Economic update Q3 2025

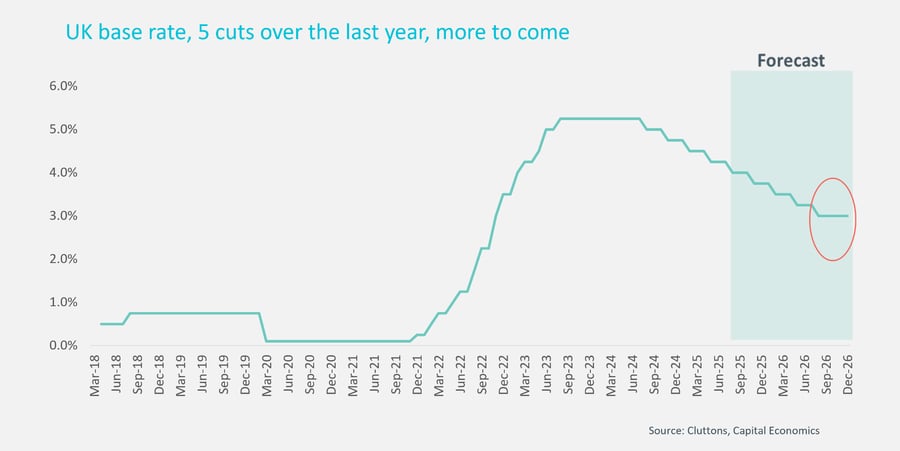

The Bank of England delivered the much-anticipated August base rate cut, reducing the base rate to 4%, from 4.25%.

More tariffs being applied by the US will increase global uncertainty, and potentially put upward pressure on inflation, while discussions of tax rises in the Autumn will affect consumer spending and consumer confidence in the UK.

Key facts

- Base rate cuts this year will spur more activity in the housing market, although the modest rebound in the rate of price growth will take longer to come through amid greater UK economic and policy uncertainty

- As a result, we are revising our forecasts for the UK mainstream sales market, predicting headline price growth of +2.0% this year (down from +4.0%) and +4.0% growth next year (up from +3.0%)

- We are also recasting our forecasts for the prime London market, expecting prices will end the year down -2.0%, compared to our previous expectation for +1.0% growth

The UK economy contracted in April and May, contrary to expectations and creating worries that the economy is flatlining. After rising by a faster than expected 0.7% in Q1, the UK’s GDP dipped unexpectedly in May, and with the figures suggesting that the activity in the first three months of the year was a result of businesses and individuals rushing to beat US tariffs, national insurance and stamp duty changes. While initial indicators suggest that economic activity may be starting to build again, this data creates a headache for the Treasury where policymakers were counting on economic growth to deliver tax receipts to help balance the books.

However, this news was also mulled by the Bank of England as it made its August rate decision. As highly anticipated, it has cut rates by another quarter point to 4%, marking the fifth quarter point cut since rates were at their peak at 5.25% a year ago.

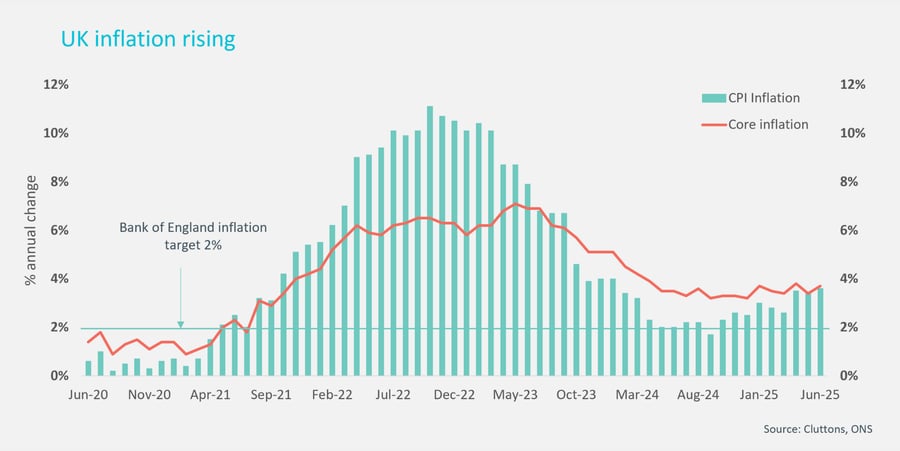

The MPC will continue to track inflation data however, with the CPI measure of the cost of goods and services rising by 3.6% year-on-year year in June, up from 2.6% in March, driven up by higher food and energy prices. The Bank targets a 2% inflation rate on a 2-year horizon, and the Bank’s most recent report on the economy suggested it expects inflation to return to 2% in that timeframe, freeing rate-setters to cut rates in August, even with higher headline inflation numbers.

While the global discussion on tariffs has been relatively quiet in recent months, thanks to the 90-day pause introduced shortly after US President Trump’s big announcements in April, tthey are now coming back to the fore as the higher tariffs are now coming into force. The EU struck a deal for 15% tariffs for most goods, down from the 30% initially announced. The UK announced a deal at the end of June, with a 10% tariff on most UK goods being exported to the US. Even though this is a preferential deal for the UK, it will still mean extra expense for exporters, and the second-round effects of more global uncertainty as more countries try to strike deals with the UK may also put upward pressure on prices.

At the same time however, economic growth is set to remain relatively flat, with possible tax rises in the Autumn putting a further brake on consumer sentiment, and ultimately consumer spending. This would open the way for interest rates to come down further, but only if inflation remains contained. Capital Economics predicts that rates will fall to 3% by the middle of next year.

This will be good news for mortgage borrowers on tracker loan deals fixed to the Bank base rate. But the picture is slightly more complicated for the wider mortgage market, as swap rates, the money market rates which determine the cost of mortgage pricing, have been drifting up in recent months, reflecting the rise in gilt yields. With expectations of more rate cuts now rising, swap rates have started to fall back a little, but many fixed-rate mortgage deals may well already be pricing in the next rate cut or two. The best two-year fixed-rate deal currently on the market is around 3.8% for those with a 40% deposit or at least 40% equity in their home, below the current base rate of 4.0%.

Lower mortgage rates spur more activity in the market as more borrowers can access finance, and this will put some upward pressure on prices, which are softening across the country. The Nationwide index showed a 0.5% decline in average house prices in the three months to the end of June, the first quarterly fall since the end of 2023. The annual change in average prices is at 2.1%, the lowest rate since July last year, and down from 4.7% in December last year. The market was boosted in the early months of the year as buyers moved to beat the stamp duty rises re-introduced at the start of April, and as activity slowed after the deadline, this put downward pressure on prices. While we expect prices will rebound, especially as interest rates decline, the recovery may take longer than previously anticipated.

The forward-looking indicators of activity in the sales market are still sluggish, such as the RICS new buyer enquiries monitor. Also, consumer confidence is likely to be affected by talk of rising taxes, which could mean some buyers hold off until after the Budget. The U-turn on the welfare bill has left the Chancellor with a £6 billion hole in her finances which she will have to address at the Budget in the Autumn, and at present it seems that it will be challenging to avoid raising taxes in some shape or form.

As a result, we are adjusting down our UK house price forecasts for this year, to +2.0% growth this year, down from our initial forecast of +4.0%. However, we are revising up our forecast for 2026, to +4.0% growth, up from 3.0%.

| Year | UK House prices | Prime London sales | Prime London rents |

|---|---|---|---|

| 2024 | +3.6% | +0.6% | +1.5% |

| 2025 | +2.0% | -2.0% | +3.0% |

| 2026 | +4.0% | +3.0% | +3.0% |

| Source: Cluttons |

Considering whether to consolidate or expand your portfolio?

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.