Commercial market update Autumn 2024

Economy: Political stability and looking for the next rate cut

The economy is so far providing a tailwind for the new government. Inflation has fallen, and economic growth has been more robust than expected. The early rate cut at the start of August was a close call, but it has provided a fillip to confidence across the board. The fact of the rate cut is itself significant, as it signals the country is now entering an era of falling borrowing costs. The markets are pricing in only one or more two cuts this year, with more reductions next year. Capital Economics are expecting rates to be approaching 3% by the end of next year.

There are still some risks in the economic outlook however, with recent pay data signalling that there could be some stickiness in this aspect of the inflation figures. Likewise, energy bill rises from October could put upward pressure on costs. There are also wider geopolitical risks around the ongoing crisis in the Middle East, the ongoing conflict between Russia and Ukraine, and the US election in November. The recent period of stock market volatility also demonstrated how quickly contagion can spread globally, albeit it might have actually served to make less liquid assets more attractive to investors.

The Bank of England has also upgraded its growth forecasts, providing more cheer for markets. The IMF now expects UK growth of 0.7% this year, up from its previous forecast of 0.5%. It predicts 1.5% GDP growth next year.

Property market overview

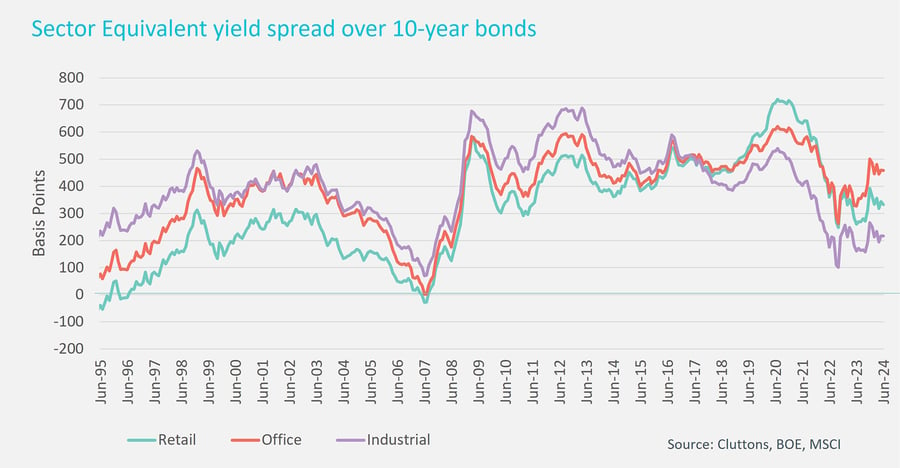

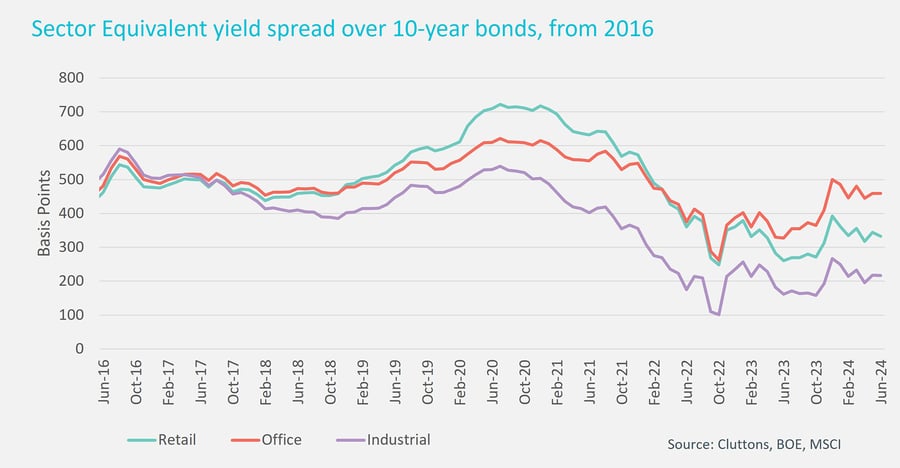

The spread between average equivalent yields and 10-year bonds has receded from the high late last year as gilt rates bounced back up. The spread for offices is back close to average levels, but this reflects yields being pushed up by secondary and tertiary office stock.

In many sectors, the re-basing of property looks to be close to complete. All property capital values, which have fallen 25% since the peak of the market in summer 2022, slipped by just 0.6% in the six months to June, and rose by 0.2% on the quarter, the first quarterly rise since June 2022.

As ever, the commercial property market remains very sector dependent and localised. Capital values for standard shops in wider London excluding central London rose by 1.3% in the three months to June, while in the wider South East, values for high street retail fell by 2.6%.

Interest rates are now on the way down, but re-financing will still be an issue for many property owners and investors as rates will remain significantly higher than the period of ultra-low rates in the decade before the pandemic. Some sales are happening as a consequence of sellers needing to reduce debt levels as a result of higher borrowing costs (impact on LTV and ICR).

There are signs that some investors are waiting in the wings for market metrics to meet their criteria, and this could lead to a bounce in investment that emerges quickly in the coming quarter.

As examined in more detail in our recent Commercial Property Examiner, we expect total all property returns to rise to 6.5% this year, from -0.1% at the end of 2023, mainly driven by income return.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Richard Moss

Partner, valuation & advisory – head of commercial UK funds

Head office

T +44 (0) 20 7647 7226