Retail market update Q2 2023

Retail sales fell back in May after rising slightly in April, according to a survey from the CBI, but the overall outlook is slightly more upbeat than at the beginning of the year.

Consumer confidence is improving from record lows late last year, and as we outlined in the Q1 report, there is a ‘lipstick effect’ in recessions, signalling that consumers move towards less expensive luxury goods amid economic downturns, turning to retail as a relief from economic turbulence. The GfK consumer confidence index continues to tick up, rising to -27 in May, up from -45 in January, after a low of -50 late last year. While the index of confidence is still in negative territory, it does suggest consumers are continuing to feel more optimistic as the year progresses, although higher than expected inflation may have an impact in the coming months.

UK footfall was up year on year in March, but this marked a fall-back from February levels, and retail parks are still lagging. The picture is brighter than during the pandemic, although footfall has not yet returned to pre-pandemic levels.

Whereas during the pandemic demand was largely driven by supermarkets and discount retailers, there has been more recent activity from fashion and food and beverage. This has been enough to stop negative net absorption in the market, although the positive figures remain very low.

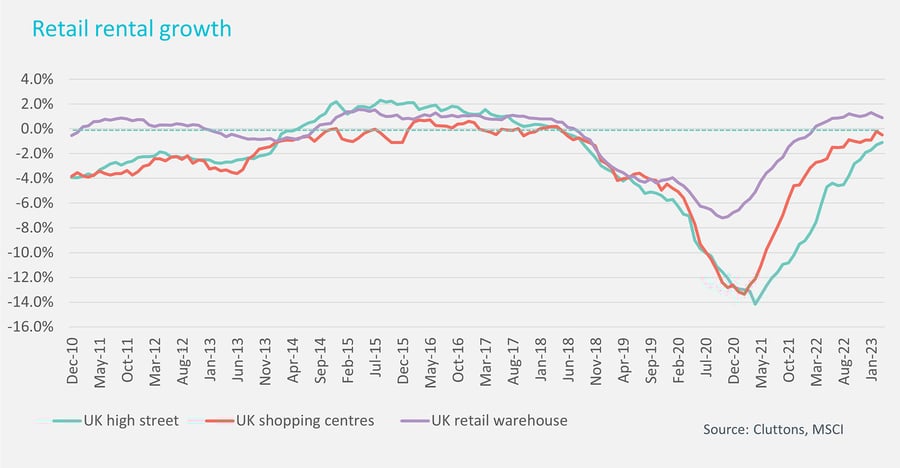

Increased demand coupled with very limited supply means the UK retail vacancy rate has dipped back to 3.1% from 3.2% at the start of last year. Increasing demand for retail for alternative uses will bring that rate down further in the coming years. This should continue to underpin rental growth, which has only reached positive territory this year, after nearly 4 consecutive years of declines.

Rents for retail warehouses have moved back into positive territory in the last 12 months, and this rental growth was 0.7% in April. Standard retail rents in the South East were down 1% on the year in April. The benefits for the retail sector as a result of business rates reliefs may mean rents are more sustainable in the medium term, especially among the larger retailers who will benefit the most.

Capital values are down around 15% in the year to April, a more modest decline than some other sectors – reflecting the fact that retail yields have been factoring higher risks for some years, which means the softening in yields in the wake of the mini-budget has had less of an impact on pricing than elsewhere in the commercial property market.

In London, the enduring appeal of prime retail property was underlined by two transactions in Bond Street and Old Bond Street, with 27 Old Bond Street, let to Alexander McQueen, achieving a sub-3% yield – emphasising its position as a safe-haven asset.

| **Retail: Data to end Q4 2022 unless otherwise stated | **General retail |

| ** | **Current quarter (last quarter / 5yr ave) |

| Occupier | |

| Qly take up (sq ft) | 2.6m sq ft (2.5m sq ft / 3.8m sq ft) |

| Rental growth (12-month rate) %* | 0.2% (0.2% / -3.7%) |

| Supply | |

| Completions (gross delivered sq ft) | 881,000 (918,000 / 1.6m) |

| Total under construction (sq ft) | 5.8m sq ft (5.3m sq ft / 7.6m sq ft) |

| Investment | |

| Qly sales volume (£) | £1.7bn (£692m / £1,603m) |

| Average initial yield %* | 6.6% (6.5% / 5.9%) |

| Prime Town High Street yield % May 2023 (Q4 2022) | 6.5%-6.75% (6.75%) |

Retail: key investment transactions

| **Address | **Location | **Date | **Building size sq ft (sub-sector) | **Sale Price (£m) | **Net Initial Yield | **Buyer |

| 63 New Bond Street W1 (Fenwicks) | London | Q1 2023 | 129,785 | £319.5m | – | Lazari Investments |

| 27 Old Bond Street W1 (Alexander McQueen) | London | Q1 2023 | 21,931 | £140m | 2.6% | Private North American investor |

| 40-44 George | Luton | Q1 2023 | 900,000 | £58m | 9.5% | Frasers Group |

| 168-192 High Street | Berkhamsted | Q1 2023 | 43,300 | £10.1m | 6.4% | Somborne Estate Ltd |

| Aldi | Weymouth | Q1 2023 | 18,500 | £6.9m | 4.9% | Private Investor |

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Richard Moss

Partner, valuation & advisory – head of commercial UK funds

Head office

T +44 (0) 20 7647 7226