UK & London sales market update summer 2024

Average values remain flat across prime London, but well-priced properties gaining more attention

Highlights

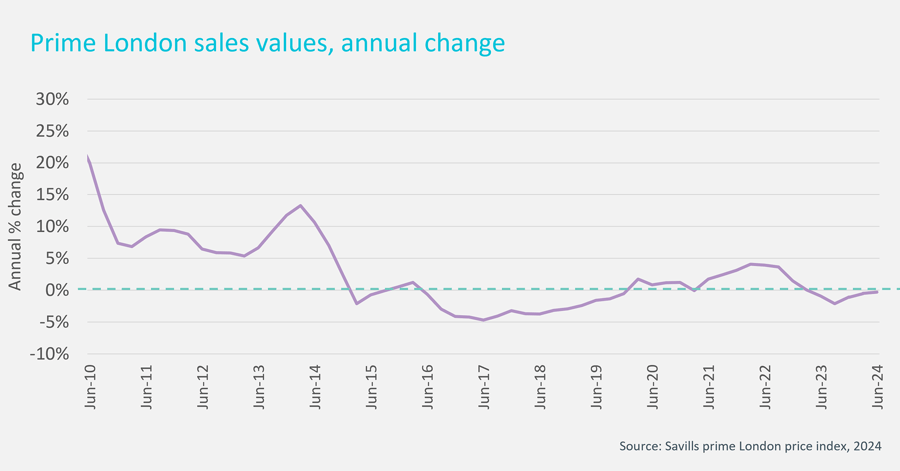

- Prime London prices unchanged year-on-year in Q2

- Average house prices in the rest of the UK edge up in July, at an annual rate of 2.5%

- Transaction levels continue to build with more stock coming onto the market

Prime London sales market

A recalibration of expectations around base rate cuts at the start of the year (with markets pricing in three rate cuts rather than five) acted as a drag on the market in Q1. But momentum started to build in Q2 in line with the usual seasonal Spring trends, aided by anticipation of the first rate cut– and that cut was delivered in early August with the Bank of England cutting rates from 5.25% to 5%. While this cut has already been priced into mortgages – with money market rates pricing in the move over the last few weeks – and even though there is only likely to be one more rate cut this year, the very fact that the central bank is starting to move rates downwards will be enough to engender confidence in all corners of the economy, including residential markets.

This increased momentum will help to boost sales numbers, and may put some upward pressure on prices, but vendors should consider that mortgages are still relatively more expensive than during the period of ultra-low mortgages, and that there are some other factors affecting London’s prime property market, not least higher average stamp duty than the rest of the UK due to higher capital values.

The new Government have pledged to increase stamp duty by 1% for non-UK buyers – it is likely that this change will come into force at or shortly after the Budget on 30 October. The stamp duty payable on a £2.5 million home by a non-UK buyer where it is a second home will rise to 15%, up from 14%.

In addition, residents who are classified as non-doms will see their tax arrangements change under new plans to be brought forward by the Government, which will bring world-wide assets into the UK tax regime within four years, rather than being allowed to shelter some overseas assets from UK tax under the non-dom arrangements. This is likely to affect the prime central London (PCL) market more than the wider prime London areas. Likewise, the introduction of VAT on private school fees from January next year which has been confirmed by the Chancellor, may affect the budgets of some purchasers from next year in the PCL market.

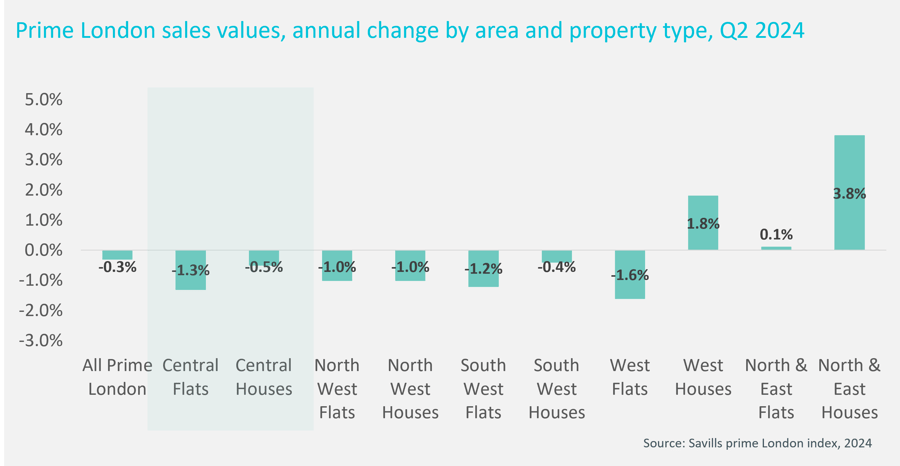

In fact, average values in the prime central London market are slightly lagging the average, with flats down by 1.3% on the year, as the chart below shows. In contrast, properties in the north and east prime markets, including Wapping and Islington, registered price growth in Q2, with average houses (which tend to be in shorter supply) values climbing by nearly 4% on the year.

UK sales market

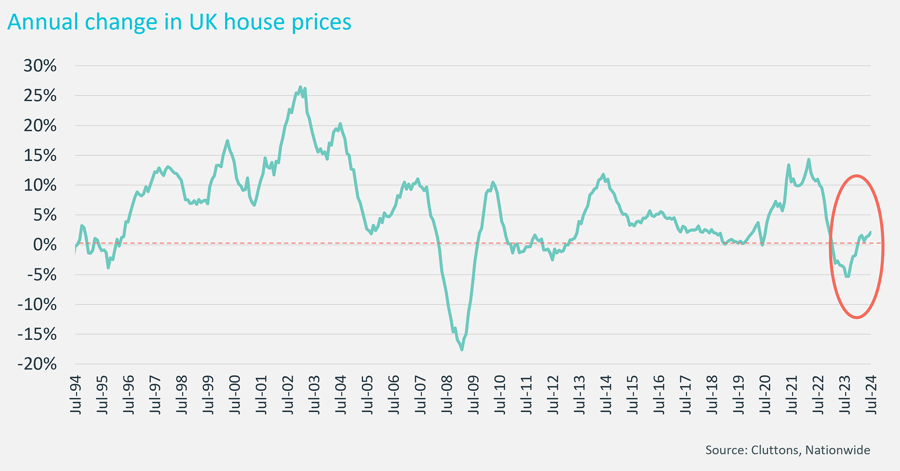

Average UK house prices rose by 0.3% during July, taking the annual growth to 2.1% equalling the rate of growth seen at the end of 2022 just before prices started falling.

Mortgage rates started to fall back in June and July in anticipation of a rate cut, and this may have underpinned this slight acceleration in growth. However, affordability remains a concern, as even with the rate cut in August, mortgage rates are still significantly higher than during the era of ultra-low rates, meaning budgets will be more constrained for buyers. This means the rate of growth may well remain muted through this year even if there is another rate cut.

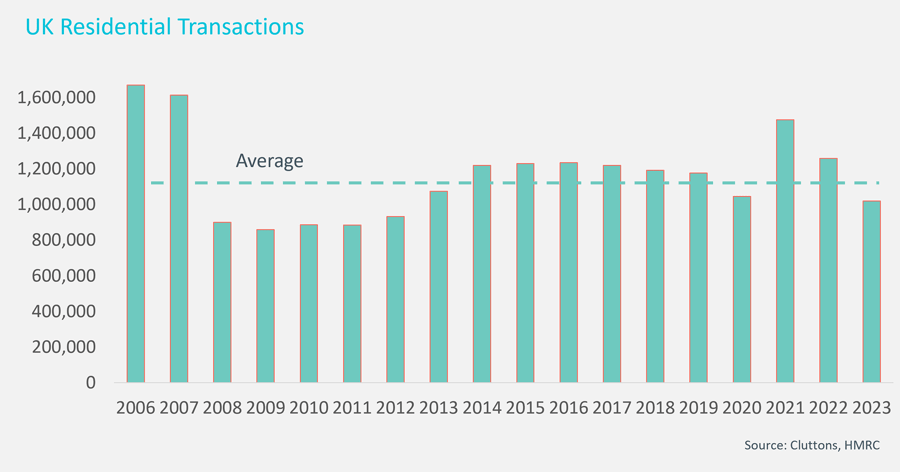

Activity in the residential sales market picked up in June, with 91,370 completions, some 8% higher than June last year. In the year from April 2024 there have been 272,700 sales, up from 245,120 during the same period last year, and getting closer to the average levels seen in the pre-pandemic years. Activity will continue to pick up this year amid rate falls, unless any surprises in October’s budget cause uncertainty.

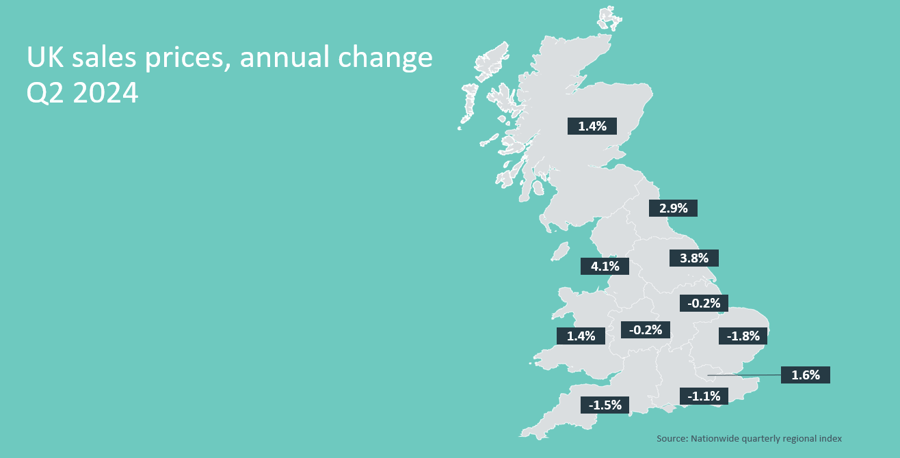

As ever, not all parts of the country are moving at the same speed when it comes to price changes. While the North West and Yorkshire & Humber are recording annual price growth of 3.8% or more, average values are still falling on an annual basis in much of Southern England. The exception is Greater London, where prices are up 1.6%. London experienced a more muted rise in prices during the pandemic, and a smaller reversal last year, giving it a platform for a stronger price recovery in current market conditions.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.