Economic update

Q4 2025

Slower economic growth and a growing productivity gap means the Chancellor will most likely raise taxes in the November Budget.

Key facts:

- There is increasing speculation this could include taxes on property, with proposals reported to include an annual tax on higher-value £2m+ properties, or additional council tax on the highest banded homes. You can see a more in-depth round-up of all Budget speculation in our blog

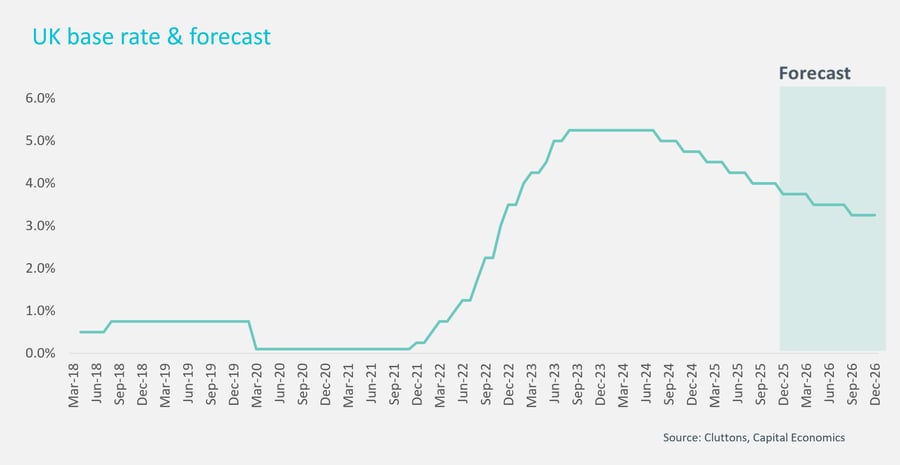

- The base rate remained unchanged in November at 4%, but the chances of a pre-Christmas rate cut in December are rising

- Average UK house prices were up 2.2% in the year to September, around half the rate of growth compared to January this year. Prime London prices are down -1.8% on the year while prime central London prices have fallen -4.6% on the year

Economic growth

The slow rate of economic growth in the UK continues, with GDP rising by 0.3% in the three months to August 2025, compared to 0.2% in three months to May. While this may mean that the UK is outperforming many of the other G7 nations, it still indicates a muted rate of growth at 1.3% year on year. This is a challenge for policymakers as it means less revenue coming in for the Treasury amid lower pay rises and employment levels, just as borrowing costs for the Government have risen. The Chancellor will have to address this in her November 26th Budget, and has strongly indicated that tax rises are on the way. It seems likely that income tax rises might be in the frame, as well as some taxes on property. Most recently a so-called ‘mansion tax’ has been mooted’ – a 1% charge on the value of homes worth more than £2m. For a £3m home this would mean a charge of £10,000 a year. For a £3m home this would mean a charge of £10,000 a year. There is more on this in the prime London market sales update, and in our Pre-Budget blog.

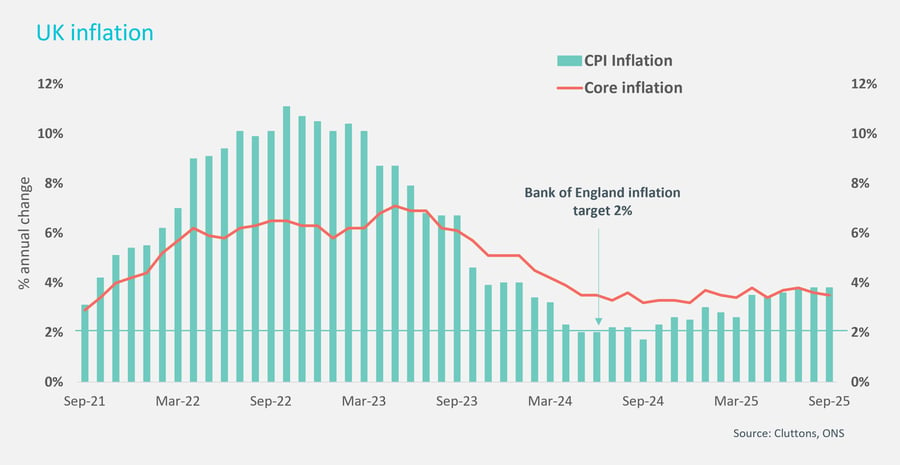

Inflation

The cost of goods and services rose by 3.8% in the year to the end of September, the same rate of CPI as in August, but core inflation, which excludes items with more volatile pricing such as food and energy, fell to 3.5% from 3.6% in August. The echoes of record-high double-digit inflation just two years ago are still loud, as this 3.8% CPI reading was seen as relatively good news as economists and the markets expected an even higher rate of inflation.

Base rate

The Bank of England’s Monetary Policy Committee (MPC) looked at the forecasts for inflation in their November meeting, which is tipped to continue to ease back, especially considering lower economic growth. However, they did not think that the disinflationary factors were strong enough yet to warrant a quarter point rate cut, although it was a close call with 4 members voting for a rate cut and 5 members voting for no change.

However, the messaging from the rate-setting committee was clear, the trajectory for rates is definitely downwards, saying “If inflation stays on track, we expect to be able to gradually cut rates further.”

We expect base rates to end next year at 3.25%, although we may need to revisit this after the Budget.

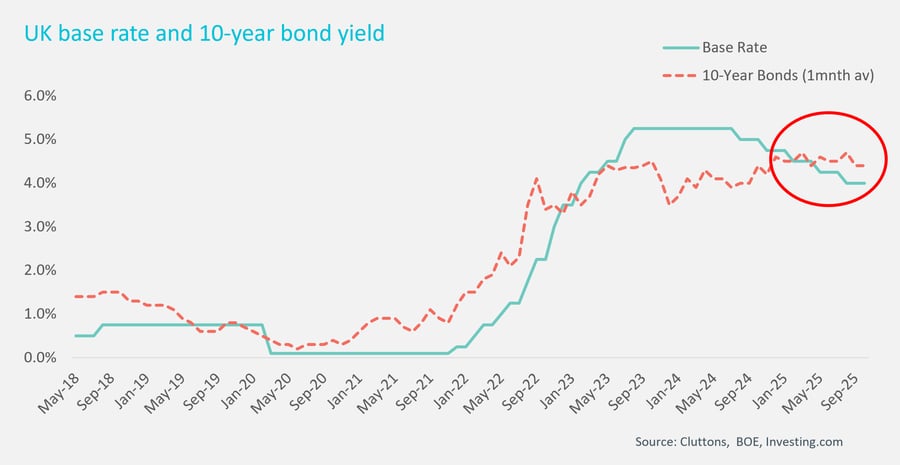

The strong narrative from the Chancellor around tax rises has played well with the markets, with gilts rates falling during October. However, the markets’ reaction to the Budget itself remains to be seen.

If the income tax rise that the Chancellor has talked about comes to pass, it will have an impact on household finances and potentially consumer confidence, and may have ripple effects that further act as a drag on economic growth, increasing the speed of rate cuts.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.