Surprises were few and far between in one of the most-leaked Budgets in recent decades. The Budget confirmed additional spending, and a range of largely back-loaded tax rises to deliver an extra £26 billion in annual revenue for the Treasury by 2030.

Property owners and investors were once again in focus, although some of the specific property changes announced by Rachel Reeves (examined below) will not be introduced for several years.

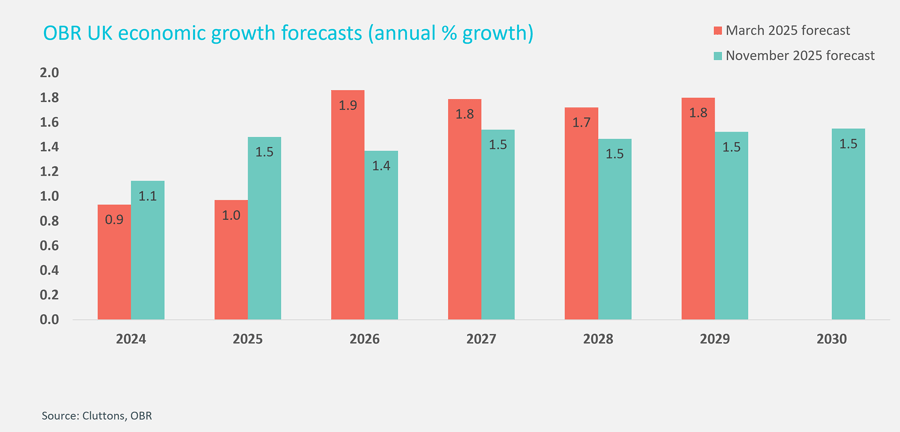

These changes come against a background of rising income tax and staid GDP growth, as the Chancellor announced an extension to the freezing of thresholds to 2030. The Office for Budget Responsibility (OBR) revised up its forecast for economic growth this year, but then downgraded its forecasts for economic growth every year from 2026 – 2029. (see chart at end). The money markets have initially responded positively to the Budget however, signalling better news for the cost of borrowing.

If you would like to discuss the measures below or any other Budget announcements that might affect your property or business decisions, please contact our experts.

Key changes for property

Higher Value Council Tax surcharge (HVCTS) on homes valued at £2 million or above.

This surcharge will be added to Council Tax bills in England and Northern Ireland, but it will be Council Tax in name only.

More will become clear when the consultation is published early next year, but it seems this will be an additional layer of tax for homeowners and landlords of assets worth £2m+ who will be liable to pay the surcharge (when homes are rented out, it is renters who are usually liable to pay Council Tax). The receipts from the tax will be funnelled from Local Authorities straight to the Treasury. The charges will rise by CPI inflation each year after being introduced.

The tax change will come into force in April 2028, after a large revaluation exercise by the Valuation Office Agency (VOA) – and property values will be based on values in 2026. The consultation will focus on reliefs, exemptions and deferrals for those who can’t meet the annual cost. The move was expected to raise £600 million a year by the OBR, but they reduced this forecast income by a third to £400 million due to capital values coming down in line with the new charges – pushing more properties into lower bands, and the reduced stamp duty receipts and capital gains tax (CGT) that will also result from this. The change will also distort the market above £2 million, creating cliff-edges as properties are ‘bunched’ below the thresholds.

| Property value threshold £m | Higher Value Council Tax Surcharge (annual) from April 2028 |

|---|---|

| £2 million – £2.5 million | £2,500 |

| £2.5 million – £3.5 million | £3,500 |

| £3.5 million – £5 million | £5,000 |

| £5 million + | £7,500 |

Laura Dam Villena, Head of Residential Agency, says: “After months of speculation, one more positive outcome is that the certainty provided by the Budget announcements will release some pent-up activity in the prime London market. Our teams are speaking to buyers, sellers and landlords who now want to take their next step, with multiple offers made in the last 24 hours. Prime central London prices have already fallen 20% over the last decade because of a raft of rises in taxes, stamp duty and other policy moves. Yesterday’s move will trim another margin off pricing for homes in the £2m+ bracket, homes which are mainly clustered in London and the South East as buyers factor it into their calculations. The effects of the new charges may be amplified closer to the 2028 start date, as those sellers keen to avoid the charge bring more homes to the market.”

Additional 2% tax on property income

The Chancellor announced that she had stuck to the Labour manifesto by not raising income tax, VAT or National Insurance. Yet in the same speech, she announced a rise in tax on income from property, savings and dividends.

The income tax rate for income from ‘letting land and buildings’ will rise by 2% from April 2027. This will take the basic rate from 20% to 22%, the higher rate from 40% to 42% and the additional rate from 45% to 47%.

The 2% rise for all income from property, savings or investments mean that property investors are not being singled out, but the change comes just a year after landlords will have adjusted to the introduction of the Renters’ Rights Act in May. The OBR has cautioned that the additional tax move could prompt more landlords to sell and restrict rental supply, which would drive up rents. Alternatively, some landlords with a portfolio of properties may choose to incorporate into a company structure.

Laura Dam Villena says: “We have already seen a sharp rise in the number of landlords asking us to value their property for sale as well as for rent when a tenant leaves, and a higher proportion of landlords are then choosing to sell their property. If this additional cost prompts more investors to leave the sector, a lack of supply in the market could actually drive up rents, which will be challenging for renters and for policymakers.”

Business rate multipliers

The business rate multipliers were cut in the Budget, but the rating list published soon after signalled some substantial rises for some ratepayers.

The new business rate multipliers coming into force in April next year will fall substantially from their current levels. Larger properties will see their multiplier reduce from 55.5p to 48p. Smaller properties, with a rateable value of less than £51,000, will see a reduction from 49.9p to 43.2p. For properties with a rateable value of more than £500,000, there will be a surcharge of 2.8p.

Some transitional reliefs will be introduced to mitigate these rises, but this will still allow for 30% increases in rates on some properties worth more than £100,000.

However, there are more generous reliefs available for properties in the retail, hospitality, and leisure sectors.

Gareth Buckley, National Head of Rating, says: “The Chancellor’s announcements on business rates were not as draconian as originally feared, but the rating list published after the Budget has a sting in the tail for some ratepayers. The reduction in multipliers is very welcome, but the new rating list is a mixed bag, meaning that some properties will see a large rise in rates from April next year.

“The landscape is slightly brighter for those in the retail, hospitality, and leisure sectors. The 40% relief currently available to these businesses has a cash cap limit of £110,000 per business. But from April, this limit will be removed, allowing them to benefit from the relief across their whole portfolio, a move which will be of particular benefit to companies with large property portfolios.

“The Government are consulting on empty rates as well as other measures, which leaves the door open for tinkering on empty rates management. The consultation closes in February next year, but this is not the first consultation on this complicated issue.”

Economic landscape

The ‘smorgasbord’ approach to tax rises, from additional charges for EV vehicles to a national insurance tax rise for pension contributions, means the Government will create a fiscal buffer if all the tax changes deliver receipts in line with forecasts. However, the Chancellor has not confirmed that she won’t need to introduce more tax rises next year, which raises the question about whether a bolder, simpler, tax rise in the Budget could have been an option to boost revenue for the Treasury.

The OBR has downgraded its forecast for economic growth in the UK over the coming years, which again raises the question whether a single, larger move would have created more of a platform for stability for businesses to invest, helping promote economic growth.

Commenting on the Budget, John Gravett, CEO, says: “The Government’s main priority is finding economic growth, and we need to pull all the policy levers for businesses to deliver it. This Budget, with a smorgasbord approach including more charges on pension contributions and coming so soon after the National Insurance rise for employers, risks creating a landscape where it is harder for businesses to expand and to recruit new talent. The OBR has revised down its forecasts for economic growth from next year, raising the prospect of more speculation around additional tax changes, potentially creating inertia as businesses delay strategic decisions

“There is an argument for the Chancellor to have been bolder around income tax, to silence all questions around the fiscal black hole and create a workable buffer that would then create a landscape offering policy certainty which would generate momentum for business growth across the country and much-needed investment in national infrastructure.

“On property taxes, the delayed introduction of a complicated Higher Value Council Tax Surcharge which introduces four cliff-edges in the £2m+ market suits the Chancellor as she balances her books. Yet this tax will impact receipts from stamp duty and capital gains tax, as the OBR has acknowledged. The total sums raised also have to be balanced against a large piece of valuations work, which will likely throw up some interesting findings in the consultation, something we will be monitoring closely.

“Raising tax on rental income when the rental sector is doing a lot of heavy lifting in providing homes while housebuilding levels are so low against the Government’s 1.5 million target, seems like a confusing move at this stage.”

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.