Prime London & UK rental market update Q1 2026

The introduction of the Renters’ Rights Act (RRA) is now just months away, marking the biggest regulatory change in the rental market for decades.

The new rules, coupled with tax and policy changes in recent years, and the future rise in income tax from investment property announced at the Budget, are prompting some landlords to review their portfolios. Smaller landlords, and especially accidental landlords, are the most likely to exit the market, the number of rental properties being put up for sale is rising. This is curtailing supply in the rental market and will continue to do so, amid steady demand. This supply/demand imbalance will put a floor under pricing and we expect rents to continue to climb, but recent double-digit rental growth means that affordability constraints will limit the scale of this rise.

Key facts:

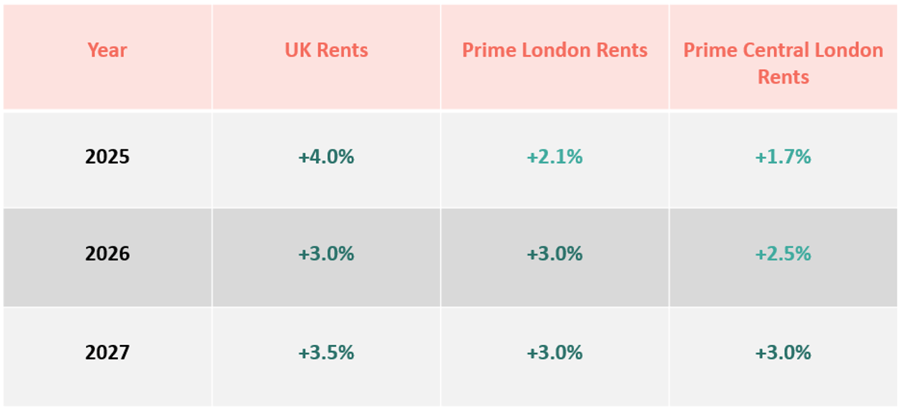

- Prime London rents rose by 2.1% in 2025, compared to 1.5% growth in 2024

- Average rents for flats in prime central London are up 2% on the year, while average rents for houses in this area are up by just 0.2%

- We expect 5.5% rise in rents in prime central London in the next two years, 6% in prime London and 6.5% across the UK.

Source: Cluttons

Some landlords will have already taken action in light of the new Renters’ Rights Act, and others may be considering their next move considering the Budget announcement of an additional 2% on income tax from property income.

EPCS

The proportion of vendors across our prime London offices asking for a joint sales and rental valuation has risen from 25% to 65% over the last year, and the number of landlords opting for a sale has been rising. While some of these homes may be purchased by investors, they could also be snapped up by first-time buyers or homemovers which means the property would no longer be in the private rented sector (PRS).

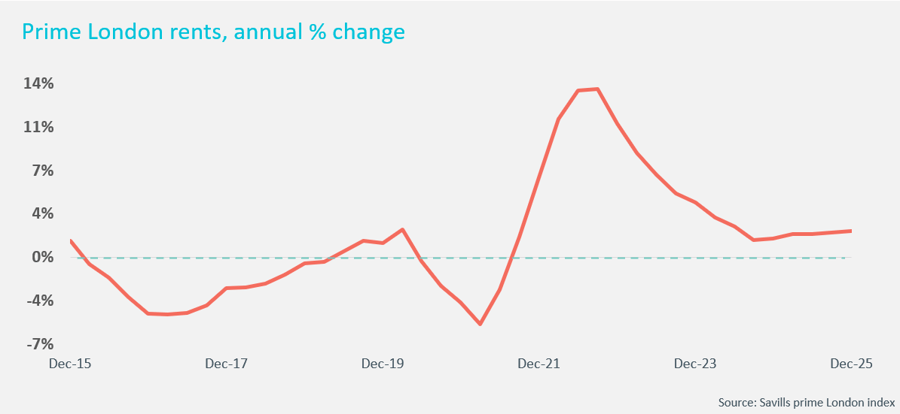

Demand in the prime London market remained steady in Q4, and rental growth has been stable for more than a year now, at between 1.5% and 2% on an annual basis, signalling the market has found a balance after the very strong rental growth after Covid. This pushed up rents close to affordability ceilings for some properties, and in some markets affordability constraints will continue to limit the scope for rental growth. Rents rose by 2.1% in the prime London market in 2025. Rents in prime central London were up by an average of 1.7%, but the rise in rents for flats is outpacing houses as more renters choose lateral space and potentially lower total rents for smaller apartments. Average rents for flats in PCL rose by 2% on the year, while rents for houses remained broadly flat at 0.2%.

We forecast the rate of rental growth will tick up slightly this year to 2.5% in prime central London and 3% in prime London as a whole. However, the introduction of the Renters’ Right Act does introduce a greater level of uncertainty around these forecasts, especially if more landlords decide to sell in the lead-up to May, which could put upward pressure on rents.

UK rental market

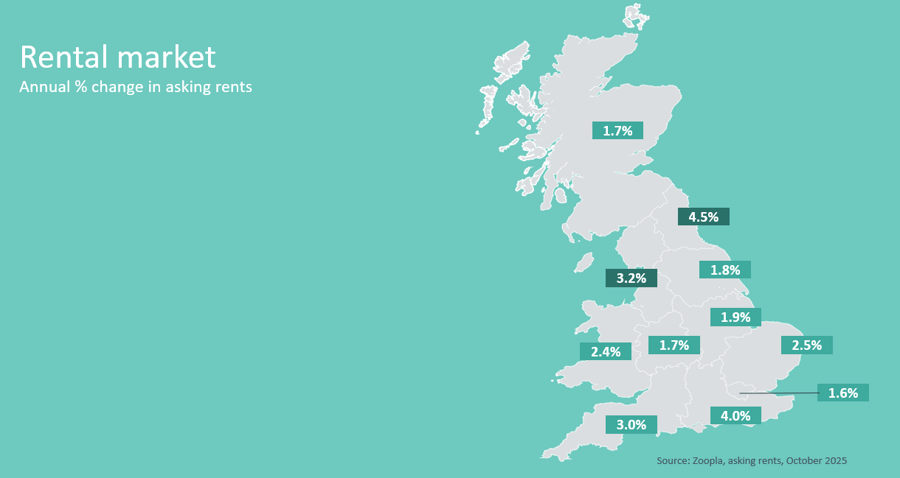

Average asking rents in the UK were up 2.2% in the year to October, according to the latest data from Zoopla. On the wider index of rental data from the ONS, which also includes renewals, average rents rose by 4% in 2025. Both indices are showing a significant slowing in rental growth from post-Covid peaks in rental growth where very strong demand coincided with limited supply. The ONS measure, which is slightly lagging the Zoopla data, shows that average rental inflation has fallen from 9% in December 2024.

The large imbalance between the supply of rental properties and demand from renters has only partly unwound, and this dynamic will continue to underpin growth in the coming years.

On the supply side, the RRA and the upcoming rise in income tax for income from property coming into force next year will likely continue the trend of some individual landlords choosing to leave the market. In addition, before 2030 landlords who have a property rated lower than an EPC C will have to invest to raise the EPC rating to this level. For properties that need too much work, the Government is still proposing that landlords invest, although they have capped the spend at £10,000. There is an expanding number of Build-to-Rent developments being delivered across the country which will boost supply in the rental market, but the numbers are still modest compared to the size of the PRS, which currently numbers around 5 million households, and is unlikely to make up the supply shortfall in the short to medium term.

There is still steady demand for rental properties, although this may ease slightly as lower mortgage rates and looser mortgage lending criteria make it easier for first-time buyers to climb onto the property ladder.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.