UK & London sales market update Spring 2024

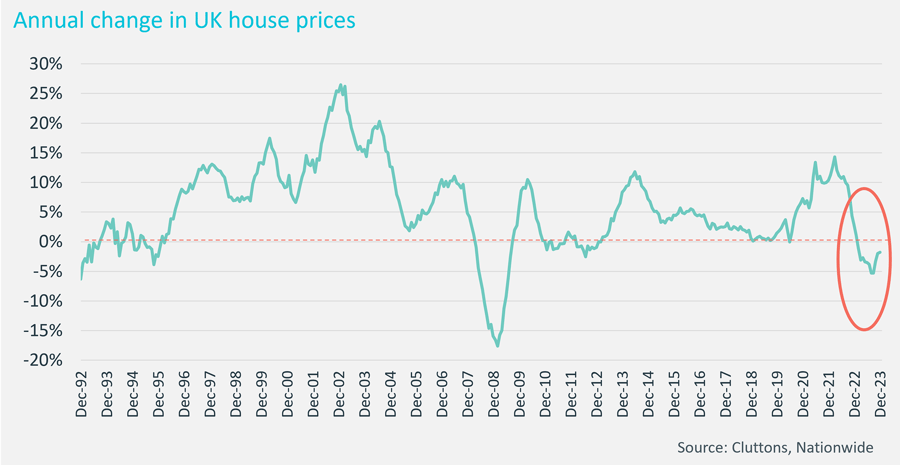

Average annual UK house prices falls hit a low of -5% in September last year, but have since moderated to around -2%.

Highlights

- Falling mortgage rates have boosted sentiment and sales activity is starting to rise

- Average UK sales values were down -2.3% in Q4 compared to Q4 2023, according to Nationwide

- Cluttons forecasts modest rise in prices next year, before more substantial growth in 2025

| Year | UK House Prices | Prime London Prices | Prime London Rents |

|---|---|---|---|

| 2023 | -2.3% | -1.1% | +4.4% |

| 2024 | +1.0% | +0.0% | +2.5% |

| 2025 | +4.0% | +3.5% | +3.0% |

UK sales market

Average UK house price falls started to moderate in October. In September, values were down more than -5%, but by the end of the year, prices were down just -1.8% on a monthly basis and -2.3% on a quarterly basis. One factor here was the almost immediate reaction to sharply falling inflation, and the Bank of England’s decisions to stop raising interest rates, which made it clear that base rates had probably reached their peak. This in turn, meant that the money markets started factoring in base rate cuts earlier this year, which in turn cut the cost of funding – allowing mortgage lenders to start cutting mortgage rates. While those remortgaging will still have to find more money, hundreds of pounds a month in many cases, when they take out a new loan, the additional expense this year will be less than it was last year.

However, while the market has been protected from large price declines, the pressure on the market has been evident elsewhere – namely in the number of transactions being carried out. Activity slowed sharply in Q3 and most of Q4, although there are signs that it started to pick up in December and into January. The latest data from the RICS survey of agents shows that in all regions of the UK, except the North of England and the West Midlands, expect sales volumes to rise in the next three months. Mortgage approvals data also signals a rise in activity which will result in an increase in sales – albeit off a low base.

London & prime London sales market

Price falls are also easing in the London and prime London markets. Average values in London were down -2.4% at the end of 2023, according to Nationwide’s data, compared to -4.3% annual decline in the summer.

London’s market has been more resilient in terms of pricing than anywhere else in the South of England, as shown in the map above. New data out from Zoopla shows a bounce-back in buyer demand at the start of this year, with London leading the way.

In the prime London market – the top 5-10% of properties in areas largely clustered in zone 1 – average values ended last year down -1.1%, compared to an annual rate of decline of -2.1% in Q3.

Just as the change of tone on base rate rises last September provided a fillip to the wider UK market, it also had an impact on the prime London market, with an improvement in sentiment. Sales values have also been most resilient in the prime central London market.

However, there is still some distance between buyers and sellers around pricing in some instances, causing a slowing in sales progression, and the number of sales. Zoopla data signals that one in four sellers in London and the South East of England are still having to accept a discount of at least 10% from the asking price to secure a sale, highlighting that the market remains price sensitive.

As we move into 2024, agents are reporting a pick-up in activity, signalling a rise in sentiment about the market, and pent-up demand coming back to the market. Sales agreed in London were 13% higher in the first three weeks of January compared to the same period last year, according to Zoopla. As we move through the year, and mortgage rates continue to fall, activity will rise further

This year’s General Election introduces new factors into the market given that the Labour party have pledged to add another 2% stamp duty surcharge on overseas buyers, and to abolish the non-dom tax status in favour of a narrower, more targeted scheme. The polls currently suggest that Labour will win the election – and so the stamp duty increase could prompt a flurry of activity before the election. However, the change to the non-dom regime could affect demand in the prime central London areas to some extent, especially if there is any uncertainty over the replacement scheme.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.