Prime London & UK sales market update Q3 2025

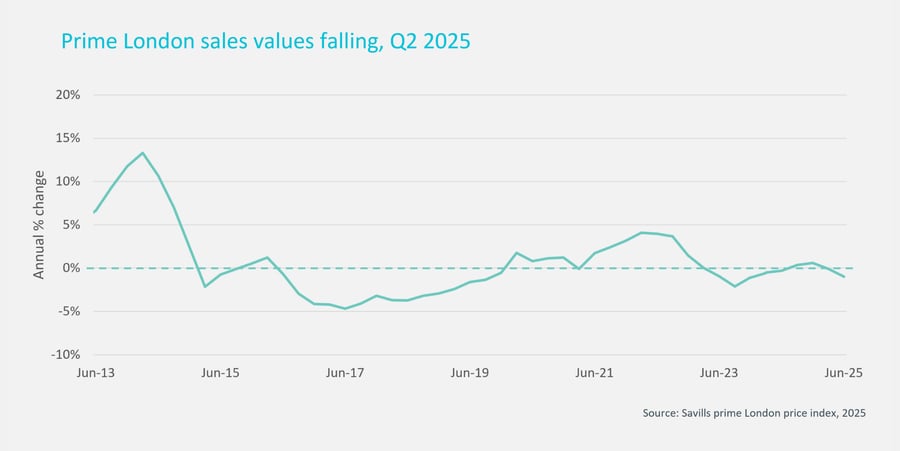

Sales price growth is slowing across all markets, with prime London pricing dipping back into negative territory in the year to the end of June.

The prime London market is becoming ever more localised, with the market moving at different speeds in the centre compared to the prime outer areas, and also across price brackets.

A more challenging policy landscape coupled with higher stamp duty rates has put the brakes on price growth, especially at the super-prime end of the market.

Prime London sales market

Key facts

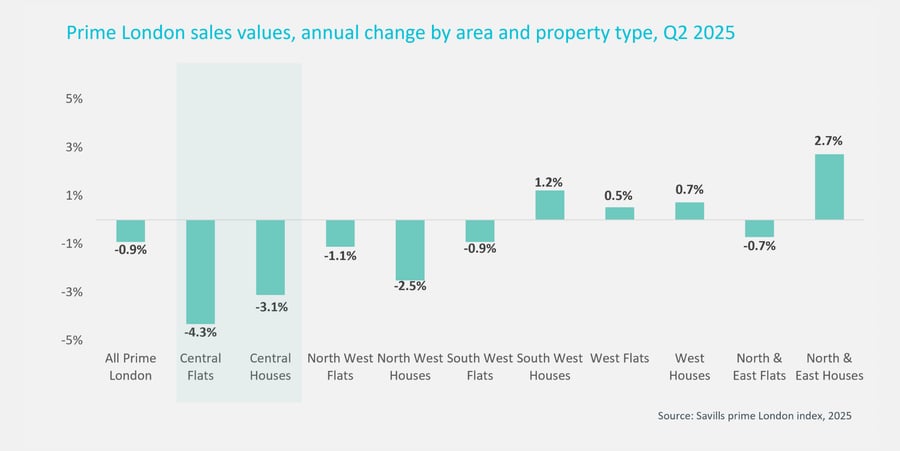

- Average prime London prices are down -0.9% on the year and are 7% lower than June 2015

- Prime central London prices are down -3.7% compared to June 2024, and have declined by nearly 20% over the last 10 years

- We have revised down our forecasts for prime central London pricing this year, and we are now forecasting an average -2.0% fall at the end of 2025

The policy landscape for the housing market in prime London has become ever more challenging since the peak of the market in 2015. Since then, stamp duty rates have been repeatedly raised, and changes in personal tax rules for many of those with homes in prime central London (PCL) have also affected the market. The rapid rise in interest rates in September 2022 stopped the small recovery in pricing during the pandemic, and there was further pressure on the market as many high net worth individuals who are non-doms prepared for this April’s tax changes by re-locating away from London. The discussions to extend the reach of the UK taxman to all worldwide assets for inheritance tax was enough to encourage an even greater number of non-doms to leave in recent months, although there are now hints that the Government may row back on this.

The exception here has been the arrival of US buyers into the luxury London market – US citizens already pay US tax on their worldwide income and assets, and there is a tax treaty with the UK to avoid double-paying.

As weaker economic growth and policy moves, such as the changes to the welfare bill, create a larger hole in the Treasury finances, attention has turned to how the Chancellor will raise more money in the Autumn. Discussions around wealth taxes have once again come to the fore, and despite apparently being ruled out at Cabinet, the chat continues. Extending the rates of capital gains tax (CGT) on property to more closely align with income tax has also been mentioned, although this was also discussed before the Budget last year, and there was no change.

Even so, the uncertainty around the direction of policy means that some buyers will adopt a ‘wait and see’ approach, which will put further downward pressure on prices at the top-end market which are already being affected by the departure of international homeowners. If there is more sustained discussion around CGT changes, those wanting to sell a property in the next year will want to put it on the market before the Budget, and could create more supply in the market, and put downward pressure on prices.

The whole of the London market is also being affected by the increased cost of living, especially as affordability for homes in the capital is stretched compared to other key UK cities. Yet the cuts to interest rates have spurred buyer interest, especially in more domestic-driven markets. Likewise, the loosening of mortgage stress tests has made home loans more accessible for some borrowers.

There is evidence that family homes in prime markets slightly outside PCL are proving more resilient. Average house prices in the North and East prime London, stretching from the east of the city to Islington are still up 2.7% on the year, although they fell 0.6% on the month in June signalling that this market may also be starting to weaken.

In contrast, average prices in prime central London are down -3.7% on the year, and are down nearly 20% over the last decade.

Overall prime London prices are down -0.9% on the year.

Agents report that well-priced homes are still attracting buyer interest, but that the asking price must reflect the realities of the current market.

We believe that the prime market will pick up next year as long as there is increased certainty around the policy and tax landscape, and amid lower interest rates. Some investors are already finding value in the market. However, we believe this year will be more challenging for sales prices than previously expected, and we are revising down our forecasts for prime prices this year to -2.0%. Prime central London prices are likely to end the year down -3.5%.

UK sales market

Key facts

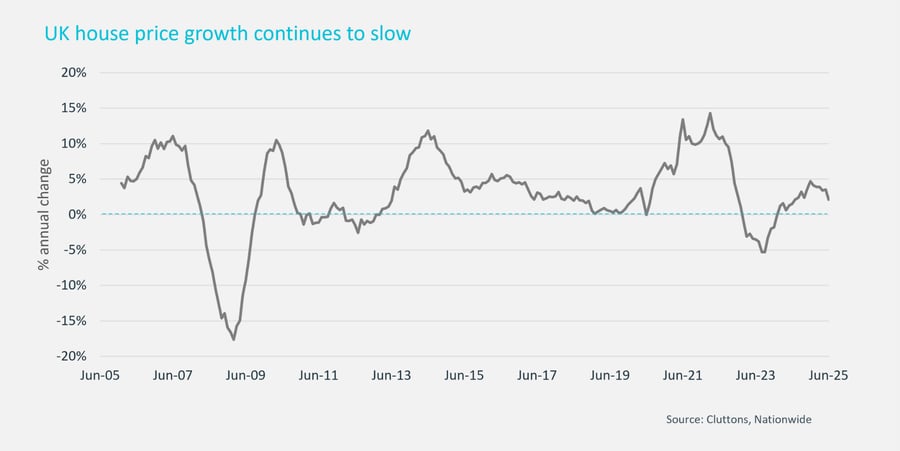

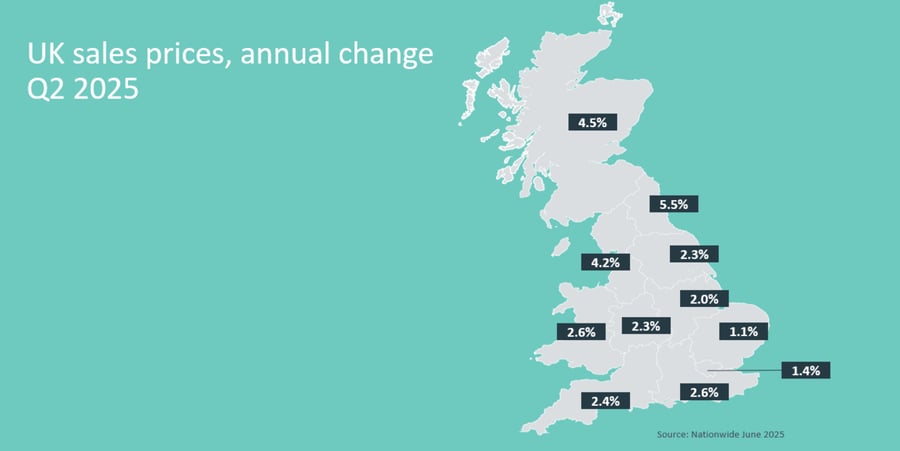

- Average house price growth slowed to 2.1% in June

- Supply has risen strongly with a record number of homes on the market according to Zoopla

- Buyer demand is also up in key UK cities, but the additional supply of homes as well as higher stamp duty rates are weighing on price growth

There has been a summer bounce in sales market activity across the UK in recent months, with demand and supply both rising, according to the latest data from Zoopla. As discussed above, the loosening of mortgage stress tests since March this year has also increased access to home loans for borrowers, creating more demand in the market. Also, the base rate cuts since summer last year have reduced the cost of mortgages.

However, even with a busy market, additional stamp duty costs and the higher levels of supply are acting as a drag on pricing across the board.

In addition, markets where affordability levels are higher, such as the North of England and Scotland, are registering higher price growth than the rest of the country.

And while the four rate cuts registered since summer last year have been a welcome boost for the market, the rate cuts this year have materialised more slowly than anticipated. It is likely there is another rate cut coming in August, although mortgage rates seem to have already priced in this change.

However, we are expecting more rate cuts towards the end of the year and into next year, which should bring down mortgage rates further, especially if there is some certainty on the global economic and UK political landscape.

As a result, we are revising down our forecasts for house price growth this year marginally to +2.0%, down from +4.0%, but we are expecting +4.0% growth next year, up from our initial forecast of +3.0%.

Considering whether to consolidate or expand your portfolio?

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.