UK & London sales market update Q2 2025

Activity in the UK housing market was boosted in the first three months of the year as buyers rushed to beat the change in stamp duty thresholds at the start of April.

However, our agents report that prime London markets have maintained momentum in April, and this is likely to be underpinned by further rate cuts and falling mortgage rates this year.

Highlights:

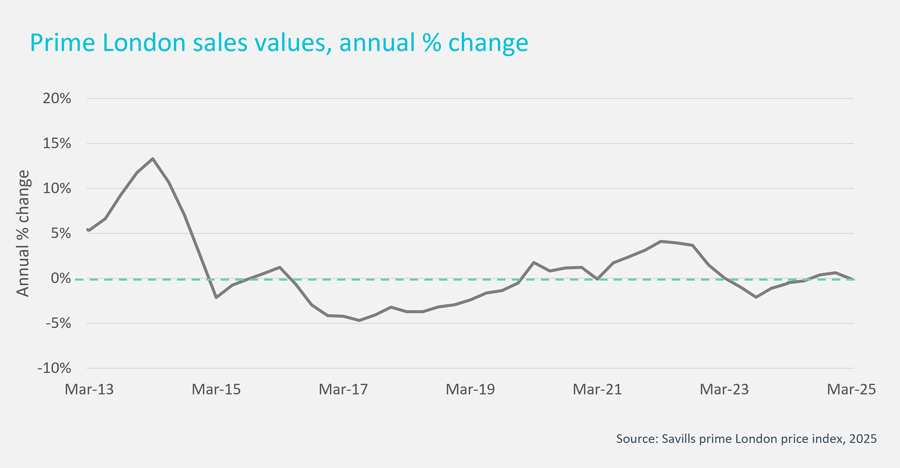

- Prime London prices down just -0.1% in the year to March, although values in prime central London dipped -2.6%

- Activity in the prime London market remains higher than last year, but pricing is key

- UK sales transactions will continue to rise this year, as stock levels climb

Prime London sales market

Average sales prices across the prime London market, which runs from Ealing to Canary Wharf and Hampstead to Wimbledon, have remained flat in the year to March, falling by just -0.1%. However, in the prime central London (PCL) market, which encapsulates higher value properties in the City of Westminster and parts of Kensington & Chelsea, average values have been falling – albeit modestly – since the summer of 2023. However, these declines picked up momentum in the first three months of the year, with average values now down -2.6% on the year, and -3.8% since June 2023.

Values in PCL are being affected by the rises in stamp duty introduced for higher-value and second homes over the last decade, as well as the changes to the non-dom tax regime which has prompted some non-domiciled residents to relocate to other global centres. A rise in stock coming to the market also means that it is moving towards a buyer’s market, and this may lead to more activity, where buyers and sellers can align on pricing. Over the last quarter Cluttons’ agents have noticed an increase in engagement from Middle Eastern and US buyers, who are increasingly attracted by London and the stability it offers in comparison to the volatility elsewhere.

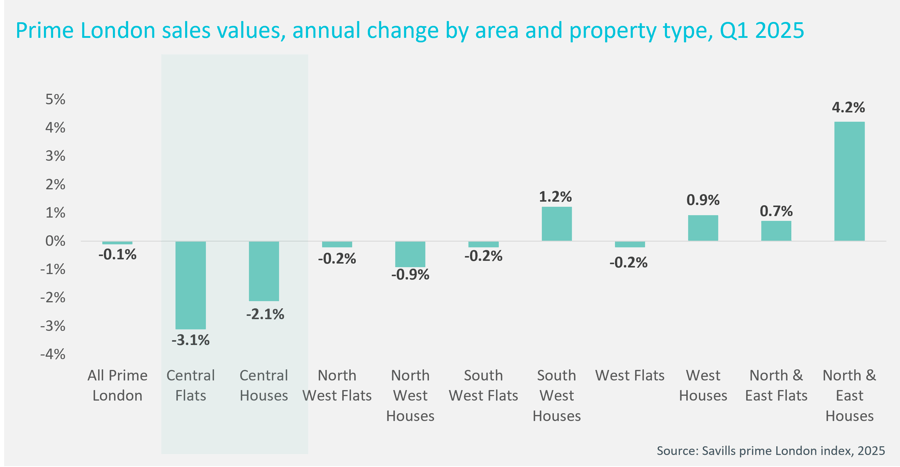

Average prices in the more domestically driven prime markets, including east London and Islington showed growth of over 2%, signalling the continued demand from families needing to move. This is underpinning an outperformance for houses over flats in most areas of prime London.

Downward movement in base rates this year, as examined more fully in our economic update, will boost demand in the market especially for homes which are competitively priced. For those buyers looking for mortgages, a relaxation in stress-tests will also boost budgets. Halifax, HSBC and Santander are all moving to change their mortgage affordability calculations, which will allow thousands of borrowers to access substantially more in mortgage funding. Stress tests were introduced in the wake of the global financial crisis to ensure that, should interest rates rise from their ultra-low levels, borrowers would still be able to afford repayments.

We forecast prime London sales prices to rise +1% this year as increased activity underpins pricing, but the risks for this outlook lie to the downside.

UK sales market

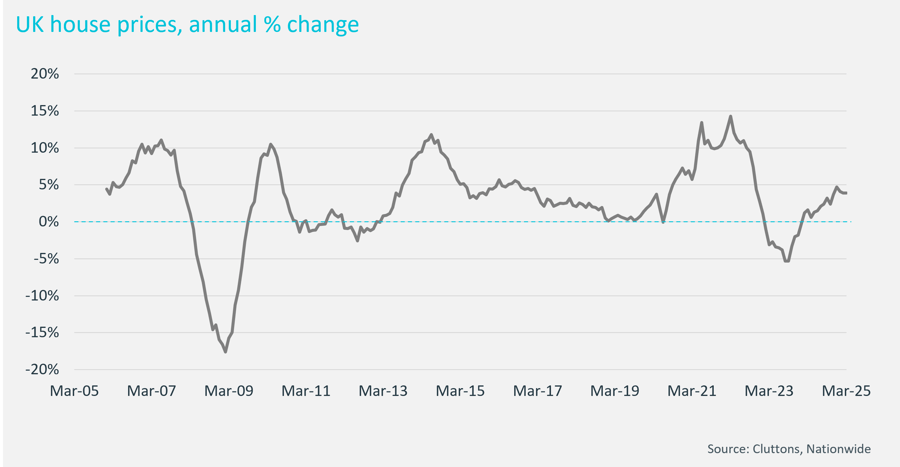

Average UK house prices fell in April, taking the annual rate of growth to 3.4%, down from 3.9% in March, and down from 4.1% in January. Market activity increased in the run up to April’s stamp duty changes as buyers rushed to complete purchases before thresholds for paying tax rose, which spurred a rally in pricing. However, this looks to be easing according to the latest data from Nationwide.

This is also echoed in the Zoopla price index data, which is seen as a leading indicator in the market. This data also highlights the wide geographical differences in sales markets across the UK. Data from the property portal shows that buyer demand in the West Midlands, North West and North East of England all rose by 15% or more in the month to mid-March, compared to the same period in 2024.

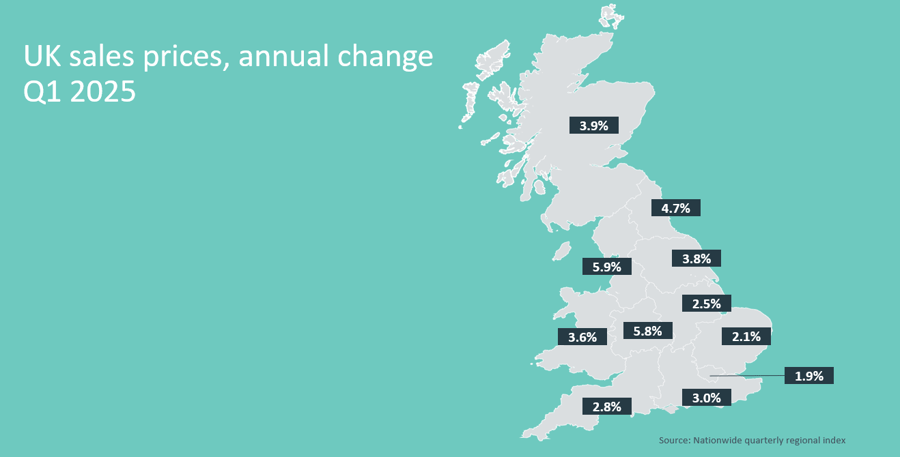

The supply of homes for sale in these markets rose by 5% or less over the same period. This imbalance is helping drive stronger price growth in these markets, which already have lower price to income ratios – making them more affordable – than homes in the South of England. Average home prices are up 3.0% in Liverpool, 2.9% in Manchester and 2.5% in Newcastle in the year to March, according to Zoopla’s price index, above the UK 1.8% average.

In contrast, the stock of homes for sale in the South West of England has risen by 20% on the year in the month to mid-March, while demand has risen by only 6% or 7%, resulting in an annual price rise of just 0.9%, according to Zoopla. These trends, of higher house price growth in the North and the Midlands is also evident from Nationwide data, as shown in the map below.

As examined in the prime London focus above, the outlook for base rates this year could impact the market. We are expecting two further rate cuts this year, taking the base rate to 4% by the end of the year, although the chances of rates ending the year at 3.75% are rising. Falling base rates, and a relaxation in mortgage stress-tests, as already announced by three major lenders, will increase buyers’ ability to climb onto or up the housing ladder, and will result in more activity in the market this year, which will continue to underpin price growth, especially in markets where affordability ratios are already lower.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.