UK & London rental market update – January 2025

The large imbalance between demand and supply partly unwound in 2024, although demand remains strong, and a lack of supply in the market is still driving rental growth.

New policies likely to come into force this year could lead to a further contraction in supply.

Highlights

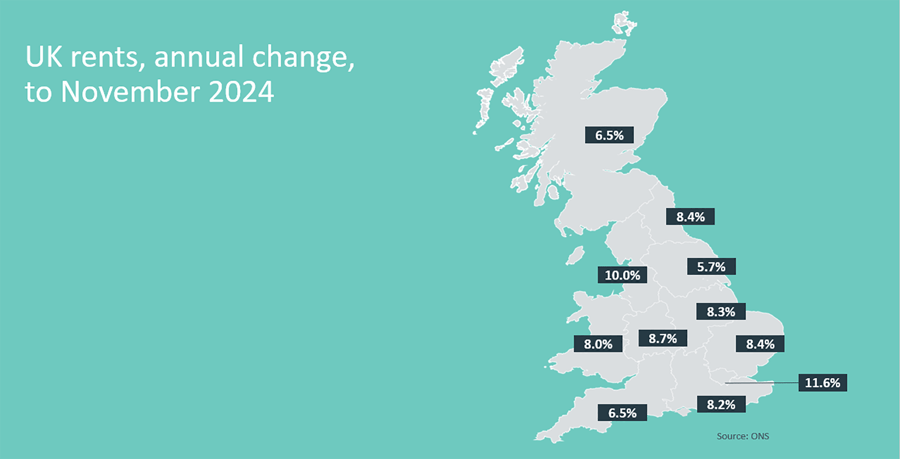

- Average UK rental growth at 9% in December, down from 9.1% in November, according to the ONS

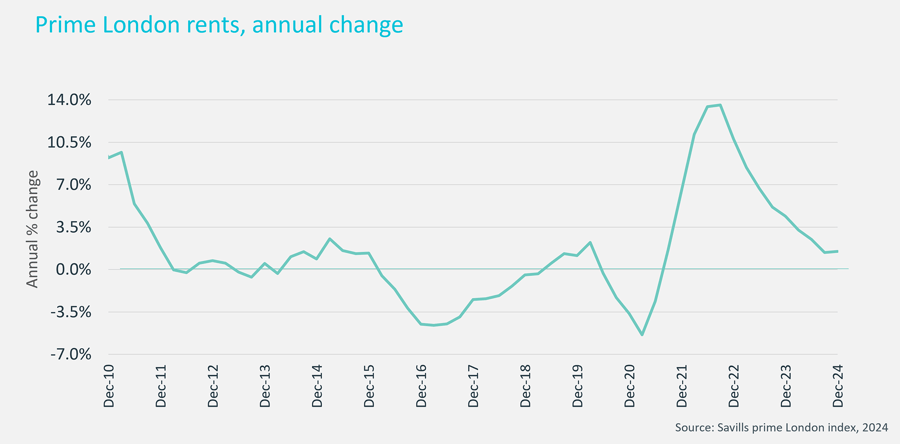

- Prime London rental growth stabilised at 1.5% in the second half of 2024

- There is strong demand for well-priced prime rental homes

UK rental market

Average UK rents rose by 9% last year, but the pace of growth is starting to slow, as growth hit 9.2% in March last year, according to official data from the ONS.

This strong level of growth is being boosted by lack of supply in the market and mortgage rates, which mean that some potential homebuyers are staying in the rental market for longer as they continue to save for a deposit to meet lending rules.

A more forward-looking measure of rental growth, the asking rent index from Zoopla, suggests that rental growth will slow further during this year. This index measures the rents advertised by landlords, but does not then reflect the rents agreed. It shows the average rise in asking rents had slowed to 3.9% in October last year, down from more than 9% in October 2023. This signals that even in the face of strong demand, affordability ceilings are being reached for rental properties after several years of strong rental growth.

In policy terms, the abolition of Section 21 no-fault evictions is a key change for the market, and will come into force as part of the Renters’ Rights Bill which has moved though the Commons very quickly since the Labour Government came to power, and will now be debated in the House of Lords after passing its third reading in the House of Commons. It is likely to be introduced into law in Spring this year. There is more on this in our blog. The changes to legislation will have limited impact on landlords who offer good quality properties, but some landlords may choose to review their portfolios in light of the new rules.

The extra stamp duty on the purchase of additional property from +3% to +5% introduced at the Budget in October last year, is an additional consideration for investors looking to enter the market or expand their portfolio, and is increasing the focus on looking for good value in the sales market.

Landlords also need to factor in regulation around Minimum Energy Efficiency Standard (MEES). The Government has said it wants the UK to reach net zero by 2030, meaning that there is likely to be a re-introduction of EPC requirements for those renting out property, likely meaning all properties must be rated EPC C by 2030. However, the Government are also consulting on the EPCs themselves, suggesting that the rating for domestic properties should be more robust, and include new metrics including carbon emissions, fabric performance and heating systems. This could push up the cost of gaining an EPC rating, but may make the grading more robust, as there are concerns at present that there is a large variation of ratings awarded by different inspections. The consultation by the Government, which is running until the end of February, is also considering reducing the time for which an EPC is valid. The current rating will run for 10 years, but the proposals include changing this to two years, meaning landlords will have to organise more frequent inspections. A study from Rightmove showed 2.9 million rental properties would need upgrading to bring rental stock up to EPC C standard (using the current EPC rating), at a cost of around £23 billion, or £8,000 per landlord.

Our agents report that property owners are increasingly exploring both sale and rental options when considering the next step for their property.

Find all the latest policy and tax updates on our blog.

Prime London rental market

Average rents in the prime London are some 20% higher now than at the start of 2021, as the market burst back into life after lockdowns came to an end. Affordability ceilings are being reached in some localities, and increased supply is limiting the scope for rental growth in the coming year. Average prime rents climbed by 1.5% in 2024, and rental growth settled at this rate during the second half of the year.

There is still a mismatch in some cases between rental expectations and demand in some areas of the prime market. The new market conditions mean that well-priced properties are attracting the most demand.

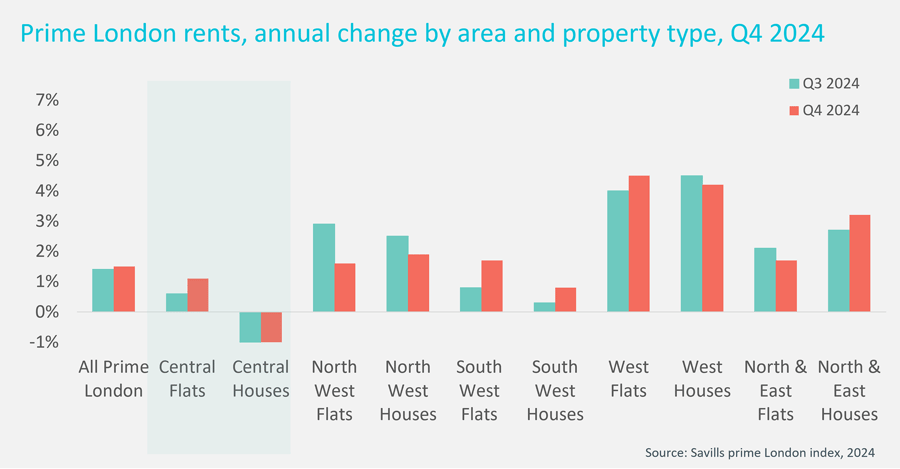

Rental growth is strongest in the North and East prime London areas, including Wapping and Islington, where rental growth for houses is still running at above 2%.

In prime central London however, the area that runs from Kensington to the City of London, average rents for houses ended the year down 1%, although they remain 22% higher than the trough of the market in early 2021.

The international nature of the prime London rental market means that those who want a base in the capital may look at renting rather than buying in the coming years, in the wake of further stamp duty rises, as well as the annual tax of enveloped dwellings (ATED) and the scrapping of the non-dom status. We expect prime London rents to rise by +3% this year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.