Economic update and residential forecasts – January 2025

A volatile start to the year in the bond markets highlighted the more uncertain global geopolitical landscape and concerns about the UK’s fiscal position, although gilt yields have fallen back after better-than-expected inflation figures.

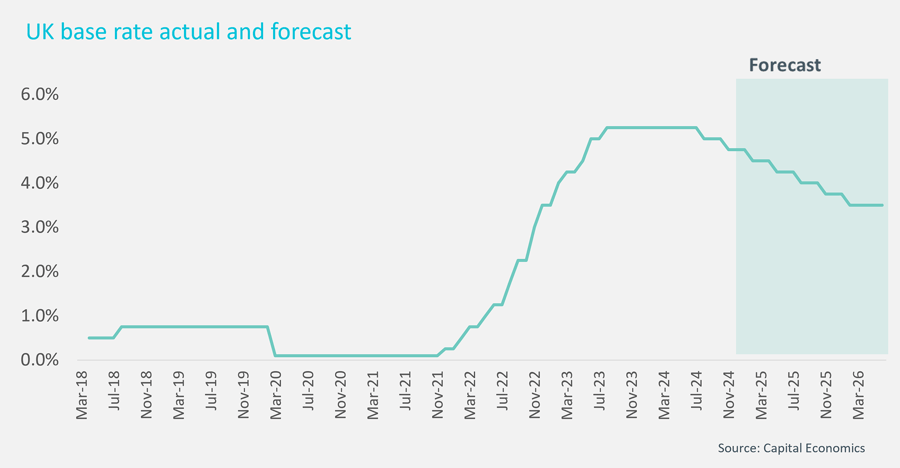

We expect the base rate to be cut three or four times this year as inflation falls back over the next 12 months and this will underpin activity in the residential sales market.

Key facts

- Activity will rise in the UK sales market, underpinning 4% growth this year

- Modest growth in prime sales values this year before gaining momentum in 2026

- Prime rental growth to pick up this year to 3%

After growing in the first half of last year, the UK’s economy slowed in H2, showing only 0.1% growth in November after declining in September and October. There is still a chance output contracted in the final quarter of the year. Overall, GDP growth for 2024 is set to be less than 1%. Many economists and the Office for Budget Responsibility (OBR) forecast that GDP will rise this year – the OBR says to 2% growth – as the spending announced by the Chancellor in her Budget starts to take effect. However, there are also real concerns about the impact of the rise to employers’ National Insurance (NICS) payments which comes into force in April, something which could inhibit employment growth and affect productivity.

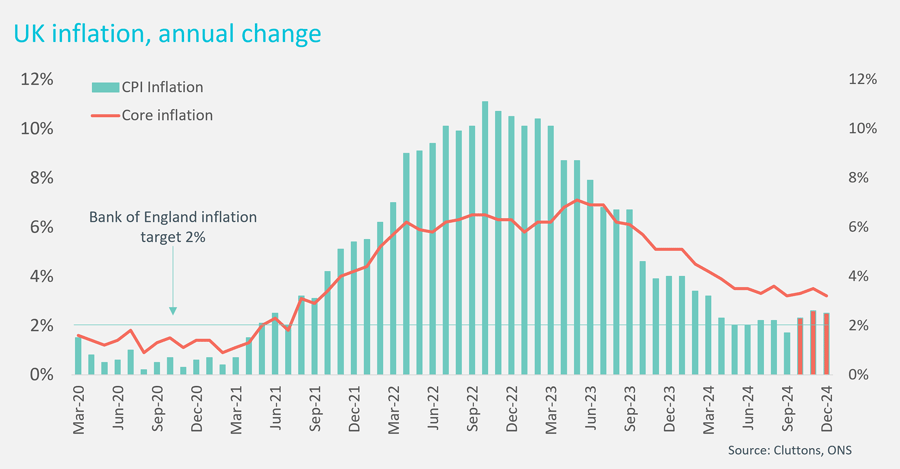

A slightly weaker outlook for economic growth increases the chances for more rate cuts this year. The markets are currently factoring in two base rate cuts this year, amid fears over ‘sticky’ inflation – inflation staying higher than target for a sustained period. But inflation fell unexpectedly in December, from 2.6% to 2.5%, and is expected to fall into the summer and during the rest of the year, which could result in more rate cuts. Capital Economics is forecasting that rates will be 3.75% by the end of the year, settling at 3.5% in 2026.

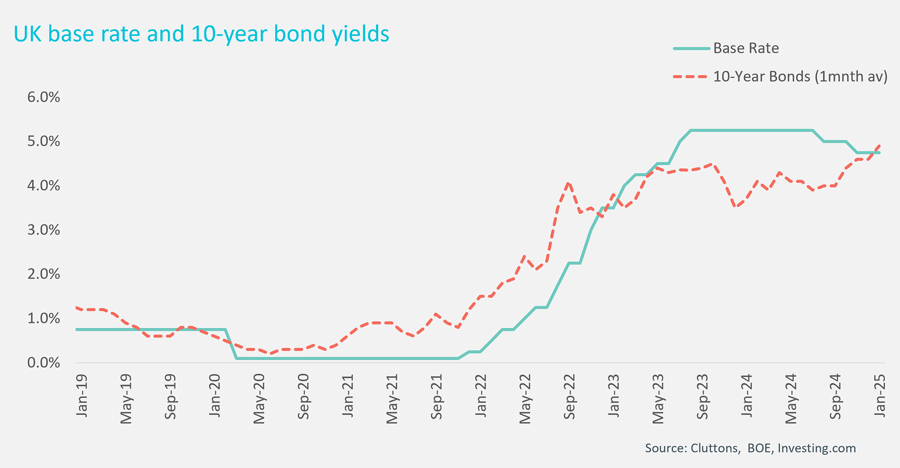

The inflation data also calmed fears that emerged in the bond markets in the first two weeks of the year. Bond markets around the world felt the impact of a more uncertain geopolitical landscape and fears over inflation in the US – bond yields rose rapidly in the US, Japan and many European countries and in the UK. Also underpinning the rise in UK bond (or gilt) yields was concern around the Chancellor’s fiscal position. As shown in the chart below, the 10-year gilt rate rose to 4.96% in early January, the highest level since 2008. Gilt yields are linked to the swap market, the money market rates which determine mortgage rates, raising the chance that even as the base rate stayed unchanged, mortgages could become more expensive.

Gilt yields fell back sharply on 16 January after that lower inflation rate emerged and weaker than expected GDP growth figures were published. Gilt rates are now returning to levels like those at the beginning of the year.

The economic outlook is a little more uncertain in 2025, but more rate cuts translating into lower mortgage rates will stimulate the UK housing market. This was evident towards the end of last year, when demand, supply and overall activity all rose, pushing up prices. UK average prices ended the year up 3.6% according to Nationwide’s quarterly index, while their monthly index put the figure higher at 4.7%.

Some of this activity was due to buyers rushing to complete their purchase before changes to stamp duty coming into force at the start of April. From then, the starting threshold for paying stamp duty on a house purchase for home movers will fall back to £125,000, after having been raised to £250,000 by Liz Truss in 2022. The rate applied on sums between £125,000 and £250,000 will be 2%. For first-time buyers, the threshold for paying stamp duty will fall back to £300,000 from £425,000, and this discount will apply to properties worth up to £500,000, while at present the threshold is £625,000.

This busy period in the market may be because activity is being ‘brought forward’, and as such there may be a slight slowdown in activity immediately after the stamp duty change. But at that point, the traditionally busier Spring period will have started, and rate cuts will underpin a pick-up in activity. We expect 1.1 million transactions this year, and we still anticipate mainstream average house price growth of +4%, in line with our forecasts at the start of last year.

However, the Government is reported to be considering relaxing mortgage lending rules for first-time buyers, easing the limits on lending at higher loan to value levels placed on banks in the wake Global Financial Crisis in 2008/09. This would make it easier for those buyers with smaller deposits to access the market. Also, loan-to-income levels could be adjusted for banks. Currently, only 15% of a lender’s book of loans can be issued to those who are borrowing more than 4.5 times their income. The average price to earnings ratio for a home in England and Wales is currently 5.

If these new rules come into force this year, the risk to our forecast will be on the upside, and house price growth could exceed +4%.

Price growth in Greater London slightly underperformed the wider market with 2% growth this year, as rising mortgage rates stretched affordability and put a lid on capital values. The prime London market, incorporating prime central London and the prime outer areas stretching from Richmond to Canary Wharf, was also more muted in terms of price growth, although activity picked up during 2024. Additional stamp duty charges for those buying an additional property is another layer on the increases in the taxation regime for purchasers of prime London residential property over the last decade. The changes to the non-dom rules have also had an impact in some parts of the market. Even so, the lifestyle and amenity on offer means that London is still a key global destination for international buyers, and where more supply is coming to the market, buyers are seeing value. We expect prime London prices to rise by an average of 1% this year before gaining more momentum into 2026.

The prime London rental market was busy throughout 2024, but the rate of rental growth continued to slow from the unsustainable double-digit highs registered in late 2022. Rental growth settled at 1.5% in the second half of 2024, and we expect it to accelerate to 3% this year as supply remains constrained and outstripped by demand. Some of this demand is linked to buyers choosing to rent in a location before purchasing, or choosing to rent on more permanent basis to sidestep stamp duty.

Forecasts – January 2025

| Year | UK House Prices | Prime London Sales | Prime London Rents |

|---|---|---|---|

| 2024 | +4.7% | +0.6% | +1.5% |

| 2025 | +4.0% | +1.0% | +3.0% |

| 2026 | +3.0% | +3.0% | +3.0% |

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.