Economic update Spring 2024

The economy grew more than expected in November, according to the latest data from the ONS, but there is still a risk that the UK could dip into recession.

Key facts

- Economic growth will remain sluggish

- Faster than anticipated falls in inflation could spur earlier base rate cuts

- Mortgage rates are already falling

The economy grew more than expected in November, according to the latest data from the ONS, but there is still a risk that the UK could dip into recession, which is defined as two consecutive quarters of falling economic output. Even if the country avoids a recession, the outlook for economic growth is muted in the coming years.

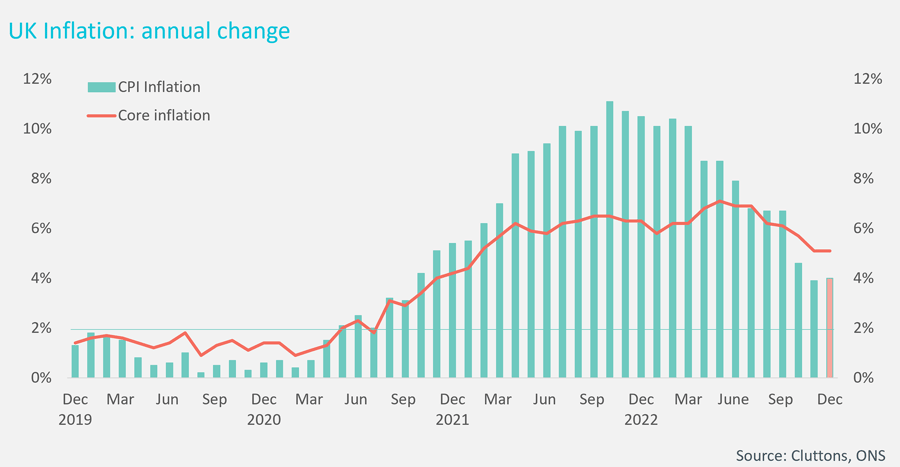

But this is not to say that all the economic news has been downbeat in recent months. Inflation fell quickly during the last half of last year. There was a surprise tick up in December, driven by higher transport and alcohol costs, but even so, CPI inflation ended the year at 4.0%, far lower than the January figure of 10.1%. These declines in inflation, barring any upwards surprises in the early months of this year, are enough to assume that the Bank of England will bring forward the date when it starts to cut rates.

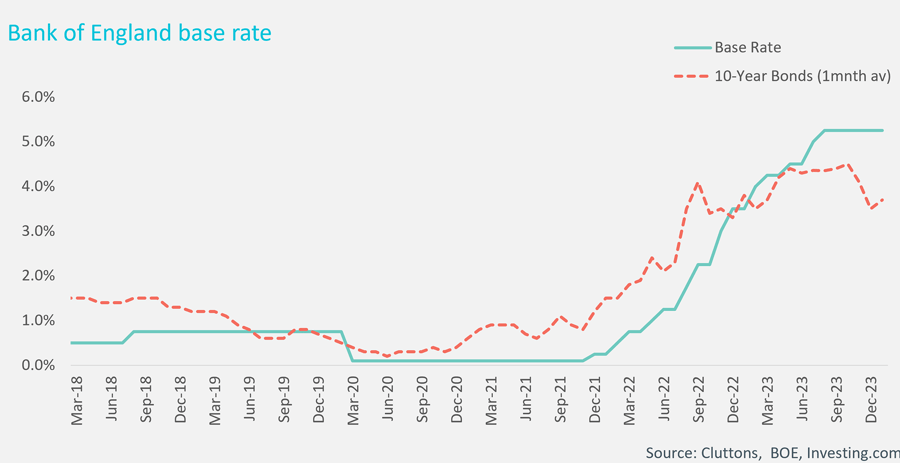

Most economists are now expecting rates to be trimmed in May or June, and forecast that they will end the year at 4% – good news for mortgage borrowers, who have already seen mortgage rates cut as money markets factor in these future falls.

This can be seen in the table below – with 10-year gilts, one of the measures of the cost of future funding, already falling from late last year, despite no change in base rates, as the money markets factored in the strong signals that base rates had peaked and would be cut sooner than expected.

The caveat here is that inflation is not guaranteed to continue falling at the same speed as witnessed in Q4 last year, especially if there is any intensification of the crisis in the Middle East, or if wider geopolitical tensions worsen. If inflation started to rise sharply, the Bank of England would be highly unlikely to cut base rates.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.