceptional environmental performance across categories like energy, water use, health, transport, materials, and ecology (BREEAM

Outstanding). Rents nearby at 76 Southbank are nearing £90 psf and £100 psf has been targeted at Row One.

A joint venture between Grosvenor and Mitsui Fudosan UK is redeveloping The South Molton Triangle between Brook Street and Davies Street in Mayfair to provide 267,000 sf of office space on eight storeys behind the existing facades and roofs. The design prioritises the reuse of existing materials and structures wherever possible and will aim to reduce carbon emissions generated during construction and throughout the building’s life. Materials used will be designed to promote sustainability throughout the lifecycle of the buildings.

Rest of UK offices Occupational view

- Vacancy rates in major regional office markets doubled since 2020 but the supply of Grade A space has decreased.

- The Government’s continued commitment to the “Places for Growth” program, involving the closure

of London offices and expansion of regional campuses, could act as a much needed catalyst for growth.

Office availability in the South East decreased by -1.3% in Q3 but increased by 2.5% y-o-y, representing more than 4.2 years’ supply at the post-Covid average rate of take-up. Availability across all Rest of UK office markets outside London and the South East also decreased by -0.2 % in Q3 and increased by 3.0% year-on-year representing

coincidentally 4.2 years of supply.

The supply of the best Grade A space has recently become more restricted. Although it is more than twice the level of supply available 12 months ago, South East Grade A availability decreased by -3.1% in Q3 and there is 8 months of supply. Rest of UK Grade A office availability decreased by -8.9% in Q3 and -4.2% y-on-y and there is 28 months of supply.

Headline vacancy rates across all the “Big 6” regional office markets post-pandemic remain elevated. At the end of Q3 2025 the vacancy rate across the UK’s largest regional office markets was stable at 9.8% and ranged

between 7% in Leeds and 11% in Glasgow. However, vacancy rates for Grade A space across all “Big 6” centres is less than 1%. Although overall vacancy rates across South Eastern centres are at a similar high level, limited development activity has left Grade A vacancy rates at just 0.3%.

“Big 6” market rental value growth has decreased to 2.4% in the year to September from 2.9% in the year to June. Bristol remains the strongest regional office market but rental growth has decreased from 6.0% in Q2 to 3.8% y-on-y. However, South East officemarket rental value growth has increased from 0.7% y-o-y in Q2 to 1.1% in Q3.

Development completions of Grade A space in the South East and Rest of UK office markets have been relatively consistent both pre and post-pandemic. Since the pandemic, an average of 12 buildings providing 78,600

sf per scheme have been completed every quarter. However, in Q3 2025 only one Grade A development was completed providing 117,589 sf.

Across the South East and Eastern regions, 2.56 million sf of space is under construction in 39 buildings. This development pipeline is concentrated on Oxford and Cambridge where the 2 million sf under construction

is 18% pre-let. The largest scheme will provide 214,000 sf of space for lab, office and amenity use at Trinity House, Oxford Business Park (OBP). OBP is an 88-acre business park with a strong life-sciences / R&D cluster. Trinity will have 4.4m floor-toceiling heights to enable lab fit-out which typically requires 8 air changes per hour, onfloor

drainage, increased riser capacity, goods lifts, and floor structures designed to provide stability for instrumentation.

Construction activity is lower in the “Big 6” office markets where just 1.23 million sf is being built in 14 buildings, 34% of which is pre-let. Land Securities’ The Republic in Manchester forming part of the Mayfield Park regeneration is one of the latest additions to the pipeline. It will be the first building on the formerly derelict 24-acre site, next

to Piccadilly station offering 325,000 sf office building designed for 2,000 people, targeting completion in 2028. Features of the sustainable building will include a doubleheight entrance, outdoor terraces, a cycle store and RV charging hub.

Investment market

- “Big 6” Regional office investment in the UK has experienced significant volatility in 2025, with a strong rebound in the second quarter after a weak start to the year.

- These “Big 6” markets remain the primary focus for capital allocation but are being challenged by Oxford and Cambridge, alongside several South East towns and other regional cities.

The UK’s major regional office investment markets strengthened in the second quarter when investment volumes increased by 63% to £265 million from £163 million in Q1 but were nevertheless -33% below the post-pandemic

quarterly average of £394 million. Preliminary estimates suggest that investment volumes in Q3 decreased by -46% to £144 million. As usual the latest numbers for Q3 are likely to be revised in the coming months.

Much as expected, Manchester received the largest share of investment in the “Big 6” markets over the last 12 months. Slightly more unexpectedly, Edinburgh and Glasgow accounted for 68% of investment in these markets in Q3; or £98 million out of a total of £144 million.

One of the largest deals in Q3 was the acquisition of Quatermile One, Lauriston Place, Edinburgh by a joint venture between BauMont Real Estate Capital and KZN Real Estate for an estimated £53.85 million. The recently refurbished building, designed by Foster + Partners, offers 123,000 sf of Grade A space. Take-up in Edinburgh’s office market reached a five year high in 2024 and prime rents are forecast to rise driven by a shortage of Grade A office space and lack of speculative development. In late 2024, M&G Real Estate acquired 65% of the issued share capital in BauMont Real Estate Capital which manages €1.5 billion of assets.

The average total return performance across all “Big 6” centres increased to 0.9% in Q3 from 0.5% in Q2 as capital growth improved to -0.9% from -1.1% in Q2. Total returns for the year to September increased to 3.5% from

2.4% in the year to June 2024. Nevertheless, capital values still decreased by -3.2% y-o-y. headline numbers mask significant variance. Occupier market dynamics vary greatly between prime and secondary buildings in most major city centres and consequently, future performance within the office sector is expected to continue to diverge at asset level.

In the 45 months since the end of the pandemic Oxford and Cambridge have started competing with the Big 6 regional centres as destinations for investment capital along with other key South East office in-town and out

of town centres including Reading, Slough and Bracknell in Berkshire; Farnborough and Camberley in North Hampshire; and Guildford and Woking in Surrey. Other cities attracting investment capital include Cardiff, Liverpool

and Newcastle.

Liverpool’s office investment reached £128 million this year, driven by the sales of the Liver and Capital Buildings. The iconic Liver Building is one of the city’s “Three Graces” on the Pier Head along with The Cunard Building and the

Port of Liverpool Building, all built between 1907 and 1917. The Grade 1 listed Liver Building was bought by Princes, one of the UK’s largest food and drinks group, as a head office for £60 million.

The Capital Building on Old Hall Street was built in 1976 and comprises 420,000 sf was acquired by Oval Real Estate for an estimated £56 million with a net initial yield of 11.3%. Having undergone a £26.2 million refurbishment in 2021, it now offers Grade A space with cafes and bars, informal work areas and social and wellbeing spaces. Oval

Real Estate are a private limited company with offices in London, Birmingham and Manchester and backed by US based institutional investors.

Philip Cazenove

Partner, valuation & advisory – head of London commercial

Head office

T +44 (0) 7894 608 075

Richard Moss

Partner, valuation & advisory – head of commercial UK funds

Head office

T +44 (0) 20 7647 7226

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.