Prime London & UK rental market update Q4 2025

The policy landscape for the rental market is on the cusp of significant change. The Renters’ Rights Bill received Royal Assent in October and will come into effect in May next year.

In addition, there is speculation that the Budget could also impact the rental market, with discussion around a possible rise in income tax which would include rental income for individuals. There is speculation that National Insurance (NI) could be cut to help offset some of the income tax rises. At present landlords do not pay NI so would not benefit from this, but this crosses over with another proposal that has reportedly been circulation for inclusion in the Budget – namely introducing NI on rental income for landlords who pay income tax. Either move will impact landlords and could prompt an additional number to consider their next move. If some choose to exit the market, this would put more strain on limited supply, which will put upward pressure on rents.

Key facts:

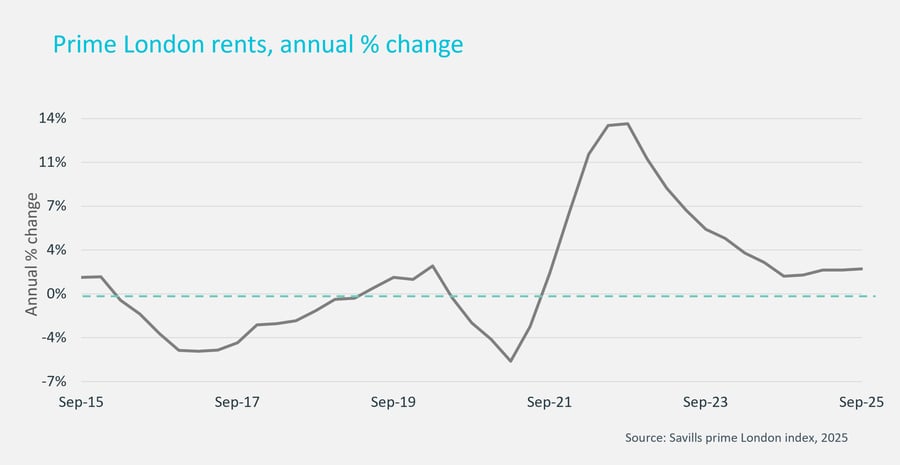

- Prime London rents are up 2% on the year in Q3, up from 1.4% in the year to Q3 2024

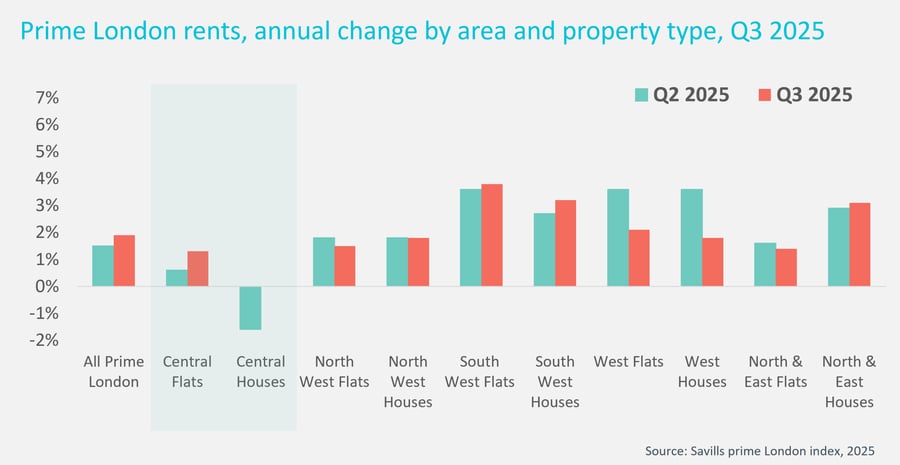

- Average rents for flats in prime central London are up 1.3% on the year, while the rent for houses is showing no change

- Average prime central London gross yields are at 3.5%, up from 3.3% in Q3 2024 as rents have risen faster than capital values

Demand in the prime central London market remained steady in Q3, with the lower rate of rental growth for houses reflecting the slower demand for family homes during the summer months. Across the wider prime London market, the supply/demand gap is more pronounced, resulting in stronger rental growth in many markets. Average prime rental growth has remained steady at between 1.4% and 2% for a year. This marks a large change from the height of the market just after the pandemic when rental growth rates hit double digits, but the steady performance since September last year signals that the market has found a new balance.

Some landlords will have already taken action in light of the new Renters’ Rights Act, but many more will find the start of the new rules will be trigger to consider their next steps. In addition, any measures which effectively levy more tax on landlords at the Budget on November 26th could also lead to additional landlords reviewing their options. Our agents report that the number of landlords asking for both a rental and sales valuation has risen over the last 12 months.

As such, we could see more rental properties being sold, and while some may be purchased by investors, they may move into the sales market. Any further reduction in the supply of rental properties could underpin rental growth, although the wider conditions in the market will likely keep the level of growth in the low single digits in the coming years. We are forecasting +3% growth this year, and +3% next year.

UK rental market

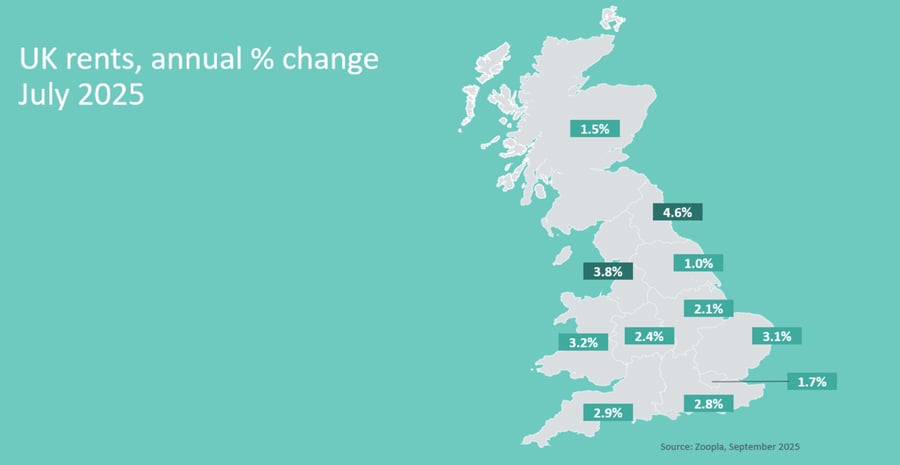

Average asking rents in the UK were up 2.4% on the year in the late summer, according to the latest research from Zoopla. On the wider index of rental data from the ONS, which also includes renewals, average rents are up 5.5% on the year to September. Both indices are showing a significant slowing in rental growth from the peak in the market. The ONS measure, which is slightly lagging the Zoopla data, shows that average rental inflation has fallen from 9% in December 2024.

The easing in rental growth comes as the large imbalance between supply and demand has partly unwound, especially in city markets where supply was particularly constrained after the pandemic. However, there rental supply is still tight in some areas, especially at specific price points. This is only being exacerbated by some landlords reviewing their portfolios in light of new rules coming into force as part of the Renters’ Rights Act. If the Budget also leads to more tax changes for landlords, this will also have an impact.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.