Prime London & UK sales market update Q2 2026

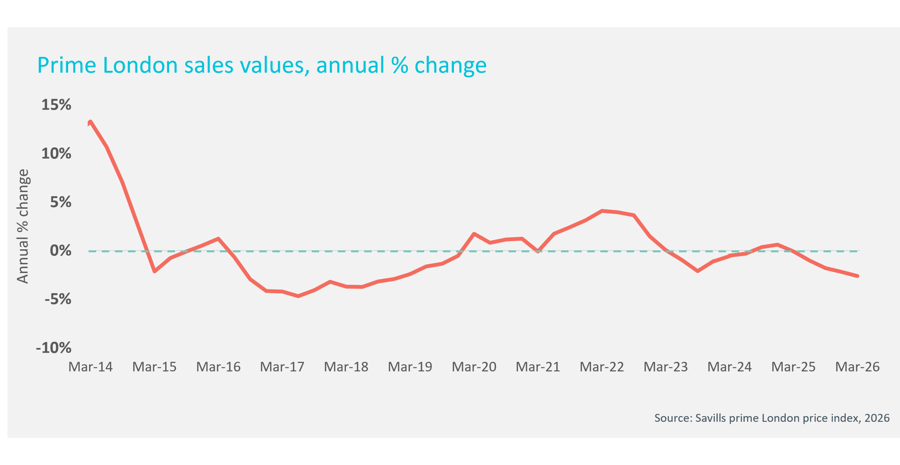

Average prime London prices fell by -2.6% in the year to the end of March, compared to a -2.2% decline during 2025.

However, the scale of quarterly declines has eased since the middle of last year in the run-up to the Budget when widespread speculation on potential tax changes took a toll on the market.

Key facts:

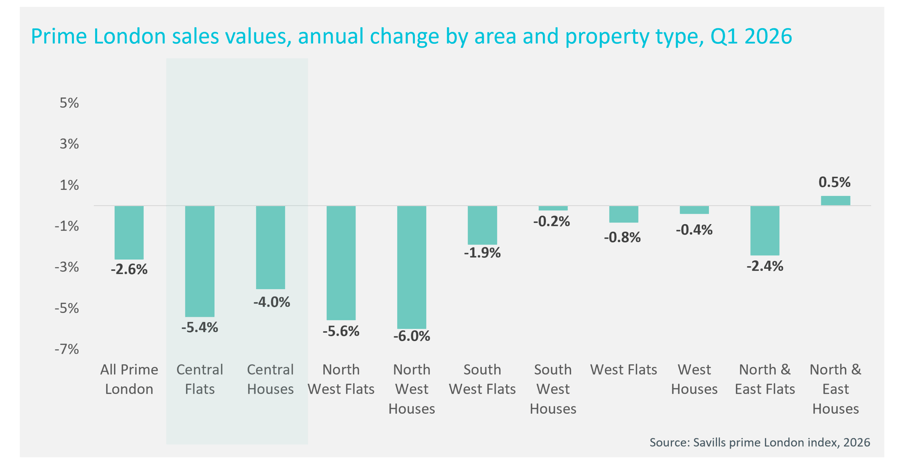

- Average prime London sales values fell 2.6% in the year to the end of March, while prime central London prices were down -4.8%.

- We forecast 1% growth this year in prime London, but the risks to this forecast are to the downside, given the economic backdrop and lack of base rate cuts in the coming months. We will review our forecasts at end Q2

Average prices fell by -0.8% and -0.9% respectively in Q2 and Q3 2025, before declining by a more modest -0.4% and -0.5% in Q4 2025 and the first three months of this year. This underlines that the prime sales market was starting to gain some momentum after the Budget. While the start of the conflict in the Middle East, and the knock-on rise in mortgage rates in March and early April caused hesitation among some buyers, others continued to transact, especially where pricing reflected the current conditions in the market.

Transactions in some parts of prime central London are driven by buyers with higher levels of equity, so while the market may be less sensitive to mortgage rates, it can be more sensitive to sentiment, the policy and tax environment and the wider geopolitical landscape.

In the Budget last year, the Chancellor announced that from April 2028, a Higher Value Council Tax Surcharge (HVCTS) will be introduced on £2m homes, ranging from £2,500 and £7,500. This surcharge is being referred to as a mansion tax, but previous proposals for a mansion tax outlined a tax equal to 1% of the value of the home with no cap. This annual charge capped at £7,500 is a more modest proposition.

This is the latest in a long line of tax changes for London’s highest value homes – from non-dom tax changes to ATED, and pricing has reflected these additional charges. Average capital values in prime central London are down nearly 20% over the last decade. but in the first months of the year, there were signs that the prime central market was bottoming out, with constrained levels of stock for the best homes set to underpin pricing, while some buyers were seeing good value. The current uncertain geopolitical climate may lead to more discretionary purchasers taking a ‘wait-and-see approach’ and lengthen deal times.

Average prices in prime central London were down by an average of -4.8% year-on-year in Q1, with flats falling by -5.4% and houses by -4.0%. However, the scale of declines in prime central London is easing, with average prices for flats down -0.8% in Q1, compared to -2% in Q3 last year. Also, for the first time, the scale of price declines in prime central London has been overtaken by declines in another area in prime London, with average prime values in North West London down -5.8% year-on-year.

We are forecasting +1% rise in prime London prices this year, and flat prime central London pricing. We are keeping these forecasts until a review in the summer, but if the Middle East conflict continues, the risks are to the downside.

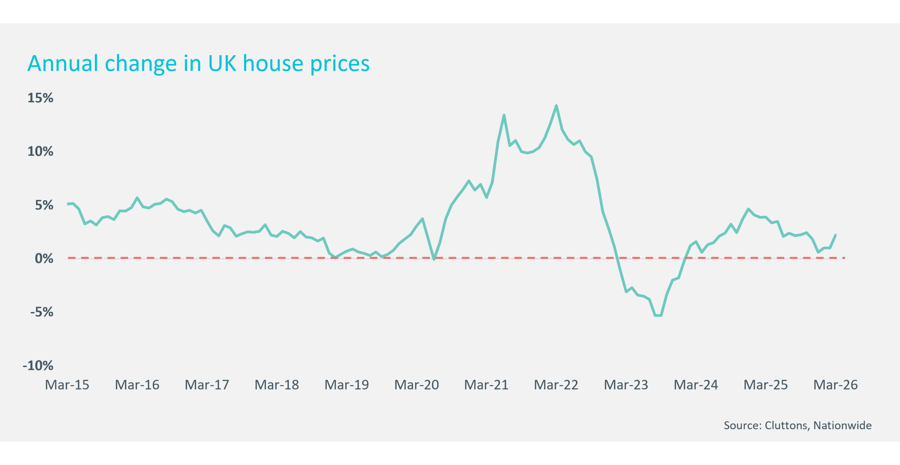

In the wider UK housing market, average price growth ticked up to 2.2% in March, from 1% in January and February, underlining the boost to buyer demand in the market at the start of the year as the forecast interest-rate cuts created a more supportive environment and created improving affordability as mortgage rates started to edge downwards.

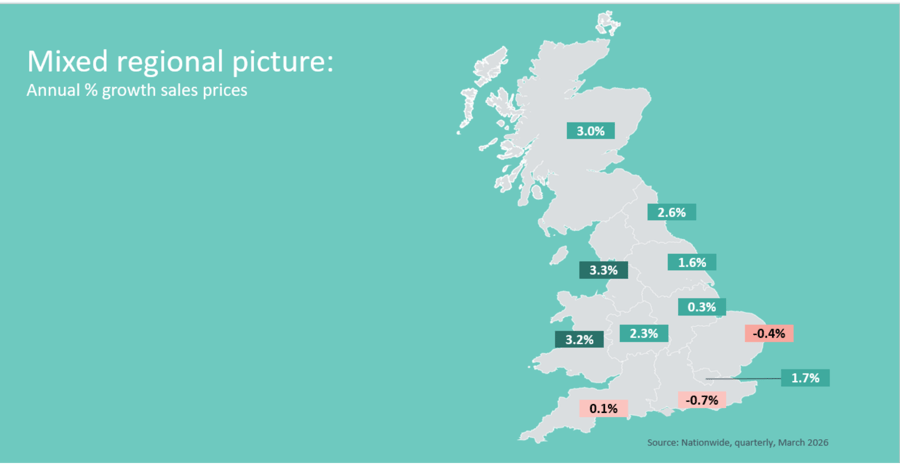

As ever, with the UK housing market, the headline rate of growth tells only part of the story, with markets in the West Midlands, Wales, the North West, the North of England and Scotland registering above average price growth in Q1. Affordability constraints amid higher mortgage rates are taking more of a toll in markets in the South of England, although there was a notable bounce back in annual price growth in Greater London to 1.7%, up from 0.7% in Q4.

However, as examined in the economic outlook, the landscape for the UK and the housing market started changing in March as the conflict in the Middle East pushed up mortgage rates into early April. This softened demand, which could be seen in the RICS housing market survey which showed falling sentiment among agents, and is likely to become clear in the Nationwide house price index in the coming months via lower headline rates of price growth.

Our forecast is for +3% UK price growth this year. If the Middle East conflict continues, the risks to this outlook are to the downside, although pricing will be underpinned by the many households who are locked in to fixed-rate deals and who will not have to deal with higher repayments in the near-term.

Forecast:

| Year | UK House Prices (Q4) | Prime London prices | Prime central London prices |

|---|---|---|---|

| 2025 | +1.7% | -2.2% | -4.8% |

| 2026 | +3.0% | +1.0% | +0.0% |

| 2027 | +3.5% | +2.5% | +2.0% |

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.