UK & London rental market update Q2 2025

Demand in the rental market remains strong, although the large imbalance between supply and demand has narrowed in some markets, meaning rental growth has moderated although a lack of supply is still driving rental growth.

New legislation, namely the Renters’ Rights Bill, could lead to a further contraction in supply – read about the proposed rules in more detail on our blog.

Highlights:

- Average UK rental growth was 7.7% in the year to March, according to official ONS data, while a more forward-looking indicator from Zoopla signals average UK rental growth has slowed to 3%

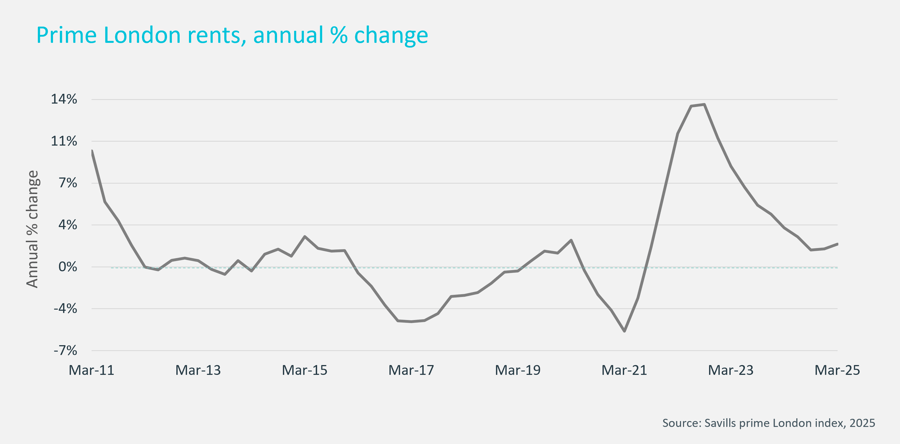

- Prime London rental growth rose on an annual basis to 1.9% in the year to March, up from 1.5% rise in year to December

- The market is more price sensitive, but demand remains strong for well-priced homes

Prime London rental market

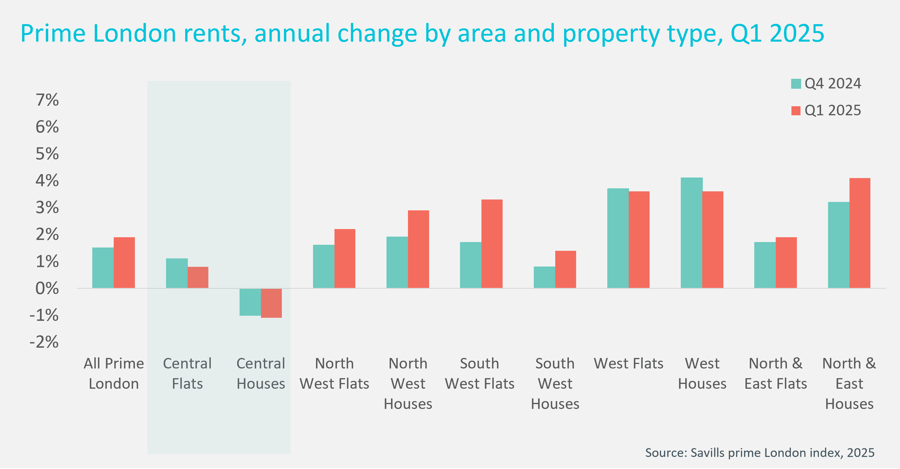

Demand for rental properties in the prime central London market remains robust, especially for competitively priced properties. Family homes in outer prime London remain sought after, amid constrained supply, and this is putting upward pressure on rents. For example, the average rent for a family home in the North and East of London is up 4.1% on the year, compared to a 1.9% rise for an apartment.

In prime central London this trend is reversed, with a modest 0.8% rental growth for flats on the year, while rents have fallen for houses, down 1.1% compared to March last year. Overall, rents in PCL are still more than 20% higher than in the Spring of 2021, but landlords who take into account recent price movements will have a better chance of attracting strong interest in their property. Well-priced properties are attracting the most demand across all Cluttons’ offices.

The international nature of the prime London rental market means that those who want a base in the capital may look at renting rather than buying in the coming years, in the wake of further stamp duty rises, as well as the annual tax of enveloped dwellings (ATED) and the scrapping of the non-dom status. Increased legislation, especially the Renters’ Rights Bill (RRB) which is likely to come into force this year, and future rules around energy efficiency ratings in rented properties, may cause a slowdown in supply as some landlords choose to exit the market, which will put further upwards pressure on rents. We expect prime London rents to rise by 3% this year.

UK rental market

The official rental data from the Office for National Statistics paints a rosier picture of rental growth than some other measures. Average UK rental growth was 7.7% in the year to March, according to the ONS, down from 8.1% annual growth in 2024. A more forward-looking indicator from Zoopla signals average UK rental growth has slowed to 3% in the year to January, down from 7.4% a year ago. All indices are aligned, however, in showing a slowdown in rental growth after the very strong rises seen during and in the wake of Covid.

While the large demand and supply imbalance that has underpinned strong rental growth recently has started to unwind to some extent, there is still strong demand in the market.

Mortgage rates are significantly higher now than at the end of 2021, when the Bank of England started to ramp up the base rate, and as a result more potential homebuyers are staying in the rental market for longer as they continue to save for a deposit to meet lending rules. Base rates are starting to fall back, with more cuts expected this year, and mortgage lenders are also relaxing stress tests which will help more first-time buyers climb onto the housing ladder.

However, as changes in the lending market may allow some renters to leave the sector and ease demand, the likelihood is that supply will remain constrained due to upcoming legislative changes. The Renters’ Rights Bill is expected to become law this year, and while everyone in the sector welcomes rules which create a more secure tenure for renters, some of the changes around gaining possession of a property may prompt landlords to review their portfolio or even sell their property. Likewise, investors may decide that the expense of meeting new energy efficiency rules coming into force in the near future may not be viable, and again, this will put further pressure on supply.

The extra stamp duty on the purchase of additional property from +3% to +5%, introduced at the Budget in October last year, is another consideration for investors looking to enter the market or expand their portfolio and is increasing the focus on looking for good value in the sales market.

Our agents report that property owners are increasingly exploring both sale and rental options when considering the next step for their property.

In some areas there is little room for rental growth and increasing evidence that affordability ceilings have been reached, even in the face of constrained supply, with only well-priced properties attracting levels of demand that were commonplace two or three years ago.

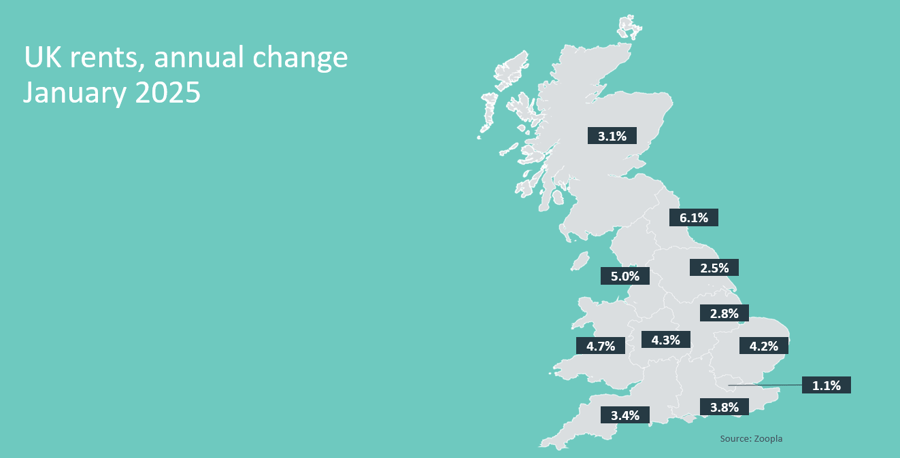

Some of the strongest rental growth is being registered in the most affordable markets, with rents up 6.1% in the year to January in the North East, and 5% in the North West in the year to January, according to Zoopla data. Rents are still registering double digit growth in Blackburn (10%), while rents in Stoke and Rochdale are up 9.6% and 9.3% respectively. Rents are up 6.2% in Newcastle, 5.4% in Liverpool and 3.2% in Manchester, but Leeds is the outlier, with rents only registering a 0.4% rise on the year. The ONS also shows lower rental growth in Leeds – and this is likely to be connected to a local rise in the supply of homes for rent.

Average earnings have risen 6% over the last 12 months, meaning that in many markets, rents have become more affordable over the last year.

We expect average UK rents to rise 5% this year.

The information provided in this report is the sole property of Cluttons LLP and provides basic information and not legal advice. It must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Cluttons LLP. The information contained in this report has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. Cluttons LLP does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.