UK & London sales market update – January 2025

Activity in the UK housing market has been boosted by in recent months by rate cuts last year and buyers keen to beat the stamp duty deadline in April when lower thresholds for paying the tax are reinstated.

Volatility in the bond markets at the start of the year underlined how the UK’s fiscal position as well as the geopolitical uncertainty can affect borrowing rates. We expect rate cuts through 2025 will underpin 4% average UK house price growth this year, although if borrowing rules are relaxed for first-time buyers, growth could be higher.

Highlights

- Prime London prices rose marginally by 0.6% in 2024 after slipping by 1.1% in 2023

- Activity picked up in the second half of last year and that momentum continues into 2025

- Uk transactions will rise this year as stock levels climb

Prime London sales market

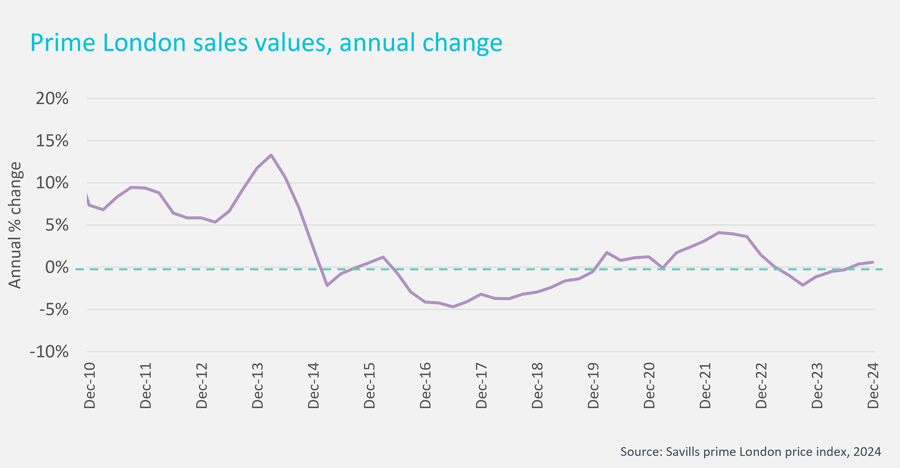

Average capital values in the prime London market have been largely flat for the last two years, ending 2024 up just 0.6%.

Demand picked up in the second half of last year, and there was sustained activity after the Budget when the Chancellor confirmed that the basic rate of stamp duty will be re-introduced in April, after being scrapped during the Budget in 2022. From April stamp duty will be payable at 2% between £125,000 and £250,000 for those moving home. First-time buyers will also be liable to pay stamp duty on purchases over £300,000, down from £425,000, and so many buyers are keen to complete their transaction before the deadline.

The move is ‘bringing forward’ activity, and so there may be a lull after the stamp duty deadline among buyers looking for a London pied-a-terre or investors. But the traditionally busier Spring period will just be ramping up, and another rate cut by then will likely underpin a rise in activity.

The Government is reported to be considering relaxing mortgage lending rules for first-time buyers, which would make it easier for those with smaller deposits to access the market. Also, the loan-to-income levels could be adjusted. Currently, only 15% of a lenders’ book of loans can be issued to those who are borrowing more than 4.5 times their income. If these rule changes come into force, this could drive more activity and underpin more price growth in domestically-driven prime markets.

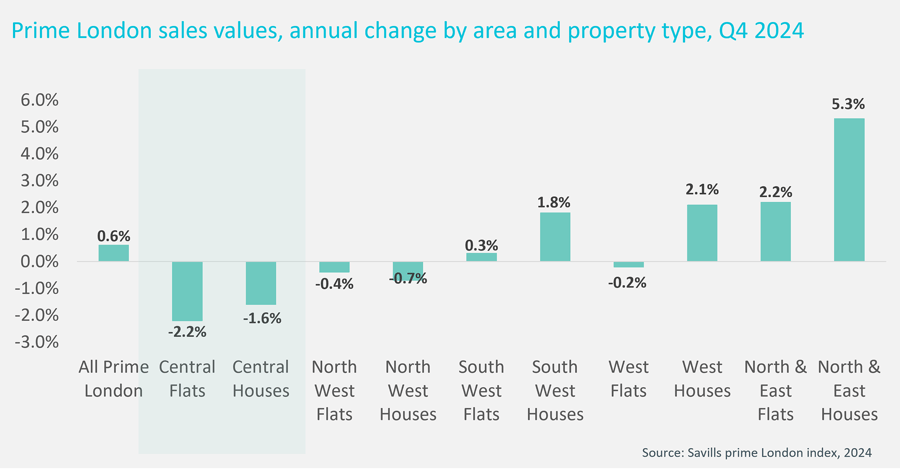

At the higher end of the market, tax changes, including the changes to the non-dom rules, could impact demand in some locations. Average values in prime central London fell by an average of -1.9% last year, and we anticipate that there could be another mild decline in prices in the central prime London market spanning Kensington to the City of London. However, prices in the more domestically-driven markets, including Tower Bridge, Wapping and Islington are likely to put in a stronger performance as buyers benefit from lower mortgage rates.

Increased stock coming to the market mean that competitive pricing is key in the prime London market, and this will put the brake on the headline rate of growth this year. We are forecasting a +1% rise this year, before price growth starts to gain some momentum in 2026 in a lower base-rate environment.

UK sales market

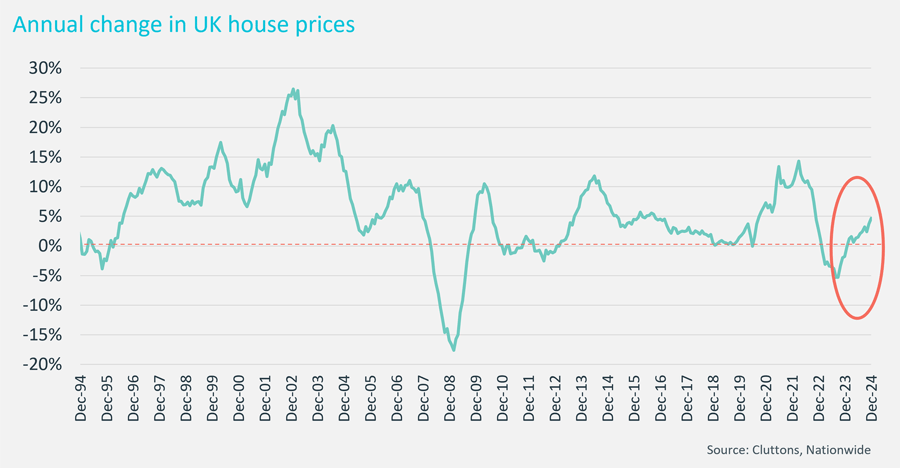

Average UK house rose by 0.7% in December after a 1.2% increase in November, taking the change in average house prices across the UK to 4.7% as activity was boosted by the upcoming change to stamp duty outlined below. As in the prime London market, some activity will have been ‘brought forward’ to the pre-stamp duty deadline, which could mean a slowing in the market in the next few months as the deadline to complete a sale before the end of March becomes too tight.

The Nationwide’s quarterly index shows a more modest annual growth of 3.6%.

However, rising wages and rate cuts through 2025 should underpin continued activity through most of 2025

If the Government relaxes mortgage lending rules for first-time buyers, a move they are reportedly considering, then this would also mean more activity among those climbing onto the housing ladder through the course of the year.

How stamp duty is changing

From April, the threshold for paying stamp duty on house purchases will fall from £250,000 to £125,000 for home movers, and from £450,000 to £300,000 for first-time buyers.

If these new rules come into force this year, the risk to our forecast will be on the upside, and house price growth could exceed an average of +4%.

Any rule changes would support markets where affordability is more of a barrier, largely markets in the South of England, where earnings to house price ratios are higher. In London, the HPE ratio is 8, while in the South East, it is 5.7%.

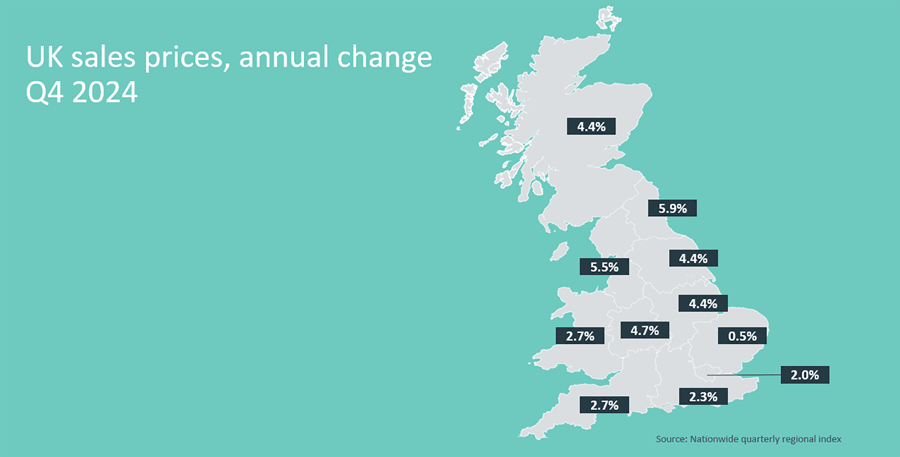

The importance of affordability in markets when it comes to house price growth is outlined by the map below which shows that over 2024, the highest level of price growth was registered in the Midlands and the North of England and Scotland, where the capital values are generally lower. The average home value in the North ended the year at £165,000, less than average value in the outer South East, at £336,000.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.