UK & London lettings market update Q2 2023

Rents continue to rise, but the pace of growth is beginning to ease in many regions. Tight levels of supply are still underpinning rental growth.

Rents will continue to rise this year, but at a slower rate than in 2022.

Our quarterly update examines the latest trends in the UK, London and prime London lettings markets.

Key highlights:

- UK, London and prime London rents have risen strongly over the last 12 months as demand far outstripped the supply of homes to rent

- Rents will continue to rise in 2023 but at a slower pace

- Constraints on the supply of rental property are unlikely to unwind quickly

UK & London overview

The average rent for new lets was 11.1% higher in February than the year before as a surge in rental demand continues to clash with a tightening of supply, according to data from Zoopla. This rate of growth was slightly down from a peak of 12.1% late last year, but still marks a rapid acceleration in rents.

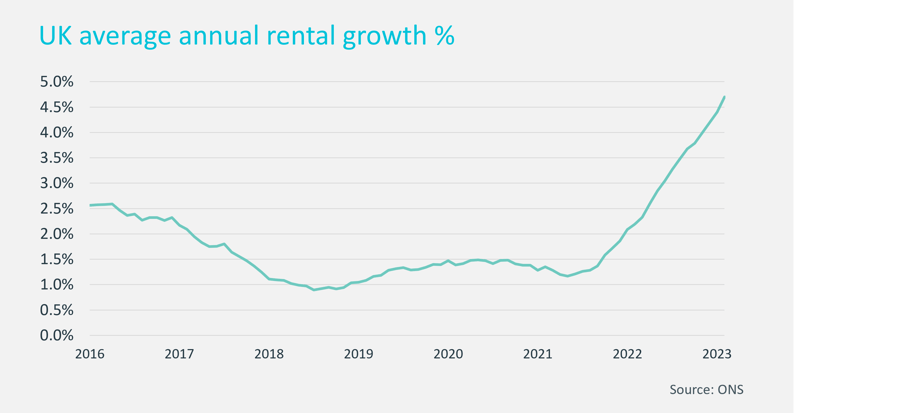

The ONS measure of rental growth, which includes rental growth for tenants who stay put in their existing residence, also rose to 4.7% in February.

Rents will continue to rise this year across the UK. Demand for rental properties remains strong, as returning students and office workers swelled the ranks of demand last year as the pandemic restrictions finally ended. In addition, recent mortgage rate rises mean that those saving for their first home are likely to stay in the rented sector a little longer as they continue to save, increasing demand again.

The supply of rental properties is coming under pressure for several reasons. A series of tax changes for landlords in recent years mean returns are eroded for some. Many landlords will also have to make changes to their properties to meet new EPC requirements.

However, there is discussion around potential changes to proposed new legislation aimed at increasing energy efficiency. Whereas landlords were being told to ensure that all rental properties were rated EPC C by 2025 under the proposed legislation, this may now be moved out to 2028, at which stage all rental properties, new let or existing let, would have to be a C rating. If this is confirmed, it would mean that landlords have some time to choose whether to invest in their property to upgrade it to an acceptable rating. Those who decide not to do this may instead put the property up for sale.

Zoopla data suggests that around 11% of homes listed for sale on the portal have previously been advertised for rent. This does not mean that all properties will move into ownership – some larger landlords are also actively expanding their portfolios, but there is no question that the economics have changed, especially for smaller landlords.

Even so, we are seeing an easing in the level of growth in rents for new lets agreed as highlighted in our previous update. There are affordability limits for rental properties, even in a tightly supplied market, and there are signals that in some markets rents may be reaching a natural ceiling. We forecast that rental growth will continue this year, but the rise will be in the mid-single digits.

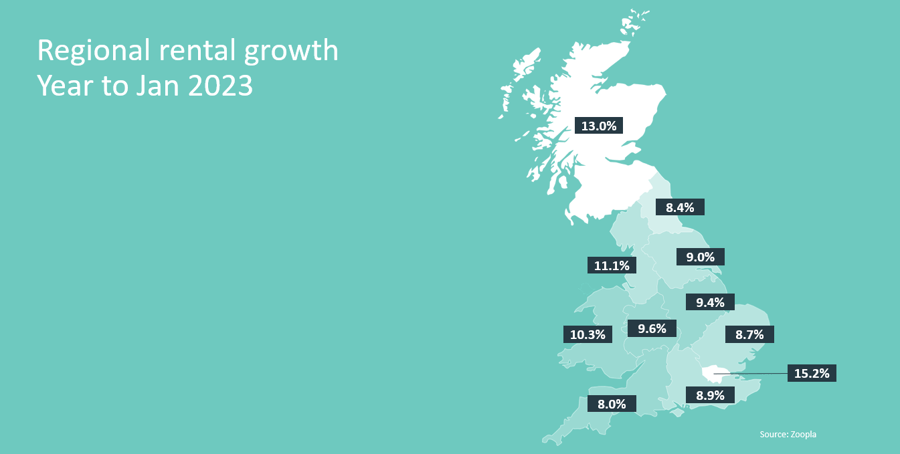

London rental growth is still leading from the front, as shown in the map below. Yet even in London, the pace of rental growth for new lets has fallen back slightly from a high of 17%, to 15.2%.

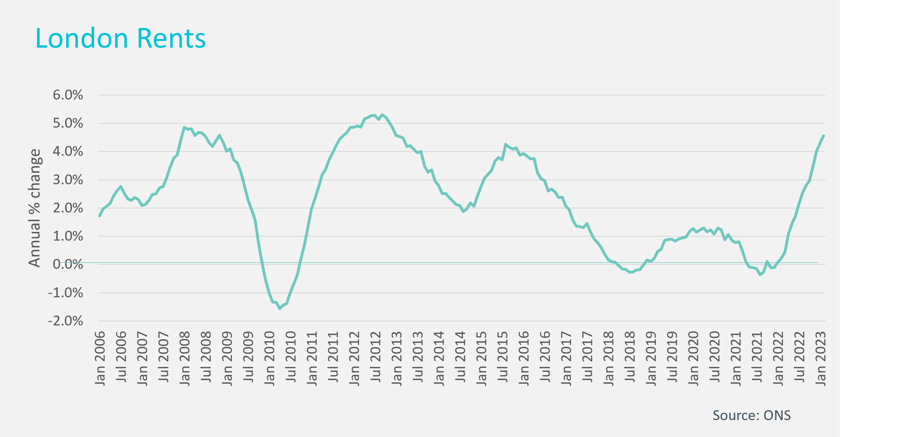

To put London’s rental growth in context, it is worth considering that rents dropped in the capital for the first year of the pandemic – with material rental falls – so the strong rental growth over the last year or two has to some extent marked a bounce-back from that downturn. This is also reflected in the ONS data below, which also illustrates the strong upwards pressure on rents in recent months.

Prime London

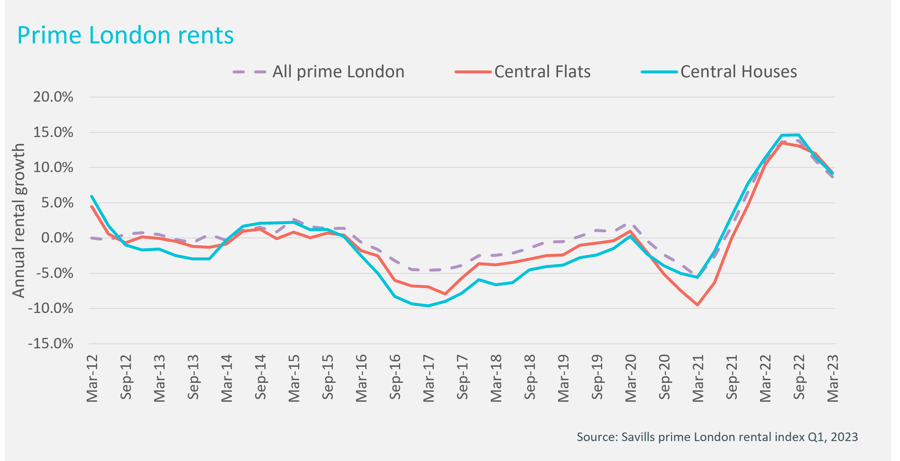

Agents report that demand continues to outstrip supply in the London market, and that most properties are achieving asking rents. Yet there has been a slight turn in the number of properties achieving a premium over asking rent, again highlighting that in some markets, a natural affordability ceiling may be inhibiting further strong upward pressure on rents.

While prime London rental growth is still strong, it is falling back from its peak last year.

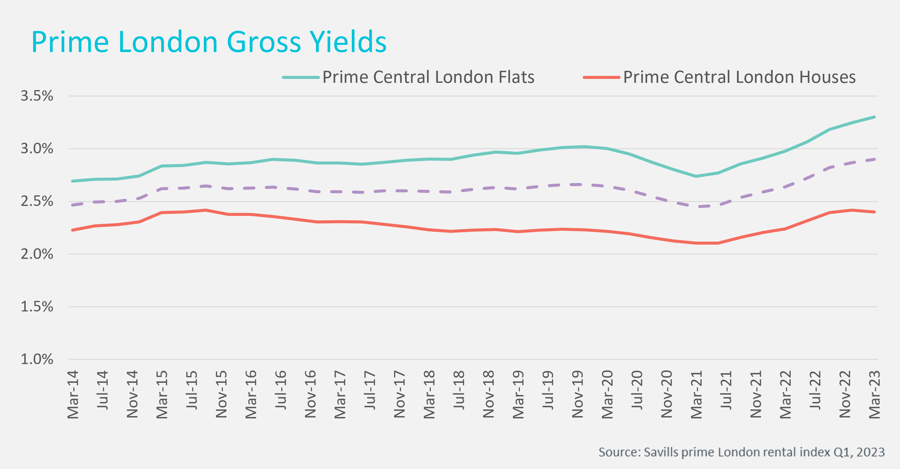

Strong rental growth, and a recent easing in capital values means that gross yields for prime central London property averaged 2.9% in Q1, the highest level in decade. As ever, property type and location will affect yields, with yields rising to 4% for a 1-bed property in central London.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.