UK and London sales market update Q1 2023

Average house price growth slowed sharply at the end of last year and continued to ease in January.

Prices will fall during this year, but the outlook differs depending on location. As we moved into February, average UK house values were down 3.2% from the peak of the market in August last year.

Our quarterly update examines the latest trends in the UK, London and prime London sales markets.

Key highlights:

- UK and London house price growth continues to slow in Q1 and is set to dip into negative territory this year amid more muted buyer demand and higher mortgage costs

- Even with house price declines, the value gains registered during the pandemic are unlikely to be fully eroded

- The prime London market has not registered the same level of growth as many other areas of the country over the last 3 years, and will register a more modest decline in values this year with some buyers seeing value in the market

UK overview

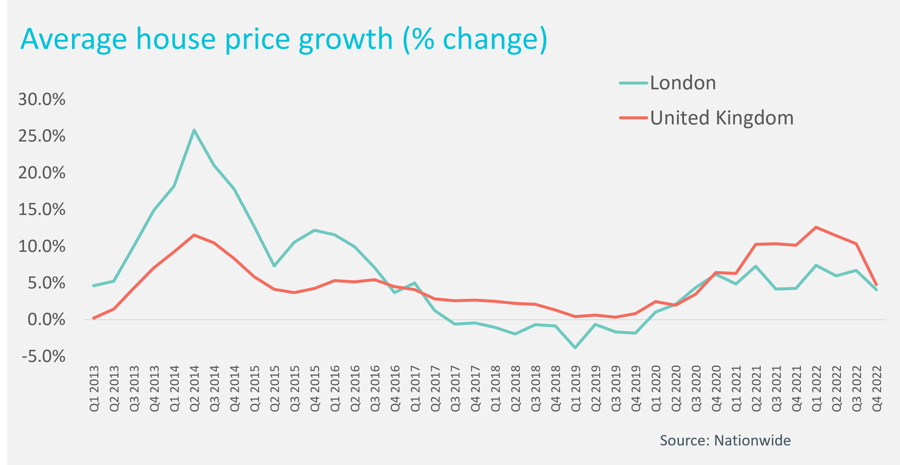

Annual house price growth dipped to 1.1% in January, according to the Nationwide Building Society, the fifth consecutive decline in the pace of growth.

There are many factors which are contributing to house price movements. A significant part of the trend is that house prices are re-balancing after a period of extremely strong growth during the pandemic. This was led by homeowners reassessing how and where they were living, pushing up demand, especially for homes with more space. A stamp duty holiday underpinned additional demand, and then last year, as the pandemic was receding, the return of demand into city centre markets drove another surge in buyer demand – all with the background of ultra-low mortgage rates.

However, as demand in global economies rose again after the pandemic, supply-side difficulties also emerged, fuelling inflation. Russia’s invasion of Ukraine and the resulting energy price shock exacerbated these price rises. The Bank of England responded by starting to raise interest rates, recently introducing it’s 10th consecutive rise to 4%, taking the base rate to the highest level in 15 years.

These factors have curbed the rate of house price growth, and will put further downward pressure on values during this year as demand levels recede. Some first-time buyers will find it more difficult to get onto the housing ladder with higher mortgage rates, and some movers will find that their budgets are more constrained. Millions of homeowners will also see their monthly payments rise – those who are on variable rates or fixed-rate deals. However, the mortgage stress testing that lenders have carried out for the last seven years means that many households have proved they can absorb these rises, limiting the prospect of sudden sales, which put more downward pressure on pricing.

Data from Zoopla, the property portal, shows that UK buyer demand fell sharply after last September’s mini-budget rattled confidence. However, the latest data shows a modest pick-up in the New Year, with demand levels seen back in 2018. This is also echoed across Cluttons’ residential agencies, with supply and demand both ticking up as buyers and vendors adjust to the new economic landscape.

Although the pace of house price growth has been slowing across the country for the last six months, the localised nature of the housing market means that this will show up as different growth levels on a regional and more local level.

In markets where the house price to income ratio is less stretched – making them more affordable compared to the UK average, and very popular during the pandemic – price growth is slowing from a much higher ratel.

We expect the average house prices across the UK to fall by 8% this year, as examined more fully in our recent forecasts. Even with this decline, values will return to 2021 levels, and the rise in house prices registered during the pandemic will not be fully unwound.

London focus

Average home values in London did not rise as quickly as the rest of the country during the pandemic, with average prices rising by 14% between the start of the pandemic and the peak of the market last summer. Average prices are still 11% higher than pre-pandemic levels, according to data from Nationwide, which translates into a £52,000 increase.

There were several reasons underpinning the fact that values did not rise as quickly as elsewhere in the country. Firstly, the movement towards homes with additional indoor and outdoor space during the pandemic meant that buyer demand in the centre of London dipped during the start of the pandemic, while higher levels of demand in outer London boroughs, where houses with gardens make up much of the housing stock, pushed prices up by double figures.

The change in working practices, with many office-based companies abruptly moving to working from home meant that buyers were also able to expand their horizons when searching for a home, leading to a surge in demand in areas of the country where capital values were lower. The higher average house prices in the capital, meaning stretched levels of affordability, thereby put a cap on potential price growth, as did the higher number of homes available for sale compared to elsewhere in the country where supply was very tight.

Houses showed stronger growth than flats during the pandemic as a result of the ‘search for space’ among buyers. As city centre life has flourished once more after the pandemic, with the opening of cultural and social amenities and the resumption of office life, demand for flats is starting to rise once more. With the limited price growth for this type of housing in recent years, some buyers are seeing an opportunity in this market. However, overall buyer demand is expected to remain muted in the coming months in London, and across the UK, according to the latest RICS market survey, as buyers absorb the changing economic landscape and rising mortgage rates as examined in more detail in the economic update.

Prime London

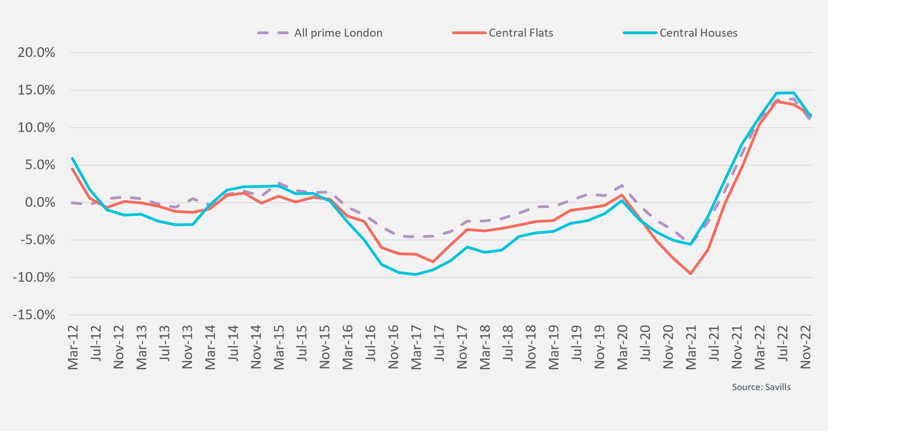

Price growth in the prime residential market in central London has underperformed the wider London market and the UK market over the last two years. The market, which had already been through a period of price adjustment after the introduction of several tax and stamp duty changes from 2015, did not experience the surge in buyer demand seen in the wider UK market in 2020. The international nature of this market meant that travel restrictions had a material impact on overseas demand. The stamp duty holiday in 2021 to 2022 encouraged a return of domestic demand, while for those overseas buyers who were back in the market, the weak pound was also a draw.

As with the wider UK market, demand stalled suddenly towards the end of the year after the mini-budget caused sentiment to dip suddenly. The economic outlook remains more challenging than pre-pandemic, and mortgage borrowing is more expensive, but there are signs that buyers felt more settled in the New Year with demand starting to tick up. Supply is also rising however, which means that realistic pricing will remain key to achieve a sale.

The relatively muted level of growth in the prime London market in recent years means that prices in this sector will not decline by the same margin as the wider UK market. We are forecasting a fall of 4% in central prime London prices this year – as examined in more detail in our recent forecasts.