Economic update summer 2024

The first base rate cut in more than four years coupled with a sense of political stability from a new Government with a large majority should underpin improving economic growth through the rest of the year and will encourage more activity in the property market.

Key facts

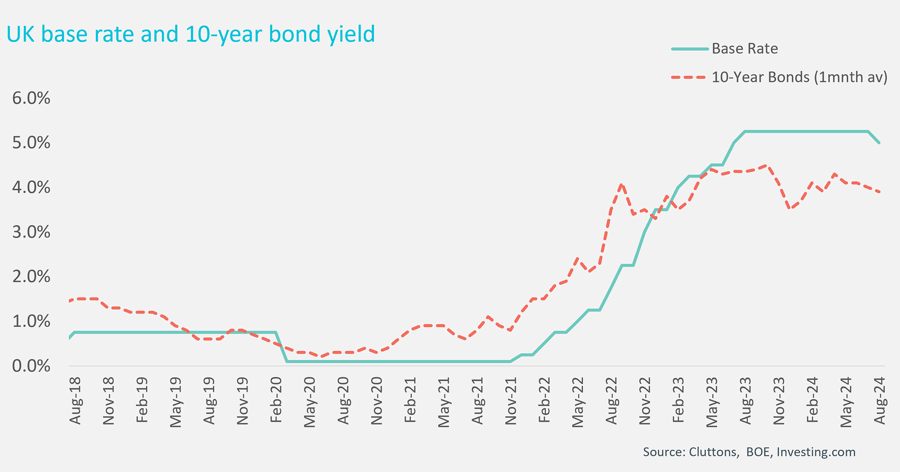

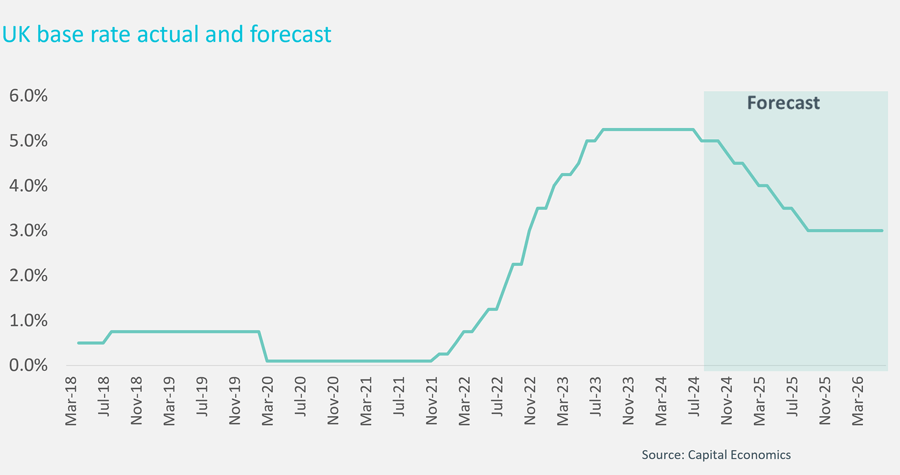

- The base rate has been cut for the first time since March 2020, from 5.25% to 5%, with expectations of another cut this year and more cuts next year

- The UK economy is performing better than expected, with upward revisions to growth for this year

- Optimism could be tempered slightly by tax rises coming in October Budget, which could include changes to capital gains tax (CGT)

The UK economy grew by 0.7% between January and March this year – which was more than expected. As a result, expectations for economic growth this year have been revised up by many economists, with EY forecasting 1.1% growth. The IMF thinks the growth will be more modest at 0.7% for the year, but even so – this means that the UK would not be lagging in terms of economic growth compared to the rest of the G7 nations.

The stability provided by the new government, which has come to power with a large majority, will likely underpin confidence in the economy. The Chancellor has been at pains to highlight that no spending plans will be announced without a full explanation of how they will be paid for, something that also reassures international markets.

However, at the same time, the Chancellor’s initial announcements also signal that there may be significant tax changes coming at the first Budget on October 30th, which could temper the rising consumer confidence currently in the market.

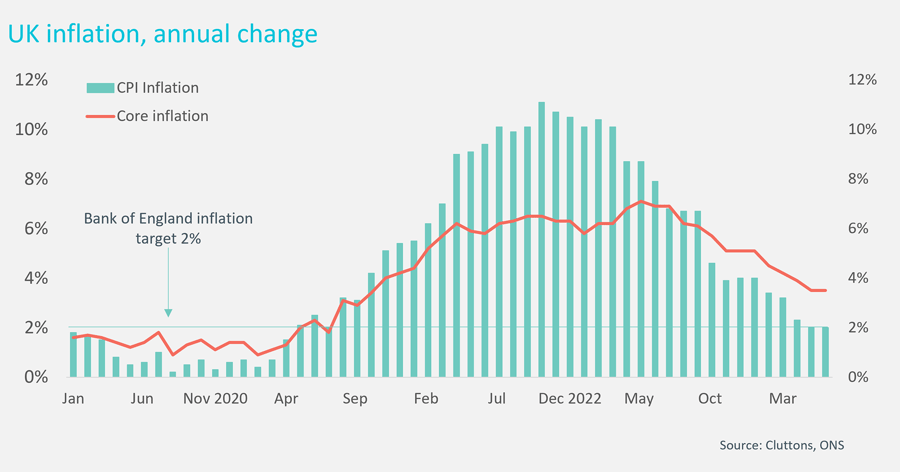

In the run up to the July election, the Conservative Party were keen to highlight falls to inflation this year to burnish their economic credentials. Inflation has indeed fallen to the Bank of England’s target of 2% from 4% at the beginning of the year and 6.7% a year ago, and it looks to be steady.

However, it is the new Labour Government who has benefitted from this decline, with the Bank of England delivering its first rate cut in four years within weeks of them coming to power.

The central bank’s monetary policy committee (MPC) voted 5-4 to cut the rate (with 4 voting to hold), signalling that although there were wide expectations of a rate cut this month or next, the timing was not a done deal. One more rate cut is currently priced in this year, with more next year. Capital Economics forecasts that rates will fall to 3% by late next year.

There are still factors which could speed up or slow down the trajectory of rate cuts over the next 12 months. If inflation continues to fall, it will open the way for more rate cuts sooner. However, it is more likely that inflation will tick up again marginally – the MPC expects it to rise a little to 2.75% by the end of the year as the declines in energy bills fall out of the calculations. But the MPC expects that an easing in pay rises in line with a looser labour market should offset this upward pressure on prices. It also said that the public sector pay deals suggested by the new Government should not put material upward pressure on inflation.

At the same time however, the central bank was at pains to point out that it would “be careful not to cut rates too much or too quicky”.

Overall, the economic picture in the UK is much brighter than it was at the beginning of the year, something that should continue to inject added activity in the residential markets.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.