Industrial market update Autumn 2023

Net absorption of industrial space dipped into negative territory in Q2 2023 for the first time in 11 years as take up fell back to levels last seen before the pandemic.

Weakness in the economy and rising costs are prompting some to delay their plans to move or expand. Even so, vacancy rates are a relatively modest 3.8%. This is well up from sub-3% before the pandemic, but around the same level as 2017. High levels of pre-leasing mean that even as higher levels of new stock are delivered, the vacancy will only climb to just above 4% next year (rising to 4.5% for logistics). In Manchester, the vacancy rate has risen from record-lows, pushed higher by the logistics sector, but is still registering just 2.5%

Some 64.2 million square feet of industrial space is currently under construction in the UK, but it is likely that future speculative construction activity may slow down amid the more challenging economic conditions. Buildings completed to a high specification, and especially those new or redeveloped schemes that meet BREEAM Very Good or Excellent standard have attracted high demand and will command a rental premium.

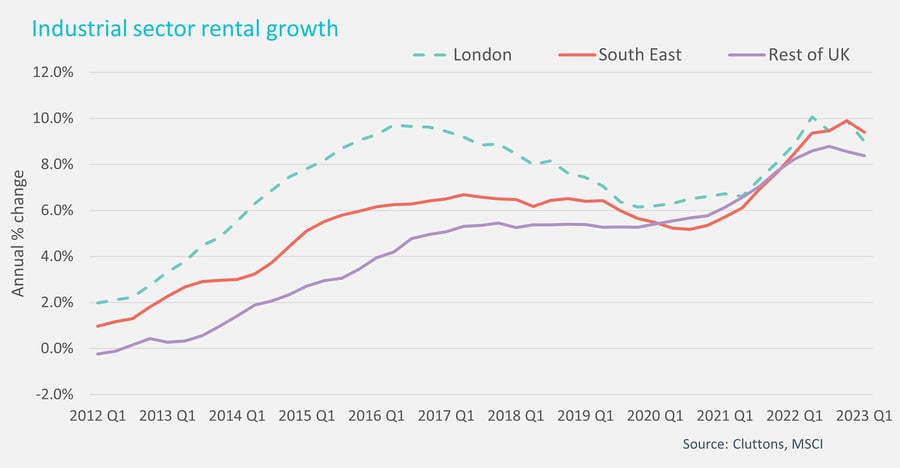

UK average rental growth for industrial is slowing, but is still registering growth of 7.1%, down from nearly 9% in Q3 2022. Rental growth in Manchester is at 8.1%, down from a high of more than 10% in the first quarter of the year.

Consistently lower demand levels in London amid a fall-back in demand from online retailers after the pandemic and affordability issues for some smaller occupiers amid surging rents means that vacancy rates in this market have been rising more sharply than elsewhere. The average rate now sits at 4.7%, the highest level in nine years. Average rents for industrial space across London have doubled in the last decade. The steam is now beginning to come out of rental growth in terms of these historical trends, with rental growth at 6.6%, this is still outpacing other sectors.

UK rental growth is expected to continue to ease through this year and next as higher energy costs, wage bills and business rates affect affordability for tenants. The relative balance between the demand and supply for industrial property will result in rental growth, but the rate of this growth will be slower than over the last two years.

Investment levels fall. Sales volumes over the last 12 months totalled £8 billion, down from £18.6 billion in the second half of 2022 as the cloudier outlook for the economy and the path of interest rates weighed on demand. The scale of investment during the pandemic is highlighted when noting that industrial property now accounts for 32% of assets in the MSCI index – making it the largest sector in the index.

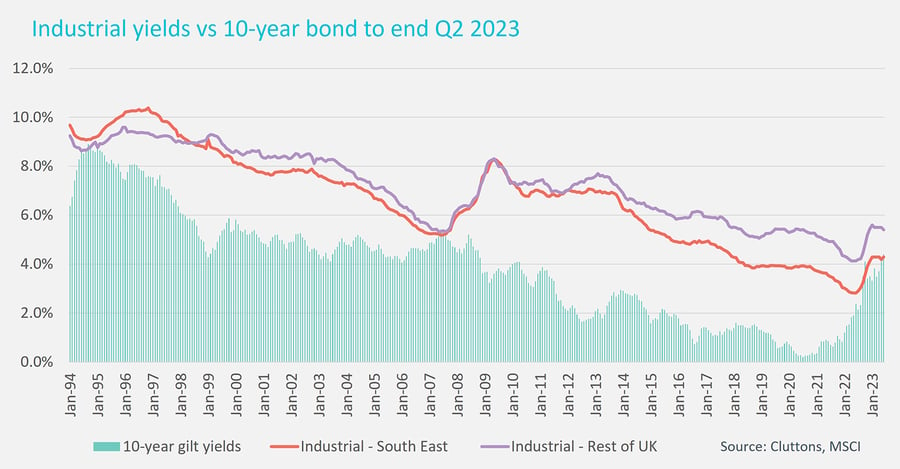

Recent rises in interest rates have increased the cost of debt, limiting the level of gearing on industrial, eroding the relative value of industrial property compared to other sectors, and pushing up yields. The upward path of yields was also driven by the market recalibrating after yields had hardened to unsustainable in mid-2022. After a sharp rise in the second half of last year, yields have now stabilised and are now around the same level as they were at the start of the pandemic – with average UK net initial yields at 4.6%, according to MSCI.

In London, yields have also softened, with sub-4% yields on deals now a rarity. Investment activity has also been muted in the first half of this year, reflecting the relative expense of London industrial property. There have been some notable deals however, as shown in the table below.

Sales volumes in Manchester were bolstered this year by a record £480 million combined sale of Trafford Park and Heywood Distribution Park to Blackstone.

| Property address | Town / City | Date | Building size (sqft) | Yield (%) | Sale Price (£m) | Buyer |

|---|---|---|---|---|---|---|

| 180 Hannah Close, Wembley | London | Q2 2023 | 180,720 | 3.5% | £74m | Church of Jesus Christ* |

| Auriol Dr, Tera 40, Greenford | London | Q3 2023 | 254,215 | – | £65m | Valor Real Estate Partners |

| Warth Park Way | Wellingborough | Q2 2023 | 660,000 | 4.0% | £85m | Aviva Investors Global Services |

| Trafford and Heywood Distribution Parks (bulk sale) | Manchester | Q2 2023 | 3.7m | – | £480m | Blackstone |

| Industrial Q1 2023 unless otherwise stated | UK | London & South East |

|---|---|---|

| **Distribution, multi-let estates and specialised industrial** | **Current quarter (last quarter / 5yr ave)** | **Current quarter (last quarter / 5yr ave)** |

| Occupier | ||

| Availability rate (%) | 5.2% (5.2%/5.5%) | 6.0% (6.0%/5.6%) |

| Vacancy rate % | 3.7% (3.6%/3.2%) | 4.2% (3.9%/3.2%) |

| Rental growth (12-month growth rate) | 7.6% (8.6%/6.6%) | 8.4% (9.3%/7.0%) |

| Quarterly take up (sqft) | 14.0m sqft (13.3m/22.6m) | 2.7m sqft (2.7m/5.0m) |

| Supply | ||

| Completions (net delivered sqft) | 7.5m sqft (11.5m/11m) | 906,422m sqft (1.2m/2.2m) |

| Total under construction (sqft) | 68.9m sqft (76.6m/55.8m) | 16.0m sqft (17.4m/10.8m) |

| Investment | ||

| Quarterly sales volume £m | £1,570m (£1,597m/£2,739m) | £608m (£594m/£1,013m) |

| Average yield | 4.6% (4.7%/4.3%) | 4.3% (4.2%/3.8%) * |

| Prime yield (rack rented) August 2023 (Q1 2023) | 5% – 5.25% (5% – 5.25%) Prime regional | 4.5%-4.75% (4.5% – 4.75%) Within M25 |

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Richard Moss

Partner, valuation & advisory – head of commercial UK funds

Head office

T +44 (0) 20 7647 7226