UK & London rental market update Spring/Summer 2024

Continued demand for rental property amid constrained supply delivers rental growth.

Highlights

- Gap between supply and demand narrowing, but rents still registering strong growth across UK

- Prime rental growth receding from 2022 peaks as supply rises

- Cluttons forecasts +2.5% rental growth in prime London this year

Prime London rental market

Activity in the prime London rental market remains strong, although the large gap between demand from renters and the supply of property available to rent which characterised the market for much of 2022 and early 2023 has narrowed.

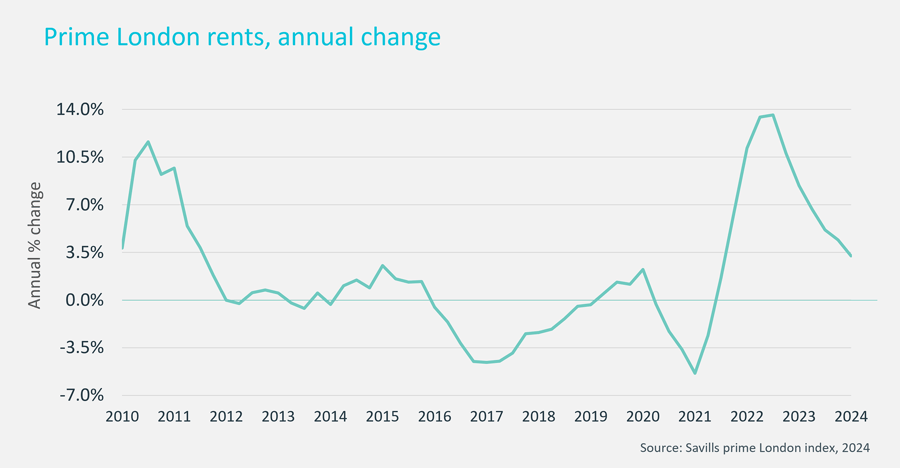

Supply of rental properties is rising, and while demand remains strong, agents also report more price sensitivity among renters. As such, the annual change in rents has slowed to 3.2%, down from 13.6% in September 2022.

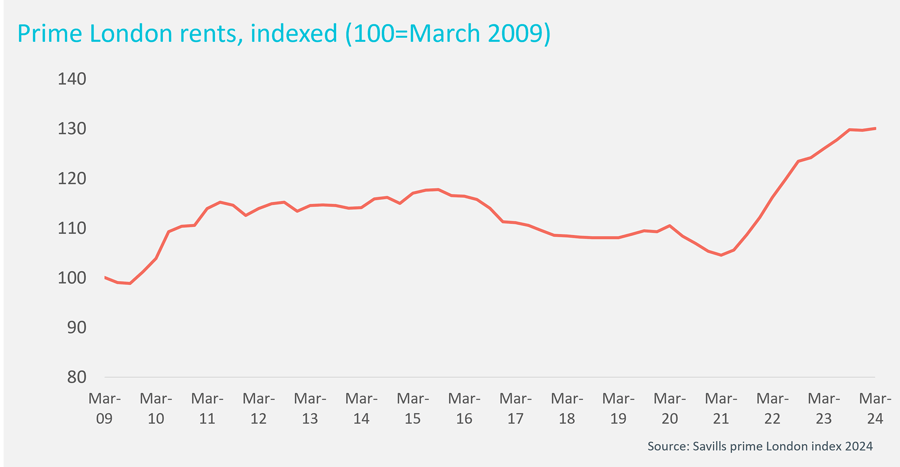

This focus on price and affordability becomes clearer when we look at the cumulative rise in rents since the market low in 2021. Average prime London rents have risen by an average of 25% in the intervening three years. In prime central London, rents have risen 24% since March 2021.

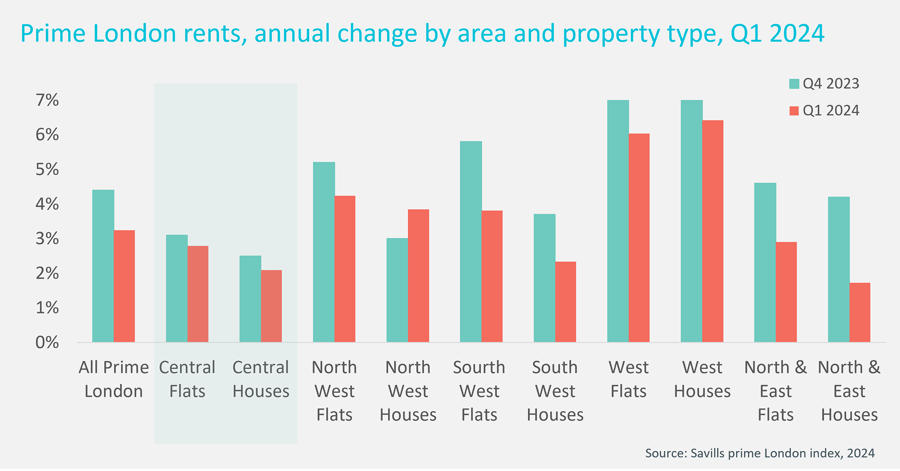

However, after falling by -0.7% in Q4 last year, prime central London rents for apartments rose again in Q1, by 0.6%, taking annual growth to 2.8%. This quarterly movement indicates a return to a more seasonal rental market, as the post-pandemic rental market – which led to consistent high levels of activity amid soaring demand – starts to unwind.

Recent data from Zoopla showed the average available rental stock per agent across the UK was 28% lower this year than in the years leading up to the pandemic. There will be some element of landlords keeping their existing tenants and not listing their properties for rent, but it also illustrates the continuing shortage of rental property. There is now some discussion around whether additional landlords will exit the market given the upcoming changes to legislation, including the renters reform bill. Recent trends demonstrate how a shortage of supply in the face of continuing demand in the most sought-after areas can push up rents.

A change to capital gains tax rules from early April, which means landlords will now only pay 24% CGT on the sale of an investment property, down from 28%, may also encourage those who were considering a sale to make a move. But our prime London agents report that the number of investors putting their property on the market for sale in recent weeks has not been out of line with longer-term trends.

UK rental market

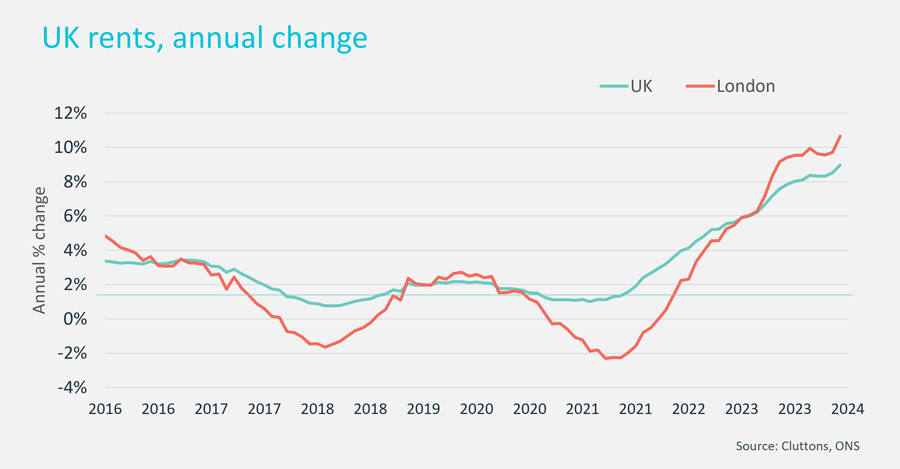

The ONS has widened its survey of rental data to produce a new more and more detailed index of rental prices across the UK. The result is that with more examples of rental data, the average growth rates for rents are higher than previously supposed. The new data shows that UK rents rose by 9.2% in the year to March (on the previous measure, rents rose by 6.2% in the year to January).

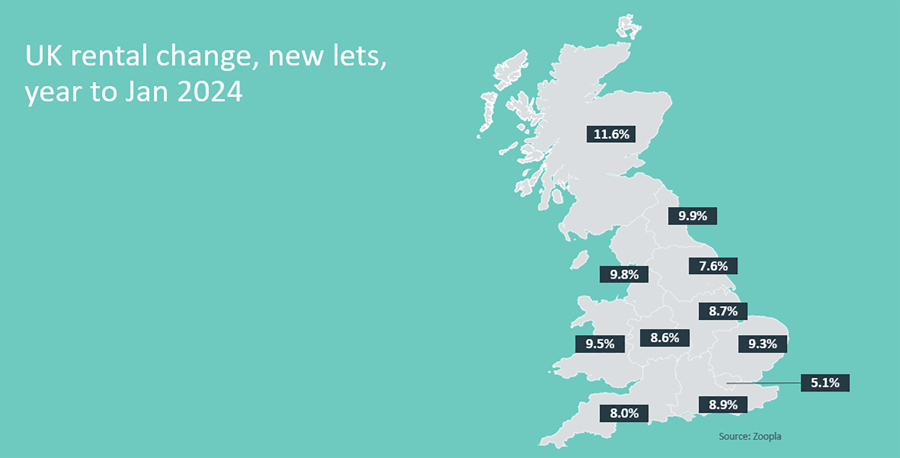

However, other measures of rents across the country signal rental growth is starting to slow, with Zoopla’s index, based on new lets agreed, showing +7.4% growth in the year to January, down from +8.7% in November. The highest rate of rental growth is in Scotland, with an average 11.6% rise in rents in the 12 months to the end of January. This echoes the ONS index which shows rents in Greater Glasgow up by 11.6%, and Edinburgh up by 16.7%. There are indications that the rent controls in Scotland which recently came to an end, meant that landlords increased rents to a greater extent for new tenants, pushing up the headline rate of rental growth.

Across the rest of the country, continued demand amid constrained supply is continuing to put upward pressure on rents. The tax landscape for landlords is becoming more challenging, while, at the same time, high interest rates on home loans mean that potential first-time buyers are staying in the rental market for longer. Agents report that the very high levels of activity have receded since the peak of the rental market in 2022, but that there are still good levels of demand, especially for well-priced rental property. The prospect of lower mortgage rates later this year will as welcome to landlords and property investors as to home buyers.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.