Prime London sales market Q3 2023

Price growth in the Greater London market was more subdued than in some other parts of the country during the pandemic.

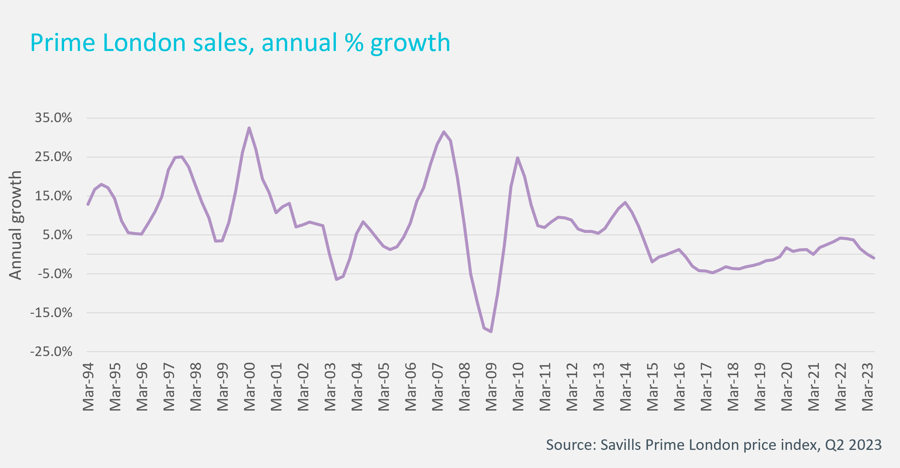

According to Nationwide figures, average prices in London are now 9% higher than Q2 2020, compared to a national average of +19%. Average price growth in prime London came in slightly lower, at 4% between Q2 2020 and Q2 2023, according to Savills prime London index.

There was plenty of activity in the London market last year, with the number of transactions in London accounting for 14% of sales in England & Wales in 2022, compared to 11% in 2021. However, the upward pressure on prices was muted by several factors. First was the limited buyer demand from overseas during the teeth of lockdowns, when overseas travel was all but stopped. Second were the higher capital values of homes in the capital, meaning that that the headroom for price growth was not as expansive as some other areas of the UK.

The shock of last September’s mini-budget, where the fact of rising interest rates were brought into very sharp focus caused a ripple in the market, as have the recent sticky inflation figures and rises to the base rate. Potential buyers dependent on mortgages have had to review which homes are within budget as affordability stress tests become more onerous. However, in the prime London markets, not all buyers are dependent on mortgages. Agents report that cash buyers are active in the market – including those from overseas who are benefitting from the relative weakness of the pound against the dollar.

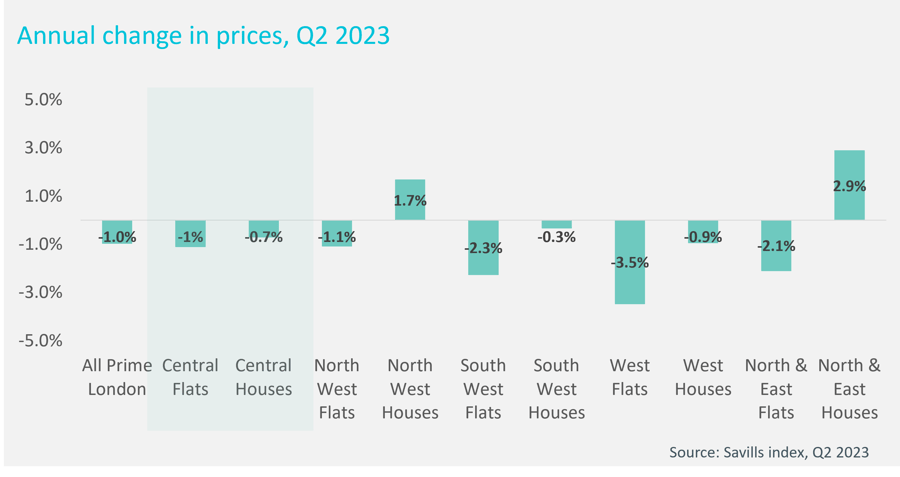

However the sales market is price-sensitive. Well-priced homes are still attracting attention, and in some cases, competitive bidding, but demand remains muted and this has been enough to take the upwards pressure out of the prime London market, with average values down 1% in the year to June.

Houses in some parts of the prime market are outperforming as buyers are still drawn to outside space, but the momentum in pricing is set to slow for the rest of the year, although we forecast the average price downturn in this market will be less pronounced than in the wider UK housing market at -4% for the year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.