Economic update Spring/Summer 2024

The UK economy has likely emerged from recession, although growth remains muted. Inflation is falling and rates cuts are on the cards this year, which will translate into lower mortgage rates.

Key facts

- Early indications that UK out of recession, but growth will be muted

- Rates will fall this year, but number of rate cuts will depending on UK and world outlook

- Mortgage have receded from peaks last year

The UK grew by 0.1% in February according to the latest data from the Office for National Statistics, and follows 0.3% growth in January. This is hardly stellar growth, but marks a turnaround from falling output at the end of last year and means the country is no longer in recession. Economic growth will still be muted in the coming years according to the Office for Budget Responsibility (OBR), in it’s latest report which was published alongside March’s Budget.

While better economic growth is clearly good news, as it signals more spending, rising job levels and more pay, it also takes away some of the urgency for base rate cuts.

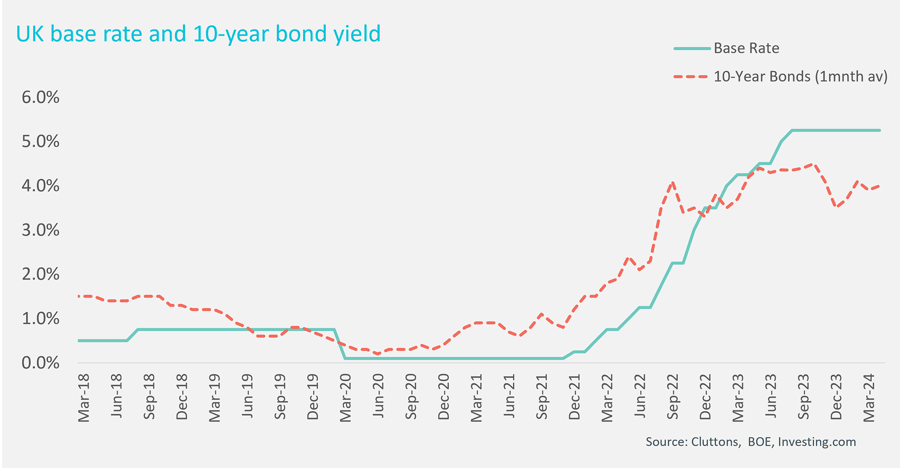

The other key trigger for base rate movements is inflation, and that has fallen sharply since last Autumn. The CPI rate of inflation was 3.2% in March, is tipped to sink to 2.2% this year by the OBR. The Bank of England’s inflation target is 2%. Capital Economics thinks inflation could fall as low as 0.5% later this year and into 2025. Falling inflation means the Bank of England can start to reverse the monetary tightening introduced to try and tackle rapidly rising inflation in during 2021 and 2022 by cutting base rates.

There were expectations at the start of the year that there could be five quarter point rate cuts this year, which would take the base rate from 5.25% to 4% by December. Expectations for this trajectory of rate cuts were highest at the turn of the year, and as a result swap rates fell sharply, and mortgage rates followed suit. Some higher-than-expected wage growth early in the year knocked back those expectations. Wage growth data is closely monitored, as the Bank often highlights concerns that higher wages feeds into higher prices as businesses must recoup the cost of higher wage bills in the cost of their services. As the expectations for the first rate cut moved back to the summer, swap rates bounced back up a little, and as a result mortgage rates have also risen in recent months from the lows in January, but they remain below the peaks hit last year.

There are concerns that the escalating conflict in the Middle East could push up oil prices, and that the UK could follow the US example and see inflation declines stall. Either or both scenarios would mean the Bank of England would have to wait before making any base rate cuts.

Inflation continued to fall in March according to the latest data, dipping to 3.2%. But this was higher than the 3.1% forecast, and money markets saw this as evidence that rate cuts may be pushed back to later in the year. Capital Economics still forecasts several rate cuts this year, but the tone of the Bank of England’s Monetary Policy Committee (MPC) rate meeting in early May will be closely watched, as will April’s inflation data released later in the month. Any rate cuts will be good news for borrowers on variable rate mortgages, and for those looking to take out a new mortgage during the rest of the year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.