Prime London & UK sales market update Q1 2026

As we highlighted in our previous report, the certainty provided by the Budget acted as a trigger to release demand in the prime London market that had built up during months of speculation about high value property tax changes. There was a bump in activity in December and into the New Year.

However, wider headwinds mean that this rise in activity is not putting upwards pressure on pricing as would be expected in usual market conditions. The market is still absorbing policy and wider tax changes introduced in recent years, with the prime central London market particularly affected by the changes to the non-dom tax regime. As a result, while deals are being done, average pricing is back to 2021 levels, while in prime central London it is back to 2011 levels. There are signs that price falls are bottoming out and we expect this to translate into a modest uplift in average prices across prime London market this year.

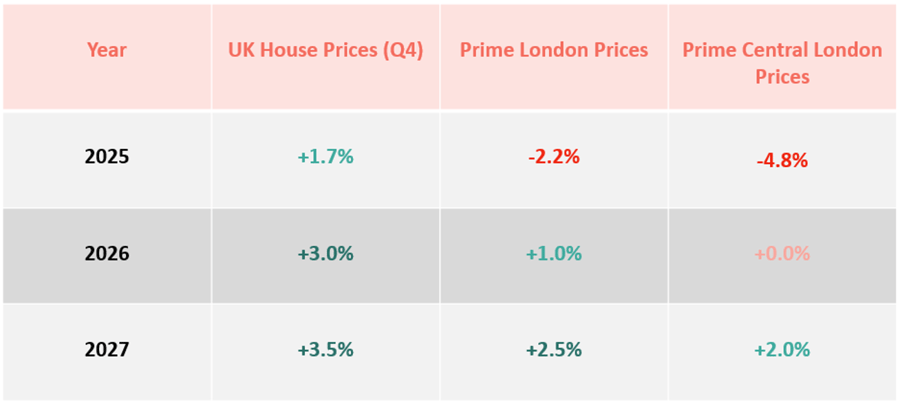

- Average prime London prices fell -2.2% in 2025, with values in prime central London down -4.8% on the year, and around 23% over the last decade

- Average UK prices growth moderated to +1.7% in Q4 compared to Q4 2024

- In Prime London, we expect 1% growth in 2026 and 2.5% growth next year, however in the central prime London market we don’t expect any growth until next year, while in the wider UK market, we expect average price growth to rise to 3% in Q4 2026.

Source: Cluttons

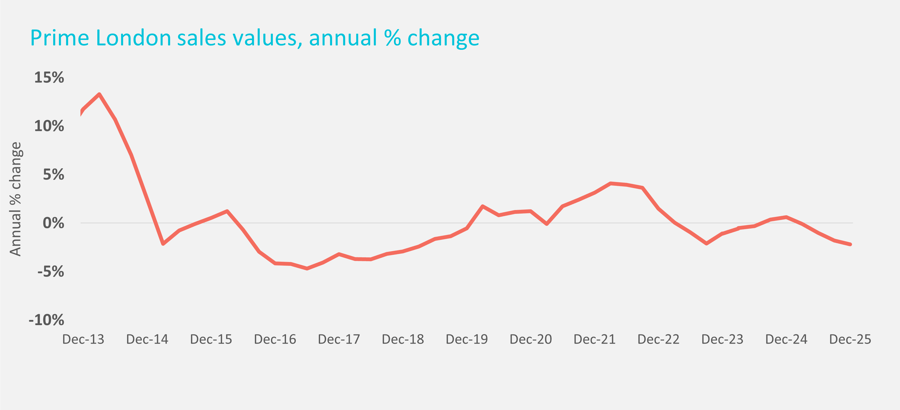

Average prime London prices fell by -0.4% in Q4, a more modest decline than the -1% fall registered in the three months to the end of September. Even so, prices were down -2.2% on the year, largely in line with our forecast for a decline of -2%. This fall comes after a 0.6% rise in 2024, and a -1.1% fall in 2023.

The declines in prime pricing are in some part due to the market continuing to adjust to new tax rules affecting demand. An additional 2% was added to the 3% surcharge for the purchase of additional homes or investment properties from October 2024, meaning that those buying such a property now pay an additional 5% surcharge on top of the basic stamp duty charges. Properties worth more than £1.5 million attract stamp duty on any value over and above this at 12% for homemovers, but 17% for those buying a second home. Buyers are factoring this additional cost into asking prices, so capital values are adjusting.

In May last year, the final stage of the change in the tax regime for residents not domiciled in the UK for tax purposes came into force, which has prompted a significant number of non-doms, including some very high profile business leaders, to relocate away from the UK. This has particularly affected the highest-value markets in prime central London. The policy changes introduced for landlords and investors, examined in more detail in the rental update, are also reducing demand in the high value market from investors and landlords.

However there has been speculation that the Government is now examining the opportunities for a wider-ranging investment visa which could open the way for more non-doms keen to be based in the UK could return.

The Budget, the focus of so much speculation for months last year, sparked a flurry of offers and exchanges as soon as it ended on November 27th. The fear of a 1% mansion tax was allayed, and while Chancellor Rachel Reeves did announce a new tax on high value properties, it will range from £2,500 to £7,500. She also mentioned workarounds for those unable to meet these annual payments – and the market is now waiting for a consultation which the Government has stated will be launched in ‘early 2026’. Although the Budget included the plan for this new tax, along with a new 2% income tax surcharge for landlords from April next year, the certainty provided by the detail of these moves was enough to release demand.

We expect price rises to remain muted across the prime London market this year, with an uplift of 1%, while in prime central London we think prices will end the year largely unchanged. However, as interest rates continue to fall and as price recalibrations start to offer value in the market we see price growth starting to build modestly in 2027.

UK housing market

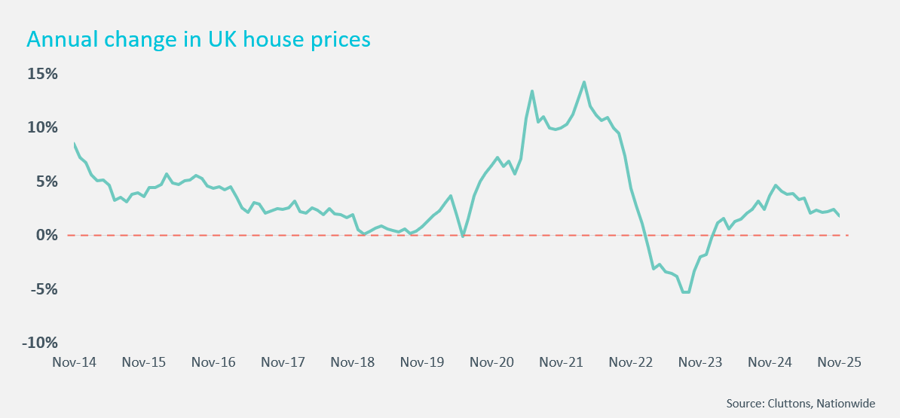

Average house prices fell by -0.4% during the month of December, and year on year prices were up 0.6%, although this rate reflects a sharp uptick in pricing in December 2024. On a quarterly basis, home values were up 1.7% in Q4 compared to Q4 2024.

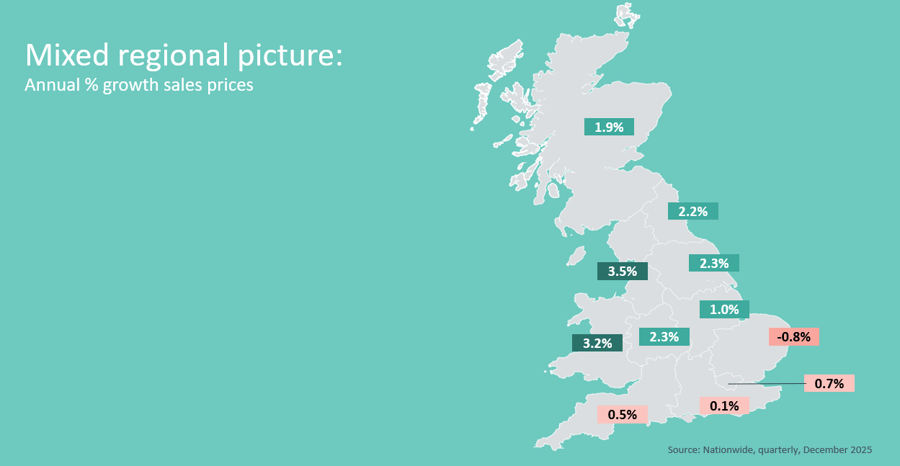

Housing markets in the Midlands and the North of England are still seeing stronger price growth than the rest of the country with 3.5% annual growth in prices in the North West year-on-year. This trend will continue into 2026 as these more affordable markets continue to benefit from falling mortgage rates during the year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.