Economic update and Residential Forecasts Q1 2026

The Budget provided clarity on the tax landscape for homes, with two major announcements coming into force next year and 2028. This was enough to release pent-up demand into the market after months of speculation dampened activity.

Key facts:

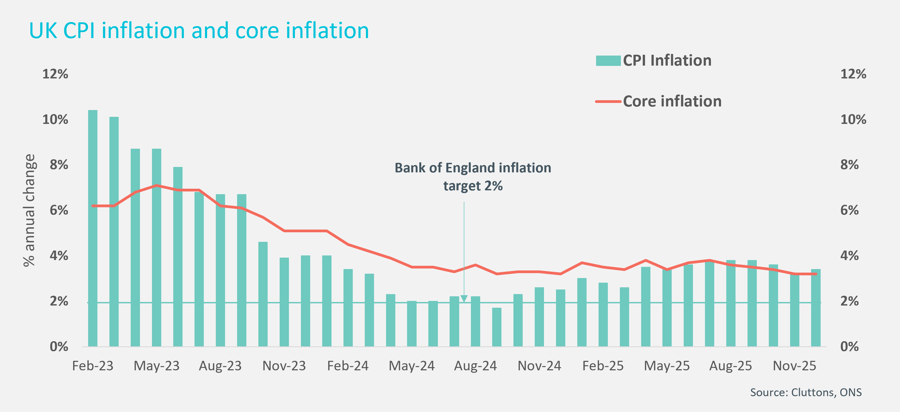

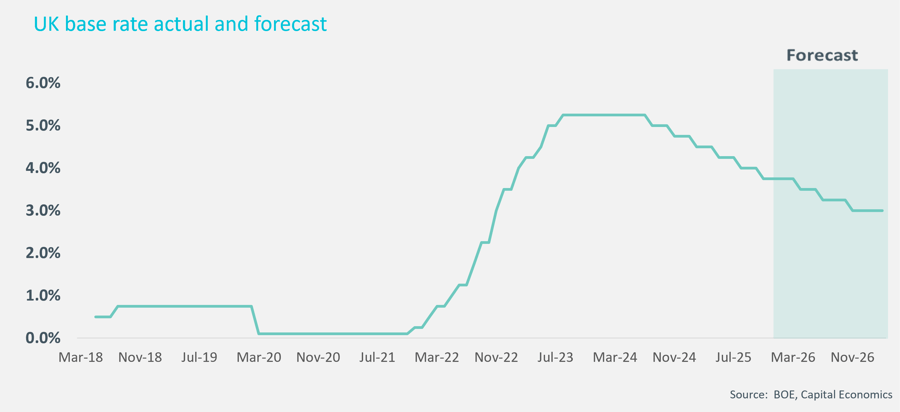

- The Bank of England cut interest rates to 3.75% in December, and we expect rates to fall to 3% by the end of the year as inflation continues to recede towards 2% target

- We forecast cumulative growth of 3.5% in Prime London sales pricing by the end of 2027, and 2% growth in prime central London, while we expect 6.5% growth in the wider UK homes market

- In the rental market, we expect 3% rental growth this year and 3.5% next year in average UK rents, with 3% annually in Prime London, and prime central London rents climbing from 2.5% this year to 3% next year.

UK economic update and prime residential focus and forecasts

The economy grew at a slightly faster-than-expected rate in the three months to November, registering 0.1% growth, after no change in the three months to October. If this trend continues into December, the UK would achieve 1.4% annual GDP growth in 2025. However, the more challenging wider economic landscape, including a continued drag effect from higher inflation and higher taxes mean that the outturn this year will still be muted, with growth of between 1% to 1.4% currently forecast.

This lower rate of economic growth means that the path is clearer for the Bank of England’s rate-setting committee to continue to cut interest rates this year, after making six quarter point cuts since rates peaked at 5.25% in 2023/2024.

Further rate cuts are also dependent on inflation rates, but despite a slight tick-up in December, it is widely expected that inflation will continue to recede this year towards the 2% target amid moderating energy prices and easing wage growth.

This means the Bank’s Monetary Policy Committee will likely vote to cut interest rates several more times this year. While February is looking unlikely for the first rate cut, odds are rising that rates will be cut to 3.5% in April. We expect rates to be cut to 3% by the end of the year.

Gilt yields fell during October to the lowest rate in nearly a year, but have since bounced up again amid the geopolitical and economic uncertainty from the US’s changeable announcements on potential tariffs. Even so, competition for business among mortgage lenders means they are chipping their rates, driving down their rates for consumers – in effect locking in some of the base rates cuts early.

November’s Budget announcements made two major changes for residential property. The introduction of and additional 2% income tax charge for residential landlords from April next year, and a Higher Value Council Tax Surcharge (HVCTS) on £2m homes, ranging from £2,500 and £7,500. This surcharge is being referred to as a mansion tax, but previous proposals for a mansion tax outlined a tax equal to 1% of the value of the home with no cap. This annual charge capped at £7,500 is a more modest proposition. Although it is called a Council Tax, all the receipts will go straight to the Treasury. The move is expected to raise around £400 million a year. The impact will be felt most by homeowners in the higher value markets in the South of England including prime London. Looking for more information? Read our latest sales forecast and rental forecast, or explore our residential services below.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.