UK economic outlook Q3 2023

The economy settled down relatively quickly from the shock of the mini-budget in September last year and the resulting spike in gilt rates and mortgage rates.

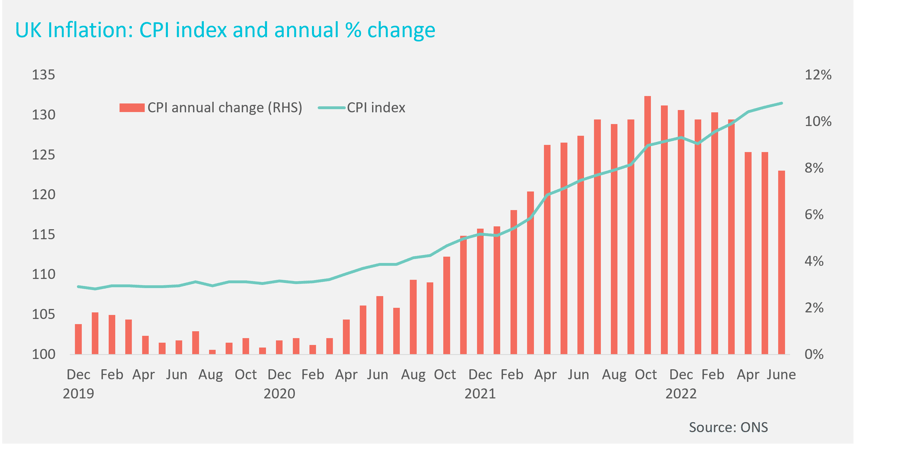

The cost of borrowing receded as the political reins were handed over to Rishi Sunak and Jeremy Hunt, resulting in brighter sentiment and higher levels of activity in the first half of the year. However, in May, it started to become clear that inflation, which the Bank of England had forecast to fall back quickly, was proving ‘stickier’ than expected. The CPI inflation reading for April (released in May) was higher than anticipated, and May’s data (released in June) disappointed again – showing that core inflation was actually still rising.

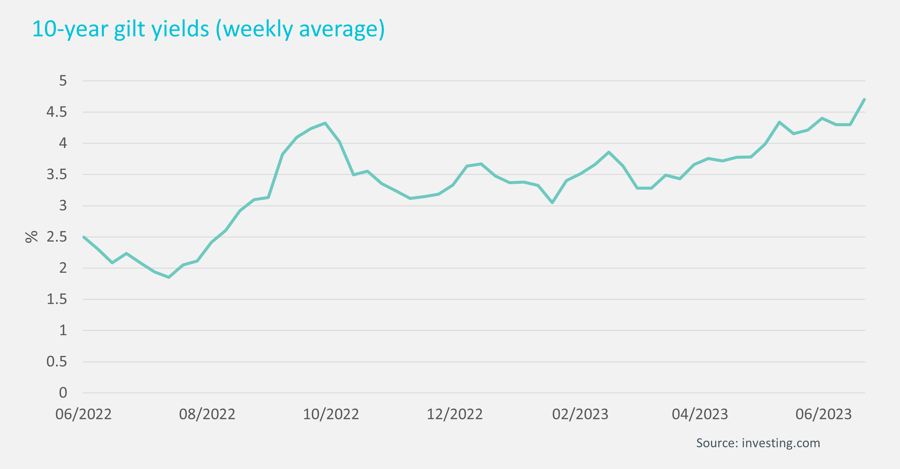

Up until the first surprising inflation figure, economists had expected the Bank of base rate to peak at 4.25% or 4.5%. In the months since then expectations have risen sharply, with some forecasting the base rate will exceed 6%. It is currently at 5%. Gilt rates have also risen sharply, and this has driven up the cost of fixed-rate mortgage pricing. For those on fixed-rate mortgages that need to be renewed this year and next, there will be a payment shock.

Better than expected inflation data for June, showing an annual rise of 7.9%, indicates that inflation is indeed falling back. It is still high, and will be unlikely to be enough to stem further base rate rises, but it will raise hopes that base rates don’t need to rise as fast or as far as had been previously expected.

Policymakers have ensured that lenders use all tools at their disposal – for example, extending the mortgage term or moving borrowers to interest-only deals – for borrowers who are struggling to meet higher repayments. Those who took out a mortgage in the last eight years have already been through ‘stress-testing’ to ensure they can meet higher repayments. The challenge is that these higher repayments come as the cost of living has risen, putting more pressure on other areas of household finances.

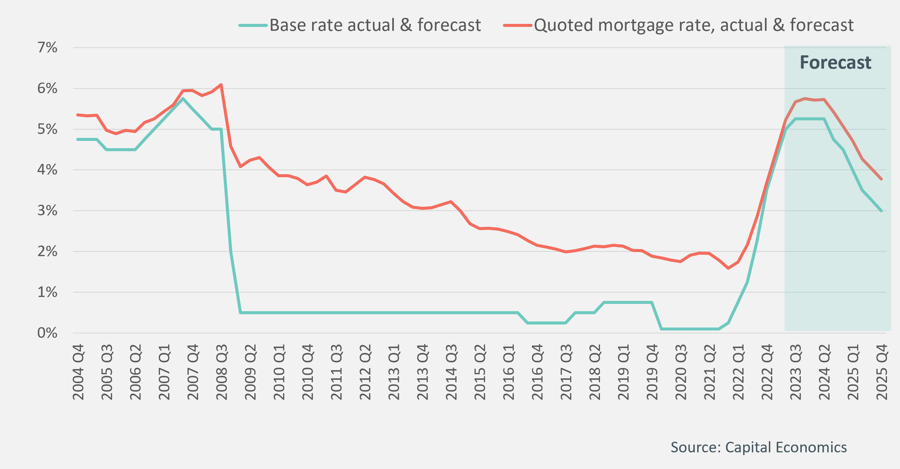

The key question is when will rates start to fall back? Economists are no longer forecasting a rapid decline in rates early next year – rather a slower downward movement later in 2024. More homeowners will have to re-mortgage at higher rates, which will have an impact on consumer sentiment – in the housing market and further afield.

It is also worth noting nearly 9 million households own their homes outright in England (compared to 7 million homeowners with mortgages) and will be feeling minimal impact from rising mortgage rates, although the rise in the cost of living affects everyone. The Bank of England has said that 4 million borrowers will roll onto higher-rate deals in the coming years, paying an average of and extra £220 a month. Some 1 million borrowers will be paying an extra £500 a month by 2026, according to the central bank.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.