Economic update Q2 2026

There was a promising start to the year, with expectations of more rate cuts boosting sentiment in the prime London and wider UK sales markets. However events in the Middle East, which caused a surge in oil prices and gilt yields has put a brake on the market.

The question now is how long the conflict will last, as the longer it goes on, the bigger upward pressure on inflation, which will minimise the chance of any base rate cuts and raise the spectre of rate rises. Meanwhile the rental market is now into a new era of the Renters’ Rights Act.

Key facts

- The outlook for the UK economy, and residential sales markets are being shaped by the conflict in the Middle East, and the knock-on impact this disruption is having on oil prices and gilt yields and the cost of borrowing

- The Bank of England held the base rate at 3.75% at the end of April, even in the face of rising inflation and rising fuel prices due to the Middle East conflict. We expect the base rate cuts anticipated at the start of the year to be delayed until much later in the year, if not next year. But if the conflict continues to limit oil supply into the summer, there is a risk central banks will look to respond to rising prices by starting to raise the base rate

- The Renters’ Rights Act came into force on May 1st, the biggest change to the rules around renting in England in a generation. Some landlords have exited the market ahead of the changes, and the start of an additional 2% uplift in income tax from April 2027. Rental demand remains strong, which will put upward pressure on rents

- The risks to our forecasts in the UK and prime London sales markets are to the downside, especially if the Middle East conflict continues. We will review our forecasts at end Q2

The UK outlook over the next year is being determined by the conflict in the Middle East, and especially the disruption to shipping in the Strait of Hormuz, which is the route by which 20% of global oil and Liquified Petroleum Gas (LPG) travels. This downturn in delivery of oil and LPG has pushed up energy prices and inflation rates around the world – and the uncertainty over the outlook has pushed up UK gilt yields and, ultimately, mortgage costs.

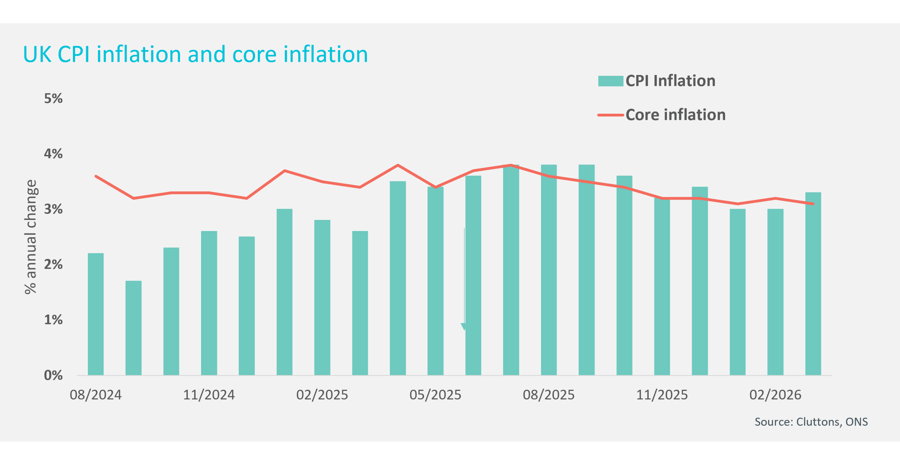

CPI inflation rose to 3.3% in March 2026, up from 3% in February, with motor fuel accounting for much of the increase. Analysts are not expecting inflation to reach double-digit figures as it did after the Russian invasion of Ukraine in 2022, however, the longer the Middle East conflict continues, the more upward pressure there will be on pricing, as the ripple effect of higher oil prices filters through to a range of goods.

The Bank of England kept Bank Rate on hold at 3.75% in March and April as it ‘looks through’ the inflationary impact of the conflict, but if it continues into the summer with no sign of a permanent ceasefire or the Strait reopening permanently, then there will be increased pressure to consider rate rises. The next rate decision is on June 18th. This pressure would be particularly acute if wages start to climb in response to higher inflation expectations. However, if the blockade for shipping is lifted, and flows normalise, gilt yields and mortgage pricing should ease, supporting confidence and activity. Even then, the inflation shock would not disappear overnight, but it would increase the likelihood of rate cuts towards the end of the year and into 2027.

The UK 10-year gilt yield has climbed from 4.3% at the beginning of March to around 4.9%, while the five-year swap rate, the money market rates which determine the cost of fixed-term lending, spiralled from 3.8% to 4.8% in the first weeks or March. As a result, mortgage lenders raised their lending rates throughout March and the start of April. Since then, swap rates have receded a little, and some larger lenders have started to trim their rates as they compete for additional custom. While the outlook remains uncertain in the Middle East, the mortgage rates will likely be more volatile than usual, so buyers who spot a good deal should move quickly.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.