Prime London & UK sales market update Q4 2025

Stories started to emerge in August that the Chancellor was considering introducing or raising property taxes in the November’s Budget, especially for more expensive homes.

Creating uncertainty in the market in the four months leading up to November 26th has had an easily predictable and entirely understandable effect – acting as a brake on transactions as some buyers and sellers choose to wait for more information. The certainty provided by the Budget could spur activity in the New Year as the market absorbs the changes and adjusts accordingly.

Key facts:

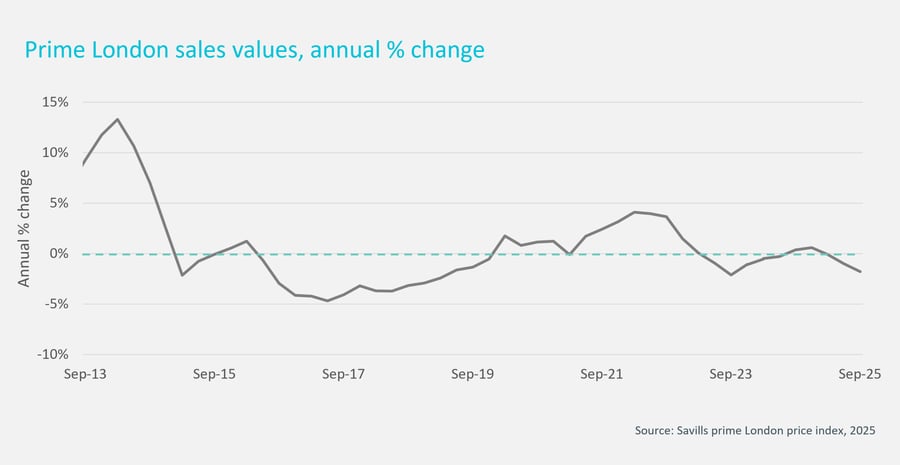

- Average prime London prices fell -1% in Q3, and are down -1.8% year on year

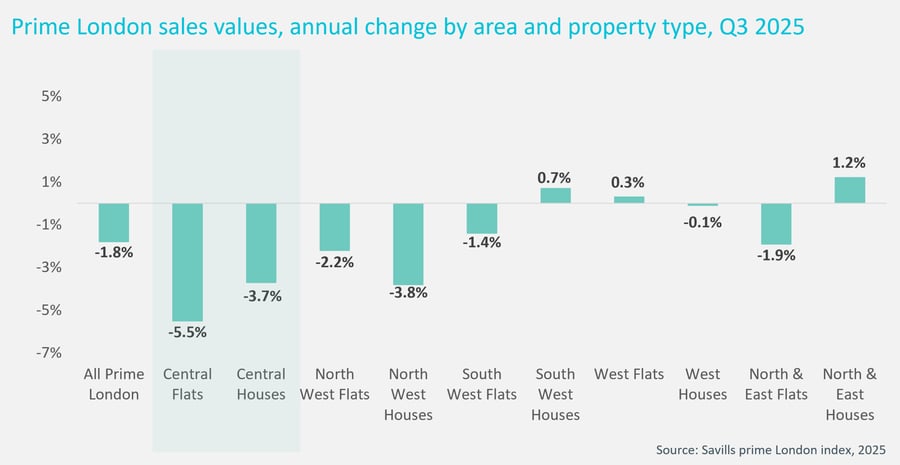

- In prime central London, average values are down by -4.6% on the year, with flats sliding by 2% in Q3

- Prime London transactions were 20% down in Q3 compared to the same period last year

Average prime London prices fell by 1% in Q3, the largest quarterly decline since Q4 2022 when interest rates had jumped by 3% in a year and Liz Truss had just delivered her ill-fated emergency Budget. The declines in prime pricing are in some part a continuation of the trend which started a decade ago as the market continues to adjust to new tax rules affecting demand. Most recently the changes to the non-dom rules, which came into force in April, has prompted some residents to move away from London. This tax change came sharp on the heels of another stamp duty rise for additional properties in October 2024.

Another factor spurring the downward movement of pricing, especially in prime central London, has been the uncertainty engendered by months of speculation on potential property taxes that could be introduced at the Budget.

We examine these more fully in our Budget blog but the current contenders, which have all featured as stories in the press, are: an annual tax on £2m+ properties referred to as a ‘mansion tax’; applying CGT on the sale of primary residences; scrapping stamp duty and Council Tax and replacing them with a graduated annual tax on the property; raising Council Tax for higher band properties.

Recent reports suggest this is emerging as the favoured option, and the higher charges will be levied for homes in bands F, G and H. These bands are still based on house price values in 1991, so the thresholds in today’s values will differ depending on house price growth regionally and locally since then. But this could affect some residents in Bank F who have homes worth more than around £600,000, although in some local authorities this value will be higher. The starting value of a home in band G is roughly £750,000.

It is likely the Chancellor would only choose to implement one of these ideas, or two at a push. The pressure on property to deliver tax revenue will have been eased significantly since early November as it also seems the Chancellor is considering raising the rate of income tax by 2p. While this would be offset by proposed National Insurance cuts for those earning up to around £45,000, such a move would raise billions.

Uncertainty in the market will be higher than usual until the Budget is over, and while activity has fallen, it is worth emphasising that transactions are continuing, especially for well-priced best-in-class properties. The draw of London remains strong, and a rise in buyers from the US is off-setting an easing in demand from other parts of the world.

We are still expecting prime London prices to decline by -2% this year. Much of next year’s price performance will depend on the Budget announcements, but we are forecasting a lift in activity, especially if there is another base rate cut in December.

UK housing market

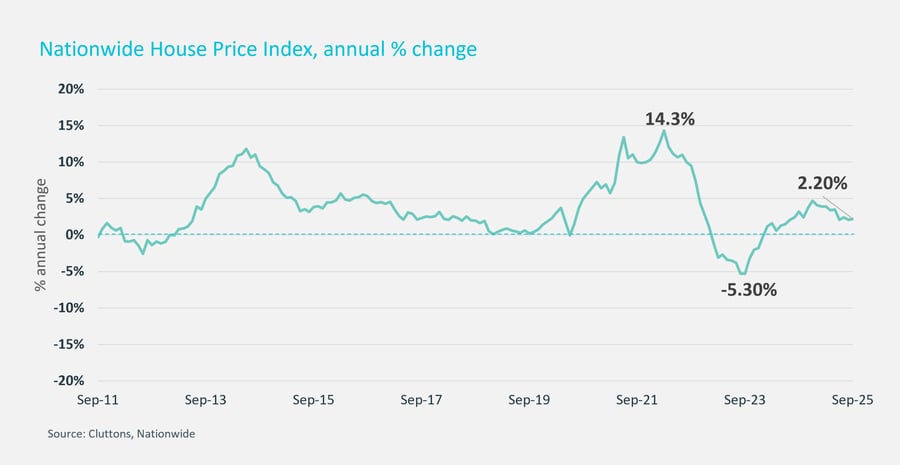

Average house prices across the UK rose by 2.2% in the year to the end of September. Headline price growth has been at this level since the summer, and we expect it to settle here through to the end of the year.

Any further rate cuts in December could provide a fillip to the market, but this would likely be reflected in the data next January and February.

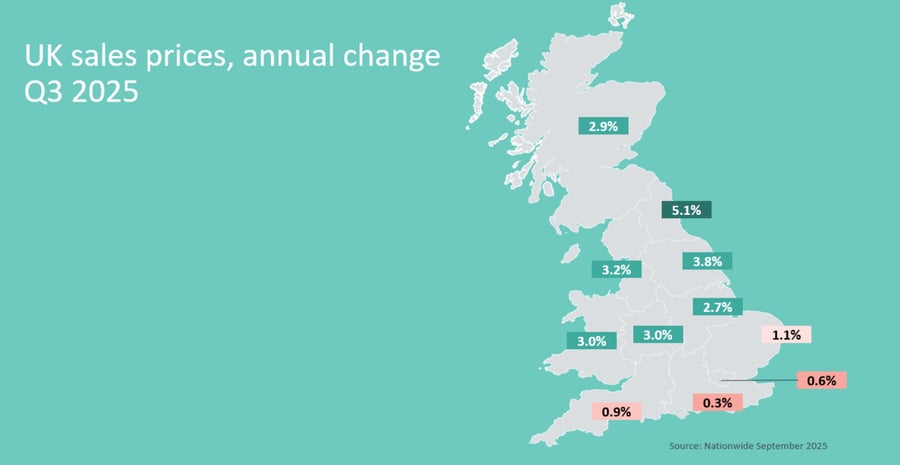

As ever, the rate of price growth varies across the country, with more affordable markets in the Midlands and the North of England showing stronger price growth. Average house prices in the North East are rising at an average of 5.1% a year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.